Processing international credit card sales is a crucial component of growth in the ecommerce space. That’s one of the most appealing aspects of selling online—your customers can be anywhere with internet access.

With that said, credit card processing fees are increasing. Merchants that sell goods internationally have been disproportionately affected by these increases.

Between rising costs to process cross-border transactions and other fees associated with international sales, ecommerce merchants aren’t profiting as much as they would like to. It’s simple—international credit card fees are cutting into your bottom line.

So how can you increase profit margins on international sales? Continue reading below, and I’ll explain everything you need to know.

Understanding Cross-Border Interchange Fees

Simply put, it costs more money to process an international transaction than a domestic one.

Over the last two years, credit card processors have been increasing international interchange fees. These are additional charges that are calculated on top of the standard interchange rates associated with any credit card transaction.

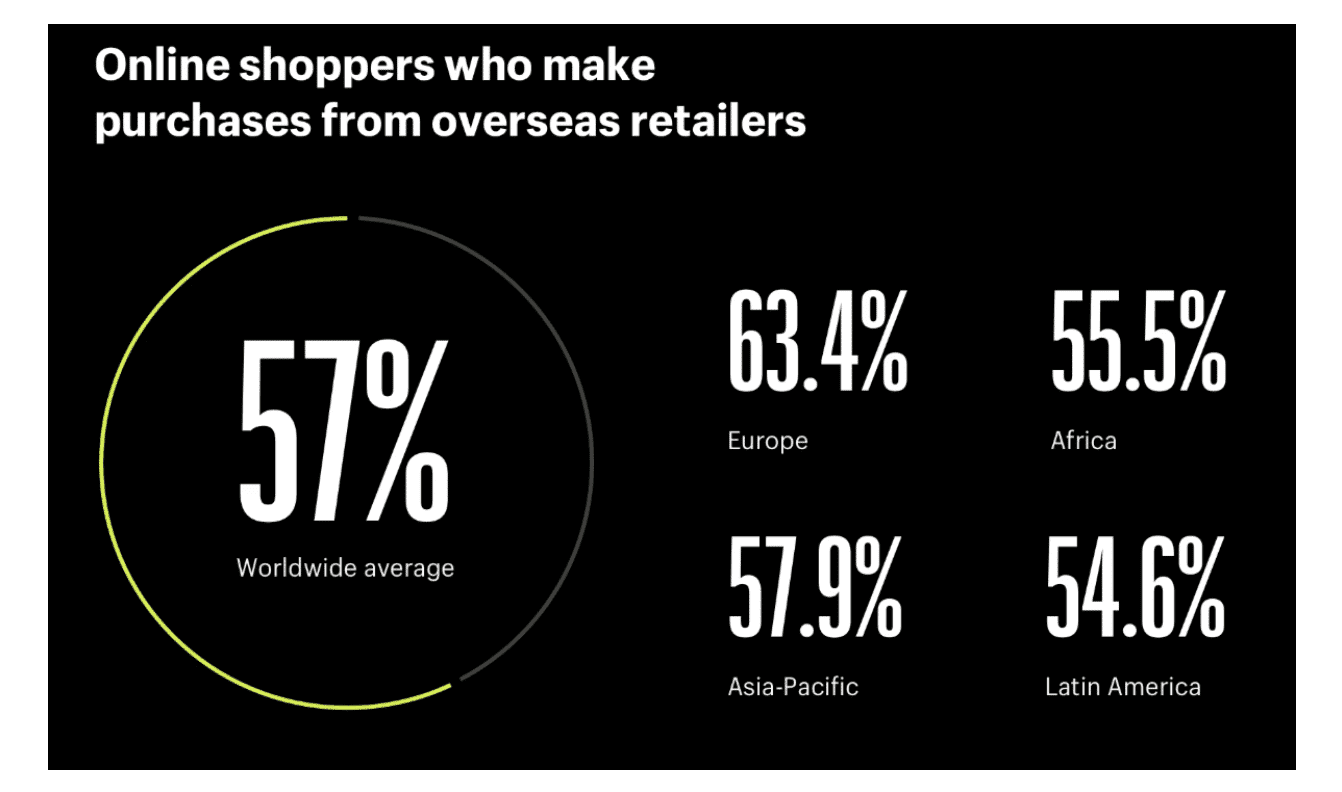

More than half of online shoppers across the world have made online purchases from an international retailer, according to a recent study from Shopify.

Credit card companies have recognized the growth of international ecommerce and likely saw these trends as an opportunity.

