If your business uses Elavon for credit card processing, your merchant agreement is likely set up on “monthly billing” by default. This is the preferred choice for accounting reconciliation, and it’s the standard setup for most processors industry-wide.

But Elavon has decided that the convenience of monthly billing is worth charging extra for. And if you want to keep this setup, you’re going to pay a premium for it.

That’s where the Elavon Monthly Billing fees come from.

Key Takeaways:

- Ellavon’s Monthly Billing Fee is 0.08% of your total processing volume.

- The fee has increased 4x over the last three years.

- You can remove it by switching to daily billing, but this creates reconciliation problems for most businesses.

- The rate is negotiable, and we’ve successfully reduced it for clients without switching billing methods.

How the Monthly Billing Fee Works

The Monthly Billing Fee (sometimes labeled Monthly Discount Adjustment Fee) is a percentage-based fee applied on your total monthly processing volume with Elavon.

It’s not a fixed or flat rate, and it’s not tied to any specific transaction type. The more you process, the more money you’re going to pay.

You can find the charge as a single line item in the “Other Fees” section of your Elavon statement.

The rate has increased significantly over the last few years. It’s currently 0.08% of total volume (effective February 2026), up from 0.02% in 2023 and 0.06% in 2024-25.

Monthly vs. Daily Billing: What’s the Difference

To clarify, “monthly billing” has nothing to do with when you get funded.

With Elavon, your deposits will still hit your bank account on roughly the same schedule (1-3 business days), regardless of whether you’re set up on monthly or daily billing. The difference is how and when Elavon collects their processing fees.

- Monthly Billing: Elavon deposits your gross card sales throughout the month, then pulls all accumulated fees in a single lump-sum ACH debit. Daily deposits match sales, and you settle up with Elavon once a month.

- Daily Billing: Elavon nets out their percentage-based fees from each batch before depositing your funds. Your deposits are lower than actual sales because the discount fee is taken out each day.

Behind the scenes, Elavon is paying interchange and assessments to the issuing banks and card networks whenever you settle transactions. Elavon is effectively fronting those costs to merchants throughout the month, which functions like a rolling, interest-free micro-loan on those fees until they’re swept at the end of the month.

That’s their justification for the fee. They’re compensating themselves for the float.

But in reality, they’re just monetizing the fact that merchants generally find monthly billing easier to reconcile and it’s better for perceived cash flow. Most processors don’t charge for this unless you’re high risk or have a poor payment history.

What This Fee Actually Costs

Fractions of a percentage may not sound like much. But at 0.08% of your total monthly volume, this fee adds up quickly.

Here are a few examples so you can estimate this based on how much you process:

- $250,000 per month = $2,400 per year

- $500,000 per month = $4,800 per year

- $1 million per month = $9,600 per year

And that’s just one line item on your statement that’s likely filled with other Elavon fees designed to pad their markup.

When you account for these additional charges beyond your discount rate, you could easily be paying Elavon an extra $20,000 to $30,000 every year in fees you never agreed to.

Can Elavon’s Monthly Billing Fee Be Negotiated?

Honestly, Elavon tends to be stubborn about this one. If you ask them to remove outright without agreeing to switch to daily billing, you’ll likely hit a wall.

But the rate itself is negotiable, and we’ve successfully got it lowered on behalf of our clients.

