Despite rapidly rising merchant fees industry-wide, cheap credit card processing still exists. But getting the cheapest rates depends on several factors.

Here’s what you need to know:

- All processors can be cheap if they want to.

- 2.9% + $0.30 flat-rate processing is NOT cheap.

- Interchange-plus contracts are the best way to get cheap rates.

- Going directly to an acquirer is cheaper than processing with ISOs for PayFacs.

- “Free” and “zero-fee” payment processing are just surcharging programs that aren’t actually cheap at all.

It’s important to understand that your current processor has the ability to offer you low rates. So don’t assume that you need to switch providers to get cheap credit card processing (you probably don’t).

4 Examples of the Cheapest Credit Card Processors

Before I show you what cheap credit card processing actually looks like, I want you to understand exactly where this information is coming from.

- We have over 1,400+ clients, and analyze roughly 20,000 merchant statements every year.

- We’ve seen statements and contracts from hundreds of different credit card processors.

- We work with businesses in practically every industry, so we’ve seen how these differences impact merchant rates.

Based on all of this information, I’ve compiled four examples of the cheapest rates we’ve seen over the last year.

But I want to make it clear that just because a processor is listed below, it doesn’t automatically mean that they always offer cheap rates. Even the cheapest credit card processors sometimes overcharge certain businesses (just like we’ve seen some notoriously expensive processors also offer cheap rates).

These four examples are from real clients of ours, and our first-hand experience seeing cheap rates. We have zero affiliation with these processors, and we’re not compensated in any way if you sign up for their services (unlike practically every other list of cheap credit card processing that you’ll find on the web).

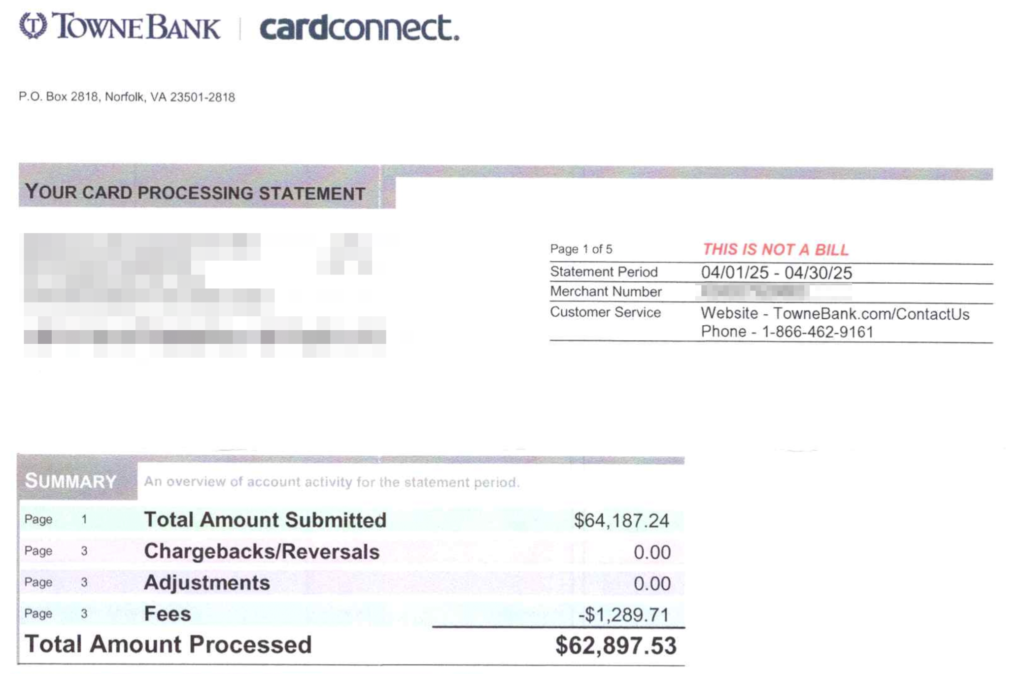

Example 1 – CardConnect: 2.05% Effective Rate for Low-Volume Healthcare Business

CardConnect is a wholly-owned subsidiary of Fiserv. So unlike other ISOs on the market, you can get cheap credit card processing from CardConnect because they’re under the same roof as the acquirer.

In this example, our client is paid a 2.05% total effective rate for the statement period, which is exceptional.

What makes this rate even better is the fact that this business isn’t processing a high volume of payments. ~$63k per month is relatively low, comparatively, and yet they were still able to secure a really good rate.

For more context, this is a small healthcare practice that primarily processes credit card payments in-person without any complex integrations or anything like that.

I also want to point out that this merchant was set up with CardConnect through their local bank (TowneBank in Virginia).

