Despite its small size, Rhode Island has some pretty specific rules when it comes to credit card surcharges. While other states either completely ban surcharging or allow it without restrictions, Rhode Island takes a middle-ground approach—surcharging is legal, but there are detailed requirements that merchants must follow to comply.

If you’re a business owner in Providence, Newport, or anywhere else throughout the Ocean State, understanding these rules is crucial before you consider implementing any form of a surcharge program. And if you’re a consumer in Rhode Island, knowing the law can help you navigate extra fees you might encounter during checkout.

Disclaimer: This information is for reference only, and it does not constitute legal advice. Consult with an attorney with any legal-specific questions.

Is Credit Card Surcharging Legal in Rhode Island?

Yes, credit card surcharging is legal in Rhode Island. But the state heavily regulates this practice under specific legislation.

In short, Rhode Island allows credit card surcharges but requires merchants to follow the detailed disclosure requirements that are outlined in RI SB925. This includes displaying the total price for paying by credit card (including the surcharge fee) and clearly posting notices of the surcharge at multiple points on-premises.

This makes Rhode Island one of the more regulated states when it comes to surcharge implementation. You can do it, but you need to do it right to stay within the law.

Can Merchants Surcharge Debit Card Transactions in Rhode Island?

No, debit card surcharging is illegal in Rhode Island (just like it is in all 50 states).

This is a federal regulation that applies nationwide, regardless of what individual state laws say about credit card surcharges. Even if a debit card is processed as a “credit” transaction (signature-based rather than PIN-based), it still cannot be legally surcharged.

So while Rhode Island gives merchants the ability to surcharge credit cards under certain conditions, debit cards are completely off-limits.

Understanding Rhode Island’s Credit Card Surcharge Laws (Full Details)

Rhode Island’s approach to surcharging is a bit more complex compared to the surcharge laws in other states. Here’s everything you need to know:

Dual Pricing Requirements

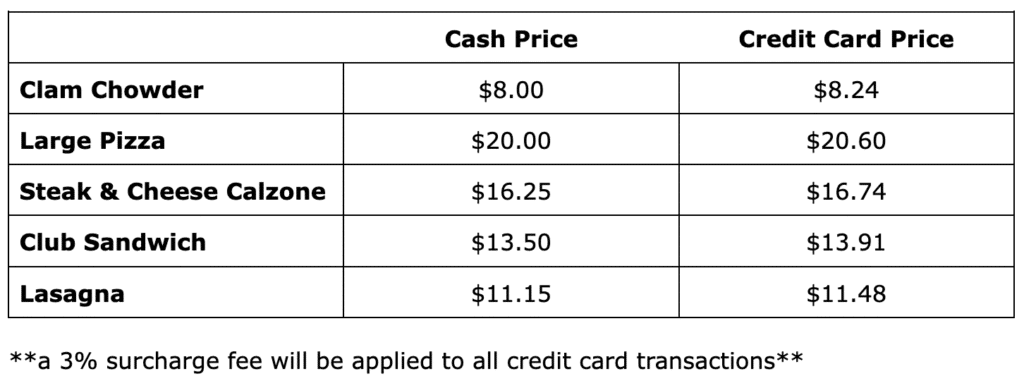

Rhode Island requires dual pricing displays to ensure customers understand the cost difference between paying with a credit card compared to other payment methods. This means you can’t just add a surcharge at the point of sale—you need to show both prices upfront.

For example, let’s say you’re imposing a 3% surcharge on credit cards. You’d have to display something like this:

This is all about transparency and ensures that the customer knows exactly how much they’re going to pay regardless of the payment method.

Any applicable sales taxes do not need to be included in either price.

Mandatory Notice Requirements

SB925 also requires Rhode Island merchants to post notice of the surcharge program at points of entry and at the point of sale. This notice must be posted clearly in a minimum of size 16 font and displayed in prominent locations.

The notice must also contain an explanation of the surcharge, the amount of the surcharge, and which credit cards are subject to additional fees.

Basically, you can’t have this fine print buried or hidden away. The state wants to protect consumers so they can make informed decisions about how to pay and how much everything costs.

Receipt Documentation Requirements

In addition to displaying a notice of the surcharge in multiple locations throughout the premises and listing credit card prices alongside cash prices, merchants also need to itemize surcharge fees as separate line items on all receipts.

This creates a paper trail and ensures customers know exactly what they paid for even after the transaction has been processed.

Disclosure Requirements for Online and Phone Transactions

SB925 has separate rules for online and phone transactions.

