If you’re a hotel, airline, car rental company, or another business in the travel space that accepts card payments from travel agents or booking intermediaries, you may be seeing some unfamiliar line items on your payment processing statements.

These merchant fees are part of Mastercard’s Global Wholesale Travel Program, and they come in two forms:

- MC Wholesale B2B Acquirer Fee — 1.57%

- MC Commercial B2B Fee — Ranges from 1% to 2%

Both of these charges apply to the same volume, which is why so many merchants get confused when they see the same transactions getting hit with multiple fees.

Are they both legit? Do you need to pay both? I’ll clarify all of this below.

What is the Mastercard Global Wholesale Travel Program?

Mastercard launched its wholesale travel program specifically for travel intermediaries.

Travel agencies, travel management companies, and booking agents can get issued virtual cards through the program, and then use those cards to pay travel suppliers (hotels, airlines, car rental companies) on behalf of their clients.

Here’s how it works.

- A customer books a trip through a travel intermediary.

- The intermediary collects payment from the traveler.

- Then, separately, the intermediary pays the hotel, airline, or car rental company using a virtual Mastercard account number.

The traveler’s card never enters the picture on the supplier’s side.

Virtual cards used for payments are unique numbers generated for each transaction. So when a hotel accepts one of these payments, it’s not running a guest’s credit card. It’s processing a virtual card from another business (like a travel agency), which is why this falls into its own unique B2B category.

These transactions carry their own pricing structure at both the interchange and assessment levels. Which is why they show up differently on statements compared to standard consumer card transactions and even commercial cards used by business travelers.

Mastercard Wholesale B2B Acquirer Fee (Network Assessment)

Mastercard changes a 1.57% assessment fee at the network level for transactions processed using virtual cards issued through its wholesale travel program.

It shows up on statements as some variation of MC Wholesale B2B Fee or Mastercard Wholesale B2B Acquirer Fee.

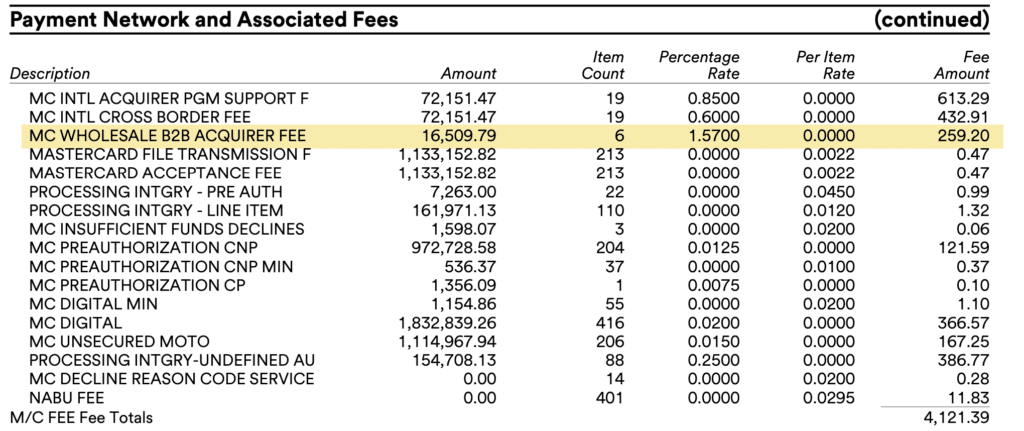

Here’s an example of this on a statement from one of our hotel clients:

As you can see, only six transactions fell into this category, but on $16,509 in total volume. This resulted in $259.20 in merchant fees for this particular line item.

Assessments like this are paid directly to Mastercard, despite “acquirer” appearing in the name. It’s possible that for these virtual card transactions Mastercard does play more of an acquiring role in addition to being the network.

This would explain why the fee is so high compared to other Mastercard assessments. Plus there’s more work involved on the backend for the virtual card program.

