Shift4 is a decent payment processor. If your business uses them to accept credit cards, the transaction process is likely very smooth, and you get funded as expected every time.

But like nearly every processor, Shift4 has a handful of billing tricks that they use to extract additional profit from your account every single month.

What most merchants don’t realize is that many of these fees can be negotiated or removed altogether.

Here are the ones we typically find when auditing statements, and they’re likely costing you thousands of dollars every single month.

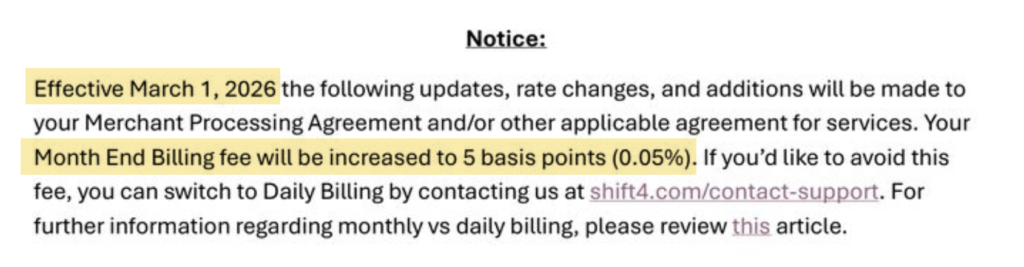

1. Monthly End Billing Fee

For years, Shift4 always pulled its monthly merchant fees from your account as a single debit. This happens on the first day of the month for all accrued processing fees in the previous month, and it’s also the default standard industry-wide.

Now Shift4 wants to charge you extra for this.They introduced a new Month End Billing fee of 0.02% in July 2025, and quickly increased that fee to 0.05% in March 2026.

That’s an extra 5 basis points on your entire processing volume every single month.

Shift4 says you can avoid this fee by switching to daily billing, but this introduces a new set of accounting complexities for reconciliation.

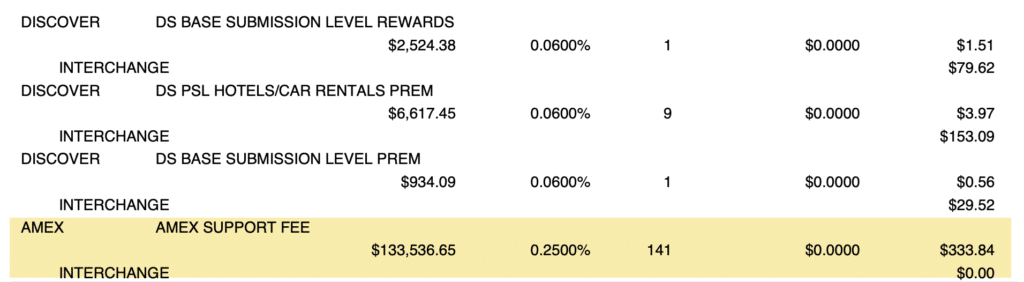

2. Amex Support Fee (or Amex Sponsorship Fee)

Despite having “Amex” in the name and being itemized alongside other card network fees, this is NOT coming from American Express.

Shift4’s Amex Support Fee is a pure profit center for the processor, disguised as a pass-through fee. It’s charged as a percentage of your entire Amex transaction volume each month, typically at 0.25%. Here’s an example:

Shift4 actually does a great job of itemizing statements so you can see a breakdown of what’s going to the processor vs. the network.

And if you look closely at the Amex support fee, you can see that the $0 of the fee is interchange, meaning the entire amount goes straight to Shift4.

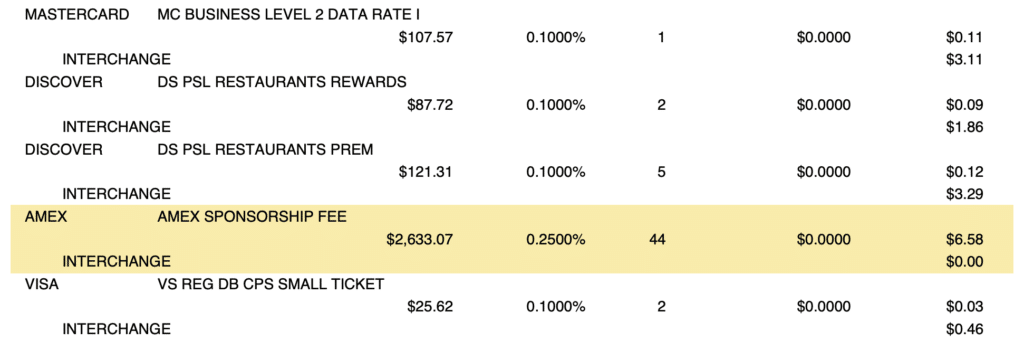

Some of you might see this appear on your statement as an Amex Sponsorship Fee:

But it’s the exact same fee. 0.25% on total Amex volume, with zero going to interchange.