Obviously, signage posted at the point of entry doesn’t apply in these scenarios. But full disclosure of the surcharges must still be provided to the consumer.

On websites, surcharge disclosures must be displayed on the homepage and at the point-of-sale checkout page.

For phone transactions, surcharge disclosures must be verbally provided to the customer prior to the sale being processed.

Federal Laws and Card Network Rules Still Apply

The maximum allowable surcharge fee is 4% in Rhode Island, which aligns with federal limits.

But it’s worth noting that every card network has its own rules for surcharging. While these technically aren’t laws, and you can’t be held legally liable for violating them, the card networks can still fine you for violating terms of your merchant agreement.

For example, Visa caps surcharges at 3%. Amex and Discover both require surcharges to be applied equally to call cards—effectively limiting you to 3% to stay compliant with card network rules.

The History of Rhode Island’s Credit Card Surcharge Laws

Rhode Island lawmakers haven’t always seen eye-to-eye on surcharging.

Back in 2013, RI Attorney General Peter F. Kilmartin actually supported a bill that would prohibit surcharging altogether (2013 H5213). The bill ultimately failed, but the AG cited consumer protection concerns and a competitive disadvantage compared to neighboring states like Connecticut and Massachusetts (where surcharging is illegal).

The following year, 2014 H7007 was another attempt to restrict surcharging—allowing cash discounts but not allowing merchants to charge more than the listed price for consumers paying with credit cards. AG Kilmartin was, again, in support of this legislation.

Here’s his direct quote: “Rhode Island consumers should not be penalized with a four percent surcharge simply for paying with credit cards. It is imperative that we take steps to protect our consumers from that possibility.”

Again, this attempt failed.

The state eventually moved toward allowing surcharging but heavily regulating it, which led to the current system under SB925.

Rhode Island Surcharge Compliance Checklist

If you’re running a business in Rhode Island and considering a credit card surcharge fee, there are several steps you need to take to ensure compliance. Here’s a quick checklist that you can use as a reference:

Before You Start

- Notify your payment processor at least 30 days before implementing surcharges.

- Provide written notice to the card networks at least 30 days before surcharging.

- Ensure your point-of-sale system can handle surcharge fees on credit card transactions (without accidentally surcharging debit cards).

- Update your price lists to contain dual pricing.

- Create clear signage for your physical locations.

- Update your website with surcharge disclosures.

Ongoing Requirements

- Prominently display both cash and credit card prices.

- Post notices at store entrances and points of sale.

- Clearly itemize surcharges on all receipts.

- Keep surcharges within federal and card network limits.

- Apply surcharges equally to all types of credit cards.

What to Avoid

- Surcharging debit cards.

- Exceeding 4% (federal law) or 3% (card network limits).

- Any hidden or surprise fees at checkout.

- Using surcharges to profit as opposed to recovering costs.

How to Report Surcharging Violations in Rhode Island

If you’re a consumer who encounters what you believe is an illegal surcharging practice in Rhode Island, you can report violations directly to the state’s attorney general’s office.

Examples of violations include:

- Surcharging on debit cards.

- Fees exceeding allowable limits.

- Hidden surcharges not properly disclosed.

- Misleading or deceptive pricing practices.

You can file a complaint online here.

Rhode Island businesses found in non-compliance with SB925 can be fined up to $500 per violation.

We’d also like to hear about any surcharges you’ve experienced in the state of Rhode Island. While we don’t offer any consumer services here at MCC, we’ll pass your feedback along to merchants we work with in your state. So drop a comment below and tell us how you feel about all of this.

Final Thoughts on Rhode Island’s Surcharge Laws

Overall, Rhode Island has a balanced approach to credit card surcharging. They allow businesses to recover processing costs while still attempting to protect consumers through transparency.

But implementing a compliant surcharge program in Rhode Island requires significant attention to detail and ongoing maintenance. Between dual pricing mandates, signage, and receipt documentation, there are added administrative burdens that can increase your costs and potentially offset what you’re attempting to recover.

More importantly, you could lose customers. In a small state like Rhode Island where word of mouth and customer loyalty are crucial for success, pushing your customers away to recoup a few percentage points may not be worth it.

If you’re struggling with high credit card processing costs, you can look to alternative solutions prior to implementing a surcharge program. The first thing you should do is attempt to lower your rate with your existing processor—allowing you to achieve similar savings without the compliance headaches or lost customers.

Here at MCC, we can help you reduce your processing costs without implementing a surcharge program or changing providers. We’ll audit your statements, identify areas for savings, and negotiate directly with your processor on your behalf. Contact our team today for a free assessment.

{kind=link}