Many countries have put caps on domestic credit card processing fees. Still, there aren’t any international regulations for cross-border businesses regarding how much they can be charged.

Why are cross-border interchange fees higher than domestic transactions? While it’s easy to point the finger at the card networks and processors, greed is not the driving factor here.

Banks take a higher risk to process an international transaction. There is an increased chance of fraud for these sales. So increasing the rates makes sense for these organizations, as it helps protect them against fraudulent transactions.

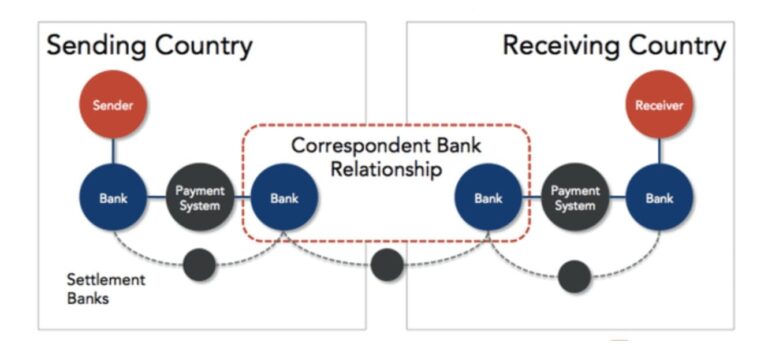

Furthermore, the transaction itself is more complex during a cross-border sale. In many cases, there are two bank transactions taking place between two payment systems in different countries.

Every credit card transaction has middlemen involved. Between the merchant and the consumer, you have the acquiring bank, issuing bank, credit card processor, and the card network.

Each player in between the merchant and consumer must be paid for their role in the transaction. But when you process an international sale, you’re adding a new intermediary to this picture, in order to connect the banks between two countries. As a result, the fees are higher.

It’s the same reason why international wire fees are higher than domestic wire fees. Many banks charge $25-$35 for a domestic wire, while they charge upwards of $45 for an international wire.

Here’s something else to keep in mind. Card networks determine what is defined as a “cross-border” sale. In many cases, this doesn’t align with the actual borders we know between countries.

For example, let’s say a French consumer makes a purchase from a US ecommerce merchant using a Visa card. Visa considers this to be a cross-border sale. However, if that same shopper buys something from an Italian retailer, it won’t be a cross-border transaction. When it comes to payment processing, Visa groups France and Italy in the same region.

How to Reduce Cross-Border Transaction Fees

Interchange rates set by the card networks are non-negotiable. But with that said, there are a few ways that you can avoid these expensive processing fees and increase margins on international sales.

Get a Domestic Merchant Account

This is only a viable option for merchants that do a ton of volume in a particular region. It’s not an easy process, and it’s not something that happens overnight. There are also lots of other factors to take into consideration before you make this decision, such as the tax implications.

With that said, incorporating your business in another country would allow you to get a domestic merchant account in that area. As a result, you would be able to bypass paying the cross border fee.

Again, this doesn’t make sense for the vast majority of ecommerce retailers. But it’s worth considering for businesses with a well-established customer base in foreign areas.

The US and Canada Exemption

If setting an up an additional corporate entity in another country doesn’t sound appealing to you, there is an exemption between the United States and Canada that can help you avoid paying cross-border interchange fees.

Visa outlines special circumstances in its international operating regulations. The exemption allows for US merchants to get a domestic Canadian merchant ID. Candian companies also have the option to get a domestic US merchant ID.

This exemption is only for virtual terminals and ecommerce merchant accounts and only gives you the ability to process credit cards within that region.

Partner With a Company to Lower Your Credit Card Processing Rates

While there’s nothing you can do about the interchange fees set by the card networks, there are other ways to lower your processing fees.

Partner with a company that can negotiate your credit card processing costs on your behalf. Here at Merchant Cost Consulting, we’ll speak to your credit card processor and find other ways for you to save money on processing.

As a result of these savings, you’ll generate higher margins on cross-border sales.

Final Thoughts

International transactions and cross-border interchange fees are eating into your profits. While it may not seem like much, an additional 1% fee can add up quickly.

Let’s say your store sells $250 million worth of goods annually. 30% of those sales are international. That means $75 million of your revenue is subject to cross-border interchange fees. Assuming you’re paying an additional 1% for international transactions, that’s an extra $750,000 per year in credit card processing costs.

No matter how big your company is, that’s a ton of money.

So contact our team of experts here at Merchant Cost Consulting. We’ll help you lower your credit card processing costs and ultimately increase your profit margins on cross-border sales.

{kind=link}