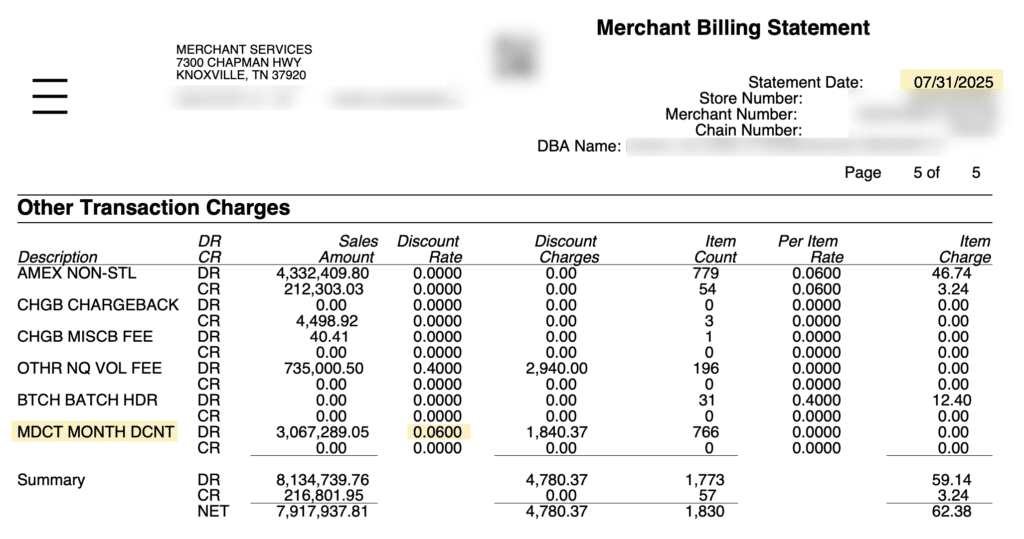

Here’s an example from July 2025, when Elavon’s Monthly Billing Discount Rate was 0.06%. You can see it labeled as MDCT MONTH DCNT in the Other Transaction Charges section:

At $3,067,289 in volume, that single line item cost this merchant $1,840 in one month.

After negotiation with Elavon on our client’s behalf, we were able to get this fee lowered to 0.02% without having them switch to daily billing.

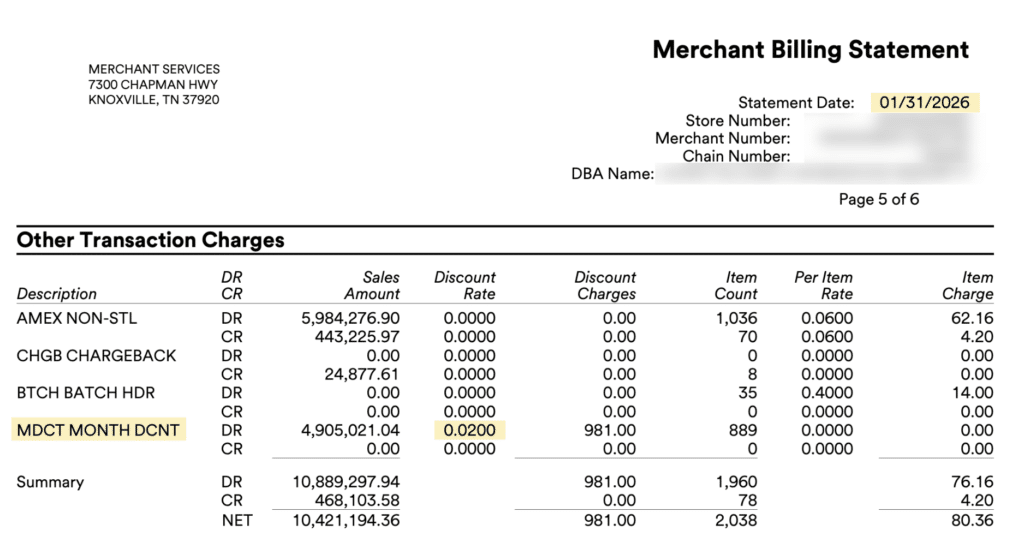

Here’s what that same account looked like in January 2026:

What makes this result even more noteworthy is that the merchant processed significantly more volume in January 2026: $4,905,021.

Yet the fee was just $981.

They ran 60% more volume through Elavon and paid nearly half as much for the fee. This is a direct result of our negotiations with them.

And if you look even closer at the July 2025 statement, you’ll also notice an OTHR NQ VOL FEE that cost this merchant an additional $2,940 that month. This fee is completely gone on that 2026 statement. More savings we were able to negotiate.

What to Do If You’re Paying This Fee

Pull out your latest Elavon statement to double-check if you’re paying this fee. Navigate to the “Other” section of your statement and look for some variation of MDCT MONTH DCNT.

If it’s there, you have a few options:

- Switch to daily billing to eliminate this fee entirely.

- Contact Elavon directly to push back on the rate.

- Have an expert negotiate with Elavon on your behalf.

Daily billing just doesn’t make sense operationally for lots of merchants due to the accounting and reconciliation complexities.

So your best bet is negotiating directly with Elavon. The problem is that Elavon isn’t always receptive to negotiations when merchants reach out. They assume you’re uninformed, and tell you “there’s nothing they can do.”

But when we contact Elavon on your behalf, we have hard proof that they’re willing to reduce the rate. They can’t tell us “the rate is set in stone” because we know for a fact that they reduced it for other accounts.

That’s why we’ve had so much success negotiating with Elavon over the years, and we’re able to get other junk fees removed from your statement, too.

{kind=link}