Processors do this all of the time. Change names or slightly rebrand fee names to throw merchants off.

3. Annual Program Fee

Annual fees are a money grab.

Shift4 isn’t the only processor that does this. But their annual fees are among the most expensive because instead of charging a flat amount, they charge per device.

Last year’s annual program fee was supposed to be $99 per device. But we saw this inconsistently charged across accounts. Here’s an example from one of our clients who was charged $250 per device from Shift4’s Annual Program Fee:

That’s $1,000 just because they have four devices.

Shift4 charges you for your equipment initially, then they continue to charge you every time you process a transaction (as they should). So what’s the annual fee program fee for? Nothing.

Don’t let the fact that it’s “only” once per year make you overlook or dismiss this charge.

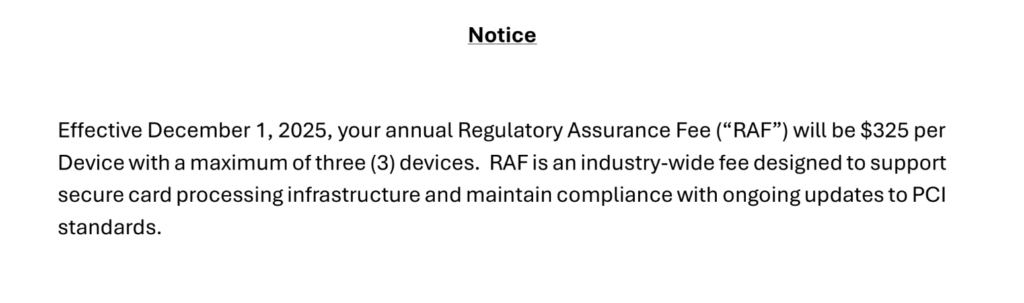

4. Regulatory Assurance Fee

While it sounds legit, Shift4’s Regulatory Assurance Fee is just another annual fee disguised as something else.

It’s $325 per device, with a three-device max, effectively capping it at $975 per year.

And it’s charged in addition to the annual fee mentioned above. Businesses paid thousands in these two fees alone, just a few months apart.

But my biggest problem with the fee is that it’s misleading. Look at this notice they sent out:

According to Shift4, the fee is to maintain PCI compliance standards and imposed industry-wide. This is simply not true. No industry-governing body is forcing processors to charge this fee, and we audit statements from dozens of other processors who don’t charge it.

If they want to charge you an additional annual fee, fine (I guess). But clouding the truth about its origins is another story.

I should also mention that the fee used to be $189.99 per device. The jump to $325 was a massive increase.

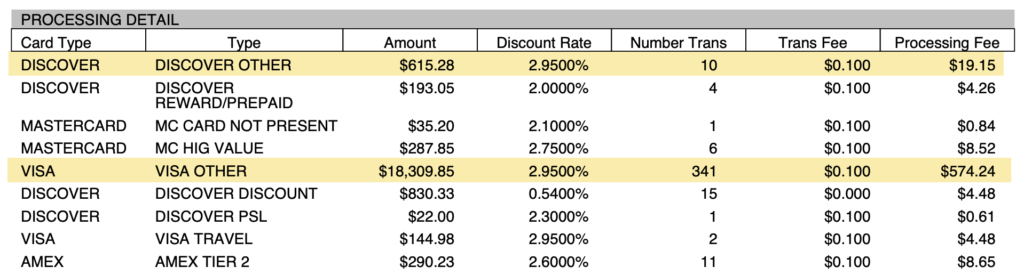

5. Visa/MC/Discover/Amex “Other” Fees

If you’re looking through your statements and see the name of a card network followed by the word other, like:

- Visa Other

- MC Other

- Discover Other

- Amex Other

It’s a sign you’re on Shift4’s simple change pricing structure.