Typically, going through a reseller like this adds to your costs. But this just further illustrates how every processor has the ability to give you cheap rates. Whether or not they’re willing to do it is another story, and totally subjective for each merchant account.

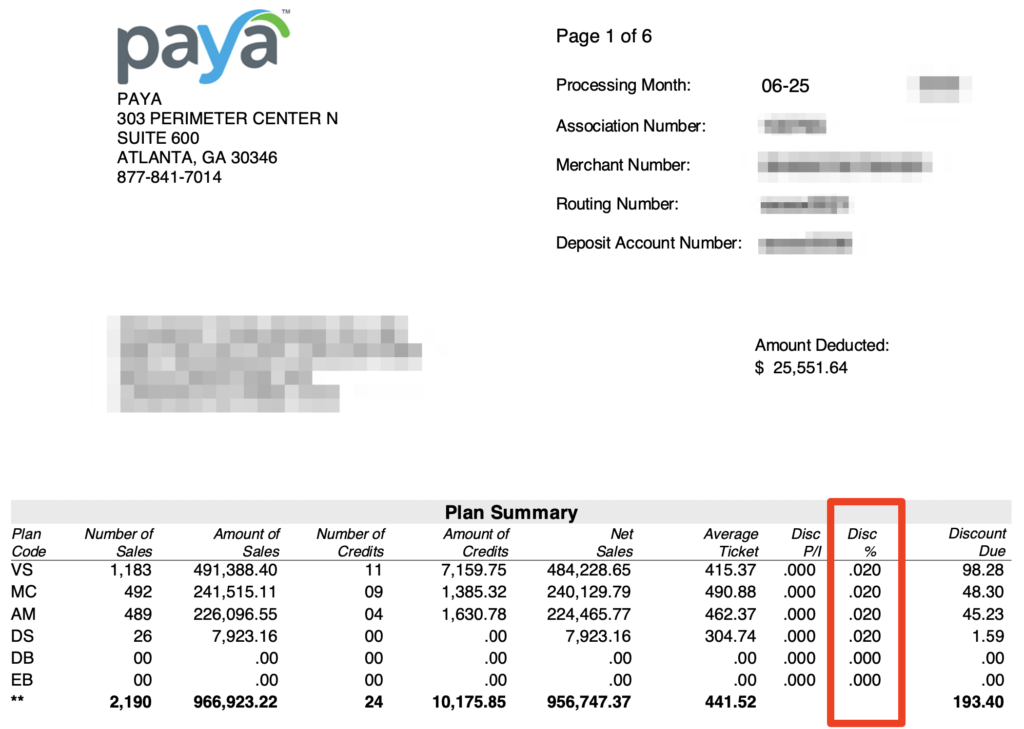

Example 2 – Paya: 2 Basis Point Discount Rate for B2B Ecommerce

Paya (now part of the Nuvei umbrella) has always offered reasonable rates to our clients using them for payment processing.

For this particular business that sells products online to other businesses, Paya is only charging a 0.02% markup on each transaction.

Processing $950k per month is a decent volume, and definitely incentivizes Paya to offer a lower discount rate.

When you factor in the total merchant fees, their effective rate for the month is 2.67%.

The bulk of this is interchange. Online transactions and card-not-present sales will always carry a higher interchange rate.

But Paya does have some other markups they’re charging beyond the discount rate, including gateway access fees, monthly clearing fees, and a few other miscellaneous charges.

Though overall, the discount rate is definitely considered cheap, and it’s one of the better effective rates you’ll see for this type of setup.

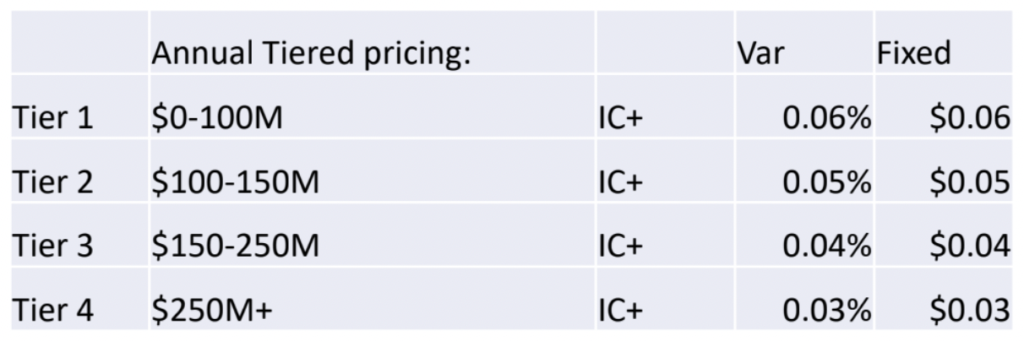

Example 3 – Braintree: 0.03% + $0.03 for High-Volume Ecommerce

Braintree is the enterprise credit card processing division of PayPal. They offer some of the best technology on the market today, and some of the cheapest rates we’ve seen.

