Simple isn’t always better. And with Shift4’s “Simple Change” pricing, it’s definitely not cheaper.

Shift4 is actually a decent processor in terms of their technology, support, integrations, and overall services offered. But we find merchants consistently overpaying by 20-40 basis points when they’re enrolled on Simple Change pricing vs. true interchange plus.

It may not seem like much, but if you’re a restaurant doing $500k per month, 30 basis points translates to $18k annually in overages. Or if you have a hotel averaging $2M per month, you could be overpaying by $70k+ every year.

Read on to find out exactly what Simple Change is, how it’s different from interchange-plus, why it costs more, and what you can do about it. I’ll also walk you through some real Shift4 statement examples and compare them against actual published rates from the card networks.

Key Takeaways

- Simple Change pricing is NOT true interchange-plus.

- It’s a bucketing system from Shift4 where they assign rates to aggregated transaction categories with markups built in.

- Shift4 also charges an additional discount rate on your total volume, so they earn a margin from two layers.

- Merchants who switch from Simple Change to IC+ can have their effective rates cut in half.

- You don’t need to leave Shift4 to save money. The pricing model can be negotiated with them directly.

What Exactly is Shift4 Simple Change Pricing?

Simple Change is Shift4’s proprietary pricing model that groups transactions into broad categories and assigns a single rate to each bucket for billing purposes.

Instead of passing through the exact interchange rates the card networks set for each card type and transaction condition, Shift4 creates their own aggregate rate for that category of cards.

The result is a statement that looks clean and easy to read, with processing detail that typically fits on a single page. You’ll only have a handful of line items per card type, grouped into categories like “Visa Other” and “Mastercard Card Present” with a single rate and dollar amount next to each one.

And for many merchants, this simplicity is appealing, and that’s how Shift4 presents this as if they’re doing you a favor. But they’re not.

While fewer rates are being shown, this consolidation allows Shift4 to inflate your rates into “catch-all” buckets while obscuring the true costs you should be paying.

Two Components of Simple Change

There are actually two separate layers of charges built into Shift4’s Simple Change accounts.

Layer 1 – Inflated Bucket Rates

Each transaction has a rate assigned to it by Shift4, which is higher than the actual interchange rate published by Visa or Mastercard for the cards in that bucket.

The gap between what Shift4 charges for a bucket and what the card networks charge as interchange is where Shift4’s markup is hidden.

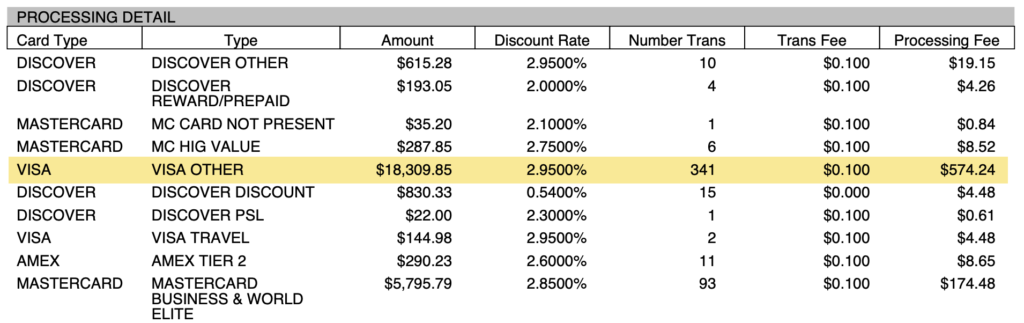

Here’s an example of a Simple Change statement, with “Visa Other” highlighted, charged at 2.95% + $0.10 per transaction:

This amount and description doesn’t match anything when we compare it against Visa’s published interchange rates.

All we know is that there are 341 transactions on $18,309.85 in volume, but the label doesn’t tell you anything about which Visa card types are actually on it. On a true interchange-plus statement, each of those line items would appear as its own card type that matches Visa’s published rate.

But here, they’re all bundled into a catch-all category that’s significantly marked up.

This is a restaurant, and those rates start as low as 2.10% per transaction. That’s a markup of at least 85 basis points for the lowest cards in this category, and potentially more depending on what types of cards are actually inside the bucket.

Layer 2 – Additional Discount Rate on Gross Volume

On top of the bucket rates, Shift4 applies an additional discount rate that’s charged separately on the entire processing volume for each card brand.

This approach effectively allows Shift4 to double-dip on their markup.

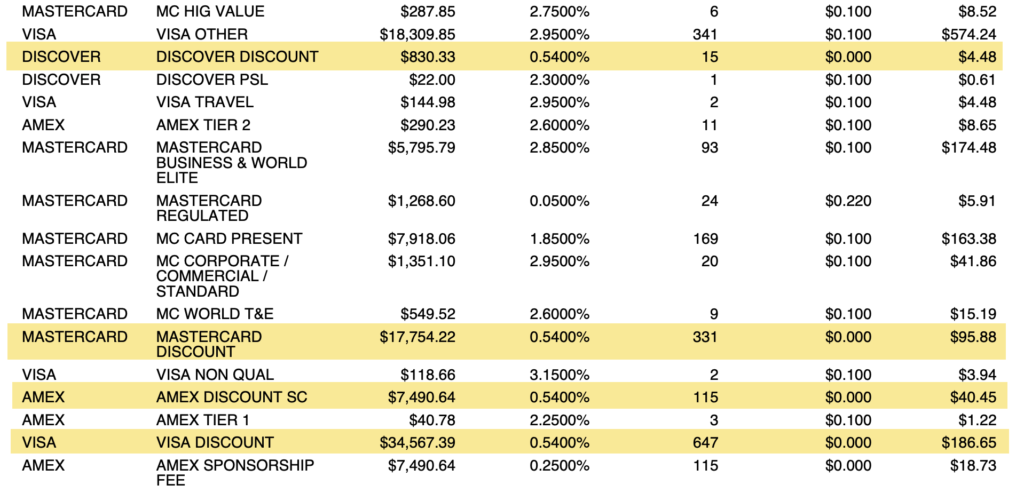

Here we can see Shift4 charging a 0.54% discount rate, itemized by total volume per card network, on this Simple Change statement:

The problem with this is that there’s already margin built into buckets (layer 1).

It should be one or the other, not both. That’s why statement transparency is so important for getting good rates. And while Simple Change is easier to read, the lack of transparency makes it easy for Shift4 to bury more margin in a way that’s nearly impossible for you to detect.

I also want to point out the Amex Sponsorship Fee at the very bottom of this screenshot. That’s an extra 0.25% going directly to Shift4, making the total markup on American Express transactions to 0.79% (and that doesn’t include the margins built into the aggregate buckets).

Simple Change vs. Interchange Plus

