Nuvei is one of the most versatile technology companies in the fintech space, and they operate across multiple layers of the payments infrastructure.

They might be your direct acquirer, or they could be running quietly in the background, powering a platform or software that you already use. Lots of merchants using Nuvei were set up through a third-party ISO, too.

Regardless of how you ended up here, understanding how Nuvei operates both as a processor and at a higher level is important because it directly affects your costs.

What Merchants Should Know About Nuvei

Nuvei is well above average when you stack them up against other processors on the market. Their technology is excellent, and when you weigh their capabilities against overall cost, you’re looking at reasonable pricing all things considered.

But you’re always going to pay above market rates for Nuvei because their processing solutions are tailored to businesses that often require custom or complex setups. And by default, this will always come at a premium (regardless of the processor).

For straightforward processing with mostly in-person card transactions and no integrations, Nuvei’s tech is likely unnecessary.

But for merchants who do need extras that go beyond the basics, Nuvei can be a decent value compared to what you’d get elsewhere for a similar setup.

How Your Nuvei Setup Affects Your Costs

The way you’re accessing Nuvei’s processing services will directly impact your costs.

Acquirer

It’s always going to be cheaper to go directly to Nuvei and have them operate as your acquirer. While they’re still going to have extra fees and higher margin for complicated setups, cutting out the middleman will save you money.

Integration

From there, costs increase if you’re using Nuvei through an integrated setup. For example, Nuvei integrates with ERP systems like Microsoft Dynamics, Sage, and Acumatica (among others). So even if Nuvei is still your acquirer and you have a merchant account directly with them, you’ll pay more because it’s more expensive for Nuvei to support this setup and there’s less competition in these markets.

ISO

There’s also going to be extra margin baked into your processing rates if you’re getting Nuvei through an ISO. That organization sits between you and Nuvei, providing your setup and support. So the markup is set in a way to ensure Nuvei and the middleman both profit.

PayFac

Additionally, there are software providers and PayFacs out there that rely on Nuvei to power their own “in-house” or embedded payment solution. In these cases, Nuvei is technically handling the backend processing on your account, but your agreement is typically with the third party that sits in the middle. It’s the most expensive setup for merchants, and the provider is the one setting the rates.

Nuvei Pricing and Fees to Watch Out For

Assuming you do have a direct relationship with Nuvei, merchants are offered three different pricing structures. Though you should only be considering one of them.

- Tiered — Nuvei groups transactions into three buckets (qualified, mid-qualified, and non-qualified), with higher prices at each tier. The problem with this structure is that they control the qualification criteria, so it’s in Nuvei’s interest to ensure the majority of your transactions fall into the highest-cost buckets.

- Flat Rate — As the name implies, you pay the same rate for every transaction. While the simplicity of this setup helps it sell, it’s very expensive and the markup on certain transactions can easily exceed 100 bps.

- Cost Plus — The best option and the only one we recommend. You pay the wholesale interchange rates set by the card networks, plus a transparent markup directly to Nuvei.

I can’t emphasize this point enough: make sure you’re on a cost-plus (interchange-plus) pricing plan from Nuvei. It’s practically a guarantee that you’re overpaying if you’re on a tiered or flat-rate structure.

And while your cost-plus markup could be higher than it should with room for negotiation, it’s still the cheapest overall despite any perceived complexity.

Other Nuvei Fees

In addition to what Nuvei charges you per-transaction, they also impose a range over other fees that could be applied to your merchant account, including:

- Monthly Clearing Fees

- PCI Monthly Fees

- Anniversary Fee (a nicer-sounding way to name an annual fee)

- Monthly Gateway Fee

- Monthly Statement Fee

- Wireless Fees

- Overage Wireless Fee

- Wireless Activation/Setup Fee

- Quarterly Data Security Fee

These are all Nuvei-imposed and they’re 100% negotiable. They’re not nearly as egregious compared to the extras charged by other processors, but they can definitely add up quickly.

The one you need to watch most closely is the Monthly Clearing Fee because it’s directly tied to your total volume of approved authorizations.

But any of these can be negotiated, lowered, and potentially removed from your account altogether.

Nuvei Statement Audit (and How to Spot Additional Markups)

I’ve pulled statements from two of our clients using Nuvei so you can understand what to look for on your own and how fees can vary drastically between accounts. And while Nuvei is generally a good processor, you’ll see that their reporting can be somewhat deceptive and is presented in a way that can bury additional margin.

