If you’re using Elavon as your payment processor and you’ve accepted a foreign-issued credit card, there’s a good chance you’ve seen an International Card Handling Fee on your monthly statement.

At first glance, it appears innocent. Your business might be in an industry where a high volume of international customers is normal (hotel, restaurant, airline, etc.). So the charge seems appropriate, and you may not question it at all.

Big mistake. Here’s why:

- Elavon’s International Card Handling Fee is a processor-imposed markup.

- It’s charged on top of your regular discount rate and per-item fees.

- It’s disguised as a network fee, appearing alongside legitimate assessments on your statement.

- The card networks already charge higher rates for foreign-issued cards.

- Elavon’s INTL Card Handling Fee is piled on top of that.

If your business processes lots of international transactions and cross-border cards, this fee can quietly cost you tens of thousands of dollars every year. And it’s something you shouldn’t be paying at all.

What is the International Card Handling Merchant Fee?

International Card Handling Fees are charged by Elavon whenever a foreign-issued card is used. It’s billed as a percentage of total cross-border volume for each card network.

- Rate: 0.80% per cross-border transaction (as of February 2026).

- Applies to every foreign-issued card processed via Elavon.

- Itemized separately but charged the same amount for Visa, MC, Amex, and Discover.

- Paid directly to Elavon as a processor-imposed markup.

The most important thing that you need to understand about this fee is that it’s a pure processor markup for Elavon, which means it’s 100% negotiable and should be eliminated from your statements altogether.

How it’s Different From Legitimate Network Assessments

Every major credit card network charges its own fees when you process foreign-issued cards. These are non-negotiable assessments that go directly to Visa, Mastercard, Discover, and American Express.

Examples include:

- Visa International Service Assessment (ISA) – Varies (~0.20% to ~1.20%) based on location of merchant and issuing bank

- Visa International Acquirer Fee – 0.45%

- Mastercard International Cross-Border Fee – 0.60%

- Mastercard Acquirer Program Support Fee – 0.85%

- Discover International Cross-Border Fee – 0.80%

- Discover International Processing Fee – 0.50%

- Amex International Assessment – Ranges from 0.40% to 0.60%

Notice anything here?

Every card network charges a different assessment rate for international processing. They all have their own fee schedules and unique criteria for applying those charges.

So it’s a red flag when you see Elavon’s broad International Card Handling Fee with the exact same name and exact same percentage charged across every network.

Here’s an example that shows the MC INTL Card Handling Fee directly next to Mastercard’s legitimate international assessments:

What’s funny is that the total combined amount of those two legitimate Mastercard assessments is less than the amount of the single fee invented by Elavon.

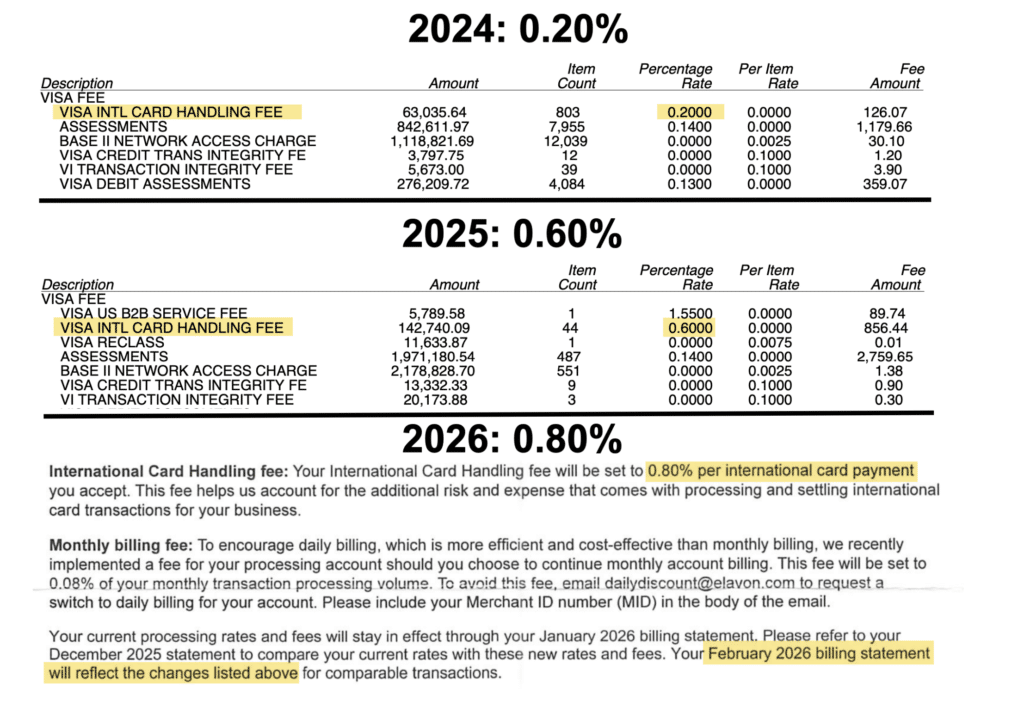

The Rate Keeps Rising Every Year

Here’s where it gets worse. Elavon’s International Card Handling Fee has been steadily increasing every year.