Unlike a true interchange-plus plan, Shift4 simple change arbitrarily groups different interchange transaction categories into buckets with margin built-in. In this case, they’re charging 2.95% for those “Other” transactions.

2.95% + $0.10 per transaction is high to begin with, and it’s right up there with what flat-rate processors charge. But Shift4 is also charging an additional discount rate on top of this. For this particular merchant, it’s an extra 0.54%, which you can see in the screenshot above.

If you compare these fee names against the published interchange rates set by the card networks, you’ll see that the names and rates don’t match.

Shift4 brands its simple change pricing as something that’s easier to understand (because there are fewer line items on the statement). But overall, we typically find merchants overpaying by 20 to 40 basis points on this setup.

Ask Shift4 to give you IC+ as soon as possible to realize these savings.

6. Premium Support and Service Fee

This is another phantom service invented by Shift4 that doesn’t actually give you anything in return.

The amount also varies from account to account. Here’s one merchant paying $25 per month:

And another business paying $70 per month:

Most merchants overlook this cost because the amount is relatively low compared to the other fees and total processing charges. But it adds up, especially when you combine it with everything else.

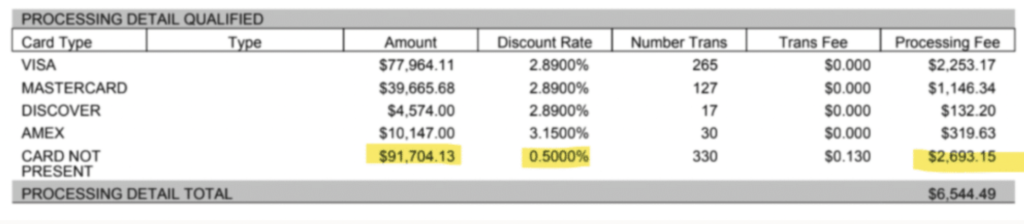

7. Fees That Don’t Add Up Properly

This is why you need to check every single line item on your statement.

Even if the fee is legit and the amount is correct, we’ve found math errors on Shift4 statements that resulted in merchants overpaying.

Check out this example:

This particular business is being charged 0.50% for its card-not-present volume. I don’t agree with it, but that’s not the point here.

Look at the math.

0.50% of $91.704.13 in CNP volume should be $458.52. But the total amount charged was $2,693.15.

It’s so easy to overlook this stuff because everything looks normal if you’re just checking things quickly. Over $2,000+ was deducted here just due to a math “error” by Shift4.

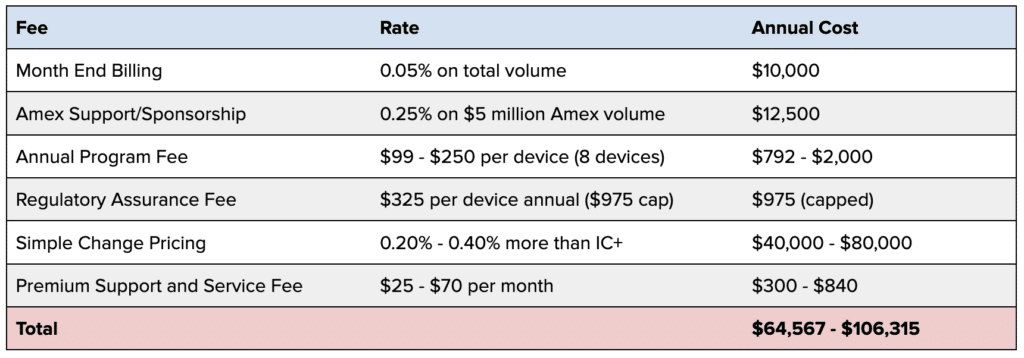

How These Fees Cost Your Business Tens of Thousands of Dollars

In isolation, none of these fees scream red flags or bleeding cash on a single statement. But the total amount in unnecessary overpayments can be staggering when you combine them, especially over the course of a year.

Let’s say you’re a hotel or restaurant doing $20 million annually. Here’s how much extra you could pay:

As you can see, just these handful of charges can easily cost your business $60k to $100k or more on top of all your other merchant fees.

That’s a ton of money.

If you need help negotiating with Shift4 to get these fees reduced or removed from your account, contact our team here at MCC. We’ll identify overages and even help lower your base discount rate directly with Shift4, so you can save thousands every single month.

{kind=link}