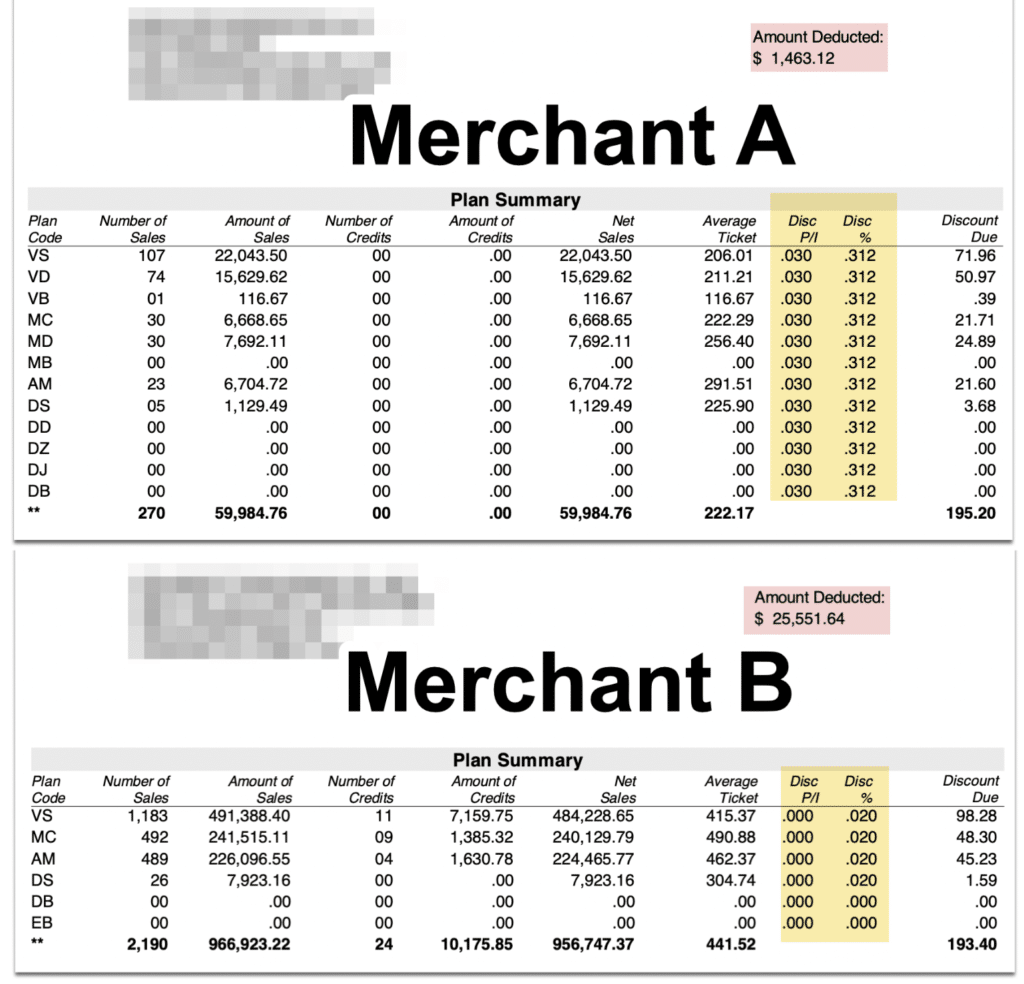

Comparing Two Nuvei Merchant Accounts

Both of these merchants are on a cost-plus plan from Nuvei. But their volume is drastically different, which directly impacts their discount rate.

Merchant A

- $59,984 net sales

- 0.312% + $0.03 per transaction

- $1,463 total fees

- 2.43% effective

Merchant B

- $956,747 net sales

- 0.02% per transaction

- $25,551 total fees

- 2.65% effective

There’s a lot to unpack here and we’re only at the first page summary.

The first obvious callout is that Nuvei is willing to give drastic discounts to merchants processing a higher volume (as they should). Merchant B’s sales are more than 15x higher than Merchant A, so Nuvei charges them just 2 basis points per transaction vs. 31 bps.

So how is it possible that Merchant B’s effective rate is 22 bps higher than Merchant A, when their discount rate is so much cheaper?