- 2024: 0.20%

- 2025: 0.60%

- 2026: 0.80%

That’s a 300% increase in just two years.

If your business processes $1M in foreign-issued cards, the cost just jumped from $2k per year in 2024 to $8k per year in 2026. That’s $6k in additional fees every year for the exact same $1M in sales.

It’s extremely rare to see a merchant fee increase so rapidly in such a short period of time.

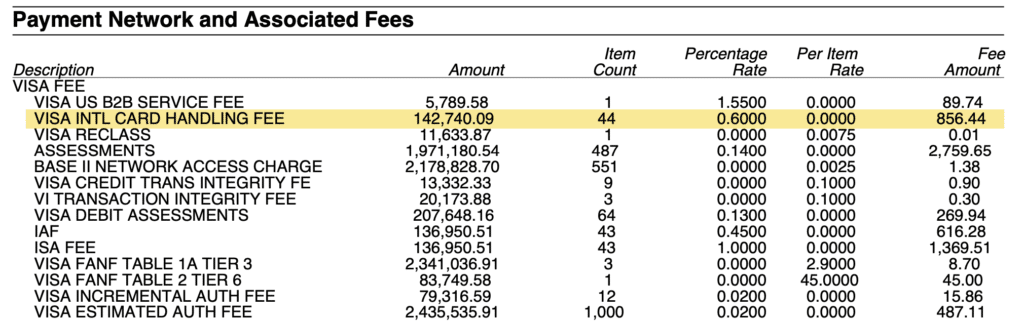

Why the Placement is So Deceptive

Processors are always going to try to squeeze more revenue out of you in the form of rate increases and additional fees. That’s standard practice industry-wide.

But my biggest problem with this particular fee is the way that Elavon presents it to you.

The fee is listed in the Payment Network and Associated Fees section of your statement, alongside other legitimate network fees:

Everything else goes straight to the networks, including the IAF and ISA Fees (Visa’s actual international assessments). Assessments are mandatory and non-negotiable.

And by itemizing this fee here, Elavon knows it’s going to be nearly impossible for merchants to catch it and identify it as an inflated processor markup.

Most merchants have zero reason to question the charge because it’s literally presented as a network fee, which would mean it can’t be negotiated or removed. When in reality, this is a processor markup buried amongst legitimate charges and it’s 100% negotiable.

International Cards Already Cost More For Merchants

Foreign-issued card transactions are already more expensive compared to a domestic sale. They have their own interchange rates, plus the extra card network assessments that we’ve already covered.

Let’s say you’re running a hotel that books lots of rooms from guests traveling overseas.

A $2,000 Visa transaction from a card issued in another country would look something like this:

- Visa Signature Interchange: 1.85%

- Visa ISA Assessment: 0.80%

- Visa IAF Assessment: 0.45%

- Elavon INTL Card Handling: 0.80%

That’s 3.90% in merchant fees to process this card. And it doesn’t even include Elavon’s standard discount rate that they’re charging for each transaction.

When you factor this in, it’s easily going to cost you over 4% to accept this card.

There’s nothing you can do about the extra fees charged by Visa here (1.25% more on top of interchange). But Elavon’s International Card Handling Fee takes an already expensive transaction and inflates it into an amount that’s borderline egregious.

For comparison, a Visa Signature card at a hotel for a domestic credit card would cost you ~$45 for a $2k transaction (2.25% + $0.10 in Visa interchange). The foreign-issued card costs roughly $35 more on a single booking when you include the extra assessments and Elavon’s additional markup.

What Types of Merchants Are Most Affected

Any business using Elavon that regularly accepts foreign-issued cards is exposed to this fee. But merchants in certain industries should definitely be paying more attention:

- Hotels and resorts

- Airlines and travel agencies

- Restaurants (particularly in tourist-heavy areas)

- Retailers in tourist metros

- Ecommerce merchants selling outside of the US

It’s worth noting that businesses don’t need to think of themselves as “international” to be affected by this rate.

If you operate anywhere with meaningful tourist traffic (beach boardwalk, major city, near a national park, etc.), you’re likely processing more foreign-issued cards than you realize.

For example, NYU has over 27,000+ international students on its campus. So if you’ve got a bookstore, cafe, convenience store, or bagel shop near Greenwich Village in Manhattan, you’re probably catering to a high volume of students paying with cards issued in another country.

Can Elavon’s International Card Handling Fee Be Negotiated?

Yes, and that’s probably the biggest takeaway about this fee.

Legitimate card network assessments are non-negotiable. What Visa charges for ISA or what Mastercard gets for its cross-border fee, those go straight to the networks no processor can eliminate them on your behalf.

But Elavon’s International Card Handling Fee is different. It’s a processor markup, which means:

- It goes directly to Elavon.

- It’s not tied to any markup.

- It can be negotiated down or removed completely from your statements.

Here at MCC, we’ve successfully helped our clients eliminate the International Card Handling Fee by negotiating directly with Elavon on their behalf.

It’s just one of several different Elavon merchant fees that we know how to remove from statements. And for one of our clients, we saved them $60k annually by identifying overages from Elavon and negotiating their removal.

How much are you overpaying? It could be a lot more than just the international card handling fee. Get a free audit to find out, and if we find overages, you won’t have to switch providers to save money.

{kind=link}