If your business processes any foreign-issued Mastercard payments, the network will charge your processor extra assessment fees that will ultimately be passed through to your account. This is common for hotels, e-commerce stores, or any business operating in tourist locations that attract international customers.

But some of you might be wondering why you have multiple international assessment fees from Mastercard on your statement.

Are they legit? Is this a mistake? Or is your processor taking advantage of you?

The short answer:

- Mastercard has two legitimate international assessment fees.

- MC International Acquirer Program Support Fee — 0.85%

- MC International Cross Border Fee — 0.60% to 1%

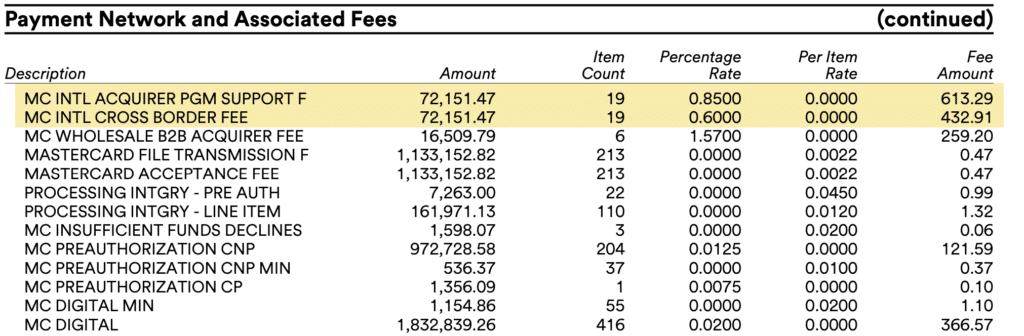

- Both fees often apply to the same transactions, so most merchants processing foreign-issued Mastercards pay a combined 1.45% in international assessments.

- Some processors disguise their own markups as network assessments, but unlike the two above, these are junk fees that can be negotiated away.

MC International Acquirer Program Support Fee

Mastercard’s Acquirer Support Fee is 0.85% and applies to transactions that are:

- Paid with a Mastercard issued in another country

- Settled in the United States

- Settled in US dollars

For example, if your business is located in the United States but a customer pays with a Mastercard that was issued in France, you’ll be hit with this 0.85% assessment.

MC International Cross Border Fee

Similarly, Mastercard’s International Cross-Border Fee applies to Mastercard transactions acquired in the US where the card was issued outside of the US.

- 0.60% for transitions settled in USD

- 1% if settled in a foreign currency

This is Mastercard’s foundational cross-border charge, and it reflects the cost of routing a transaction across different countries and currency environments.

Why Two Fees Instead of One?

Merchants often ask me why Mastercard doesn’t just roll this into a single international fee. And it’s a legitimate question.

The reason is mostly structural. The Cross-Border fee is triggered based on the country mismatch between the merchant and cardholder’s issuing bank, whereas the Acquirer Program Support Fee is tied to how acquiring banks are structured for US-based merchants processing foreign-issued cards.

Mastercard designed them as separate levers so they can be adjusted independently (by region, program, currency, etc.) without overhauling a single fee.

From a merchant’s perspective, the practical effect is the same. Both of these fees will likely show up on the same transaction volume, totaling 1.45% in international assessments from Mastercard. Here’s an example:

It’s also worth noting that your international transactions still count toward your total Mastercard volume, so the standard 0.14% credit assessment is applied on top. That’s 1.59% in assessment fees on these transactions before you factor in the interchange rate and processor markup.

Other “Mastercard” International Fees on Your Statement

If you spot any international-related Mastercard fees on your statement beyond these two, it’s a red flag. Mastercard only charges two international assessments, meaning anything else is coming from your processor.

And some processors are extremely deceptive about this, even itemizing the fee alongside other legitimate card network fees.

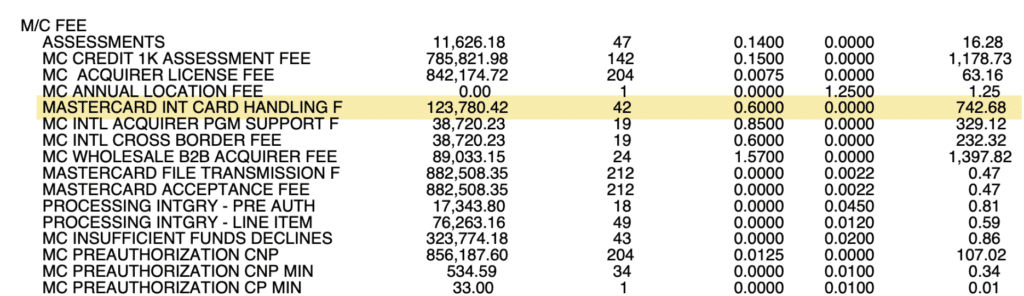

Check out this example from an Elavon statement showing a Mastercard International Card Handling Fee:

Despite being listed alongside other Mastercard fees (including the two international assessments directly below it), this is NOT a legitimate network assessment.

That’s how tricky processors can be. And the only way for you to immediately recognize this as a junk fee is if you know that Mastercard only charges two international assessments (and this isn’t one of them).

Another red flag is that the volume doesn’t match. This International Card Handling Fee is applied to 42 transactions totaling $123,780.42. But both legitimate Mastercard international assessments only hit 19 transactions for $38,720.23. If it were a real Mastercard assessment, the volume would be identical.

What To Do If You’re Seeing Extra International Fees

The two Mastercard international assessments covered in this post are legitimate and non-negotiable. Every merchant processing foreign-issued Mastercards pays them.

But if your statement shows an International Card Handling Fee or any other international-sounding line item from Mastercard that doesn’t match the two fees above, you’re likely being overcharged by your processor.

And because these markups are designed to blend in with legitimate network fees, most merchants never catch them.

So if you’re unsure about a particular charge or just want to make sure your processor isn’t taking advantage of you, reach out to MCC for a free statement audit. We’ll identify any markups disguised as network fees, and negotiate directly on your behalf to get them removed and refunded.

{kind=link}