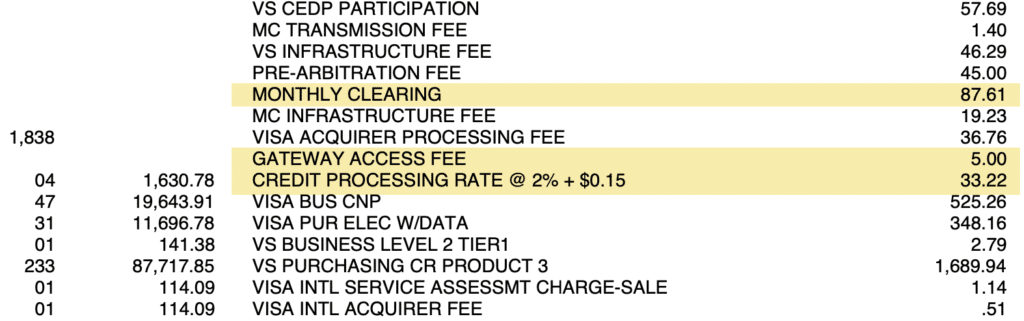

Where Additional Markups Appear

If we continue to the “Fees” section of the statement, you’ll see that Nuvei has additional markups buried alongside the interchange fees and network assessments.

We can see the Monthly Clearing Fee I mentioned earlier, plus a Gateway Access Fee (though $5 is nothing to lose sleep over on an account processing nearly $1M per month).

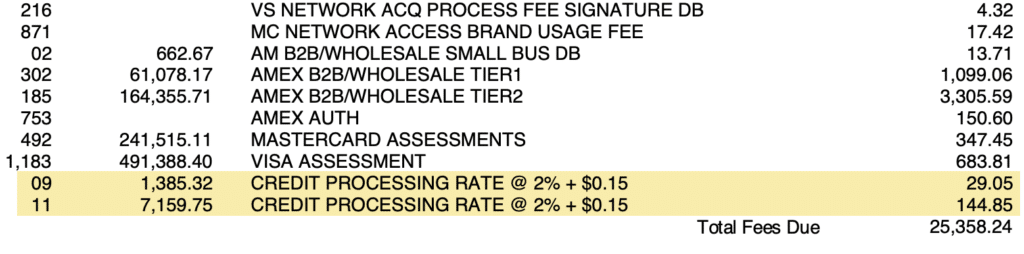

There are also transactions that are charged an additional 2% + $0.15 per transaction. And even more get hit with those same charges further down in the statement:

Why the Statement Summary Can Be Misleading

In just the five fees (there are more) that I’ve highlighted above, we can quickly uncover another $300 in extra markup charged on this account.

Which is why you can’t just rely on the total amounts summarized at the bottom of your statement:

At first glance, it’s easy to just skim through this and assume Nuvei is charging you $193, which seems like a drop in the bucket on $950k+ in sales. But that’s not the case.

And while a 2.65% effective rate is still solid, you can see why you need to analyze and scrutinize every line item on your statement.

Is it Worth Switching to Nuvei?

If you already have a merchant account with another provider, it’s typically in your best interest to see if you can get what you’re looking for from your current processor before switching to Nuvei.

While Nuvei’s technology definitely supports needs that other providers don’t offer, switching processors is more expensive than meets the eye.

You’ll need to assess whether you actually need the setup offered by Nuvei. And if it’s worth the switching fees, early termination penalties, and extra costs for the complex/custom/integrated setup.

Don’t let a low quote from Nuvei fool you. While they are a good processor and rates are reasonable, you can see from the example above that even a crazy low discount rate of 0.02% doesn’t actually translate that low once you get going. There are other fees that will drive up your costs that are tough to account for on a quote alone.

My suggestion would be to negotiate lower rates with your current processor first. See if you can save money there (which you likely can).

If You’re Already Using Nuvei for Payment Processing

The first thing you need to do is make sure you’re truly on a cost-plus (IC+) pricing structure.

This simple move of switching from tiered or flat-rate to IC+ without changing anything else will likely save you thousands on processing.

For those of you already on a cost-plus setup, there are other savings opportunities that you can target. Negotiating your discount rate is the obvious move, and if you process a decent volume, you can definitely get a lower rate.

But you should also be looking closer at other line items on your statement, particularly in the “Fees” section as that’s where Nuvei will place some other fees that you can remove or at least negotiate lower.

Final Thoughts

Nuvei is a very good processor.

Despite the extra fees that I called out in the statement examples above, this is really nothing compared to what other processors do. Even the extra margin isn’t that egregious. As the flat monthly fees are lower, and the volume-based fees aren’t charged at absurd rates.

It’s rare that you can pull two statements from one provider and see effective rates of 2.43% and 2.65%, especially with added markup baked in above the discount rate, and for accounts requiring specialized tech setups.

If you need help figuring out whether Nuvei is right for you or if you want an extra set of eyes on your statements, contact our team here at MCC for a free audit. We can help you save money on Nuvei or credit card processing from any provider, without switching anything.

{kind=link}