The catch is that you need to process a ton of volume to access these rock-bottom rates.

Here’s a tiered IC+ structure that Braintree offered to one of our clients:

The rates drop to 0.03% + $0.03 per transaction if the merchant processes $250 million annually. It doesn’t get much cheaper than that in the ecommerce space.

Starting them off at 0.06% + $0.06 for the first tier is also a great deal.

It’s contingent on a 3-year contract and the merchant agreeing to route 90% of their volume through Braintree (instead of using multiple processors).

Before we negotiated with Braintree on their behalf, they were on a three-tier structure starting at 0.08% + $0.08 per transaction, and the cheapest rate dropped to 0.05% + $0.05 when they exceeded $250M. But we were able to help drive the price down even more.

Another bonus about getting cheap rates from Braintree is that they rarely raise rates. Other processors may start you off with decent pricing, but they’ll systematically raise rates every 12-18 months to the point where it’s no longer considered cheap. That’s not the case here.

Example 4 – Elavon: 2.09% Effective With Mixed Transaction Profile

I’ve always considered Elavon to be relatively fair compared to other acquiring banks. Cheap rates are definitely available, and they’re receptive to negotiations.

This particular client is unique because they have a mix of online transactions, in-person retail, and even some corporate/commercial charges.

Elavon is giving them a 2.09% effective rate on $1.9+ million in monthly processing.

This falls into the high-volume range. They’re also getting L2/L3 optimization for the commercial card transactions, which helps keep their effective rate low.

Elavon’s markup is just 0.06% (6 basis points).

2.09% effective and 0.06% discount rate both translate to the same thing: cheap credit card processing.

But I do want to call out that not every business using Elavon gets a deal this good. In fact, Elavon just announced a 0.07% + $0.18 rate increase for some accounts that went into effect in February 2026. This rate increase alone is more than the merchant in this example is paying overall.

How to Get the Cheapest Credit Card Processing Rates

So, how can your business get cheap credit card processing rates like the examples above?

Consider the following:

Start by Negotiating with Your Current Processor

One misconception is that you need to find a certain processor to access cheap rates on credit card processing. In reality, every processor has access to the same wholesale interchange rates. You just need to negotiate a low markup.

If you haven’t discussed rates with your processor since your initial contract, there’s a good chance you’re overpaying. Even if they tell you that “you’re already getting the cheapest rate” you can’t take their word for it. So keep pushing for better terms.

Make Sure You’re on an IC+ Structure

Interchange-plus is the best way to get cheap credit card processing. It’s the most transparent and helps separate network fees from processor markups.

That said, we’ve also seen merchants on an IC+ plan with processors charging them well over 100 basis points per transaction. So interchange-plus doesn’t automatically equate to cheap credit card processing. You still have to negotiate a good deal.

Know What’s Considered Cheap for Your Specific Business

Credit card processing rates aren’t always an apples-to-apples comparison, and there are various elements that will always cause your rates to increase.

For example:

- Certain industries are automatically considered high-risk and carry higher rates.

- Integrated setups with third-party software are more expensive.

- Card-not-present transactions are more expensive than in-person sales.

Some of this stuff is completely out of your hands.

If you exclusively sell online, your floor is likely higher than a business that has a brick-and-mortar retail setup.

A dentist who integrates processing with a practice management solution offering digital payments will likely have higher rates than a neighboring practice that has standalone processing and only accepts cards in-office.

Volume Matters

Your credit card sales volume is one of your biggest negotiation levers because your processor gets a percentage of every transaction. The more you process, the more money in their pocket.

Most processors are willing to offer cheaper rates to businesses processing millions of dollars monthly. And as you’ve seen from the examples, those rates can drop even lower when you get into the tens of millions or hundreds of millions in annual processing.

Though cheap processing for low-volume merchants is still possible (like the 2.05% effective rate on ~$62k example I showed you earlier).

Avoid Gimmicks

There is no such thing as free credit card processing or zero-cost payment processing.

Any processor promoting this type of service is just going to pass those costs to your customers in the form of a surcharge. And in reality, these are some of the most expensive rates we’ve seen merchants pay.

I also recommend avoiding flat-rate processing. While this isn’t a gimmick, these processors sell you on the illusion of simplicity. Yes, flat-rate processing is easier to wrap your head around compared to interchange-plus. But you’re never going to get the cheapest rates by going this route.

{kind=link}