Mastercard Commercial B2B Travel Program Fee (Interchange)

The next layer is the interchange rate. This is what your processor pays to the card-issuing bank on each qualifying transaction.

Rates are tiered based on the product code assigned to the transaction:

- MTA — MC Mastercard B2B Product 7 — 2.00%

- MTB — MC Mastercard B2B Product 8 — 1.90%

- MTC — MC Mastercard B2B Product 9 — 1.80%

- MTD — MC Mastercard B2B Product 10 — 1.70%

- MTE — MC Mastercard B2B Product 11 — 1.60%

- MTF — MC Mastercard B2B Product 12 — 1.50%

- MTG — MC Mastercard B2B Product 13 — 1.40%

- MTH — MC Mastercard B2B Product 14 — 1.30%

- MTI — MC Mastercard B2B Product 15 — 1.20%

- MTJ — MC Mastercard B2B Product 16 — 1.10%

- MTK — MC Mastercard B2B Product 17 — 1.00%

- MTL — MC Mastercard B2B Product 18 — 1.45%

- MTM — MC Mastercard B2B Product 19 — 1.35%

- MTN — MC Mastercard B2B Product 20 — 2.00%

- MTO — MC Mastercard B2B Product 21 — 2.00%

- MTQ — MC Mastercard B2B Product 22 — 2.00%

The product code is assigned by the issuing bank in the terms of the wholesale program, and the merchant has no control over which tier applies.

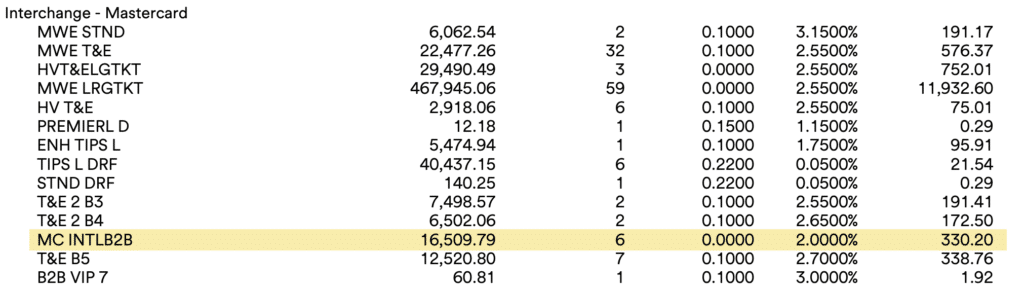

Now if we look at the statement from above, we can see a 2% interchange fee being applied for the for the exact same $16,509 volume:

In this particular case, it’s coded a bit differently as a MC INTL B2B, which is likely because the travel agency is located outside of the US.

I included this example specifically because it’s a good reminder of how things don’t always pass to your statements as cleanly as you’d expect, even if the fee is completely legitimate.

Every processor has their own way of itemizing things, despite how the networks code things internally.

It’s also one of the reasons why it’s so difficult for the average merchant to understand their statements. Even one like this that’s transparent, it’s tough to find things if you don’t know what you’re looking for.

When you combine the assessment and interchange for these transactions, this merchant paid a total of 3.57% on these transactions. That’s $589.40 in network-level costs, before any processor markup.

What to Check on Your Statement

We typically see these fees pop up on hotel statements. But they apply to other travel suppliers too, including airlines, car rental agencies, cruise lines, and passenger railways.

So if you fall into any of these categories, there are a few things you should verify on your statement:

- Does the volume on the B2B assessment line match the corresponding interchange line?

- Both fees apply to the same transactions, so they should match.

- Is your processor clearly itemizing both charges as pass-through costs or are they grouped into broader categories without detail?

- If grouped, it’s easier for them to hide markup.

Again, lots of this is tough for the average merchant to spot. And we’re just talking about two lines on a statement with hundreds.

If you want a professional to look things over and help you out, our team here at MCC can give you a free audit.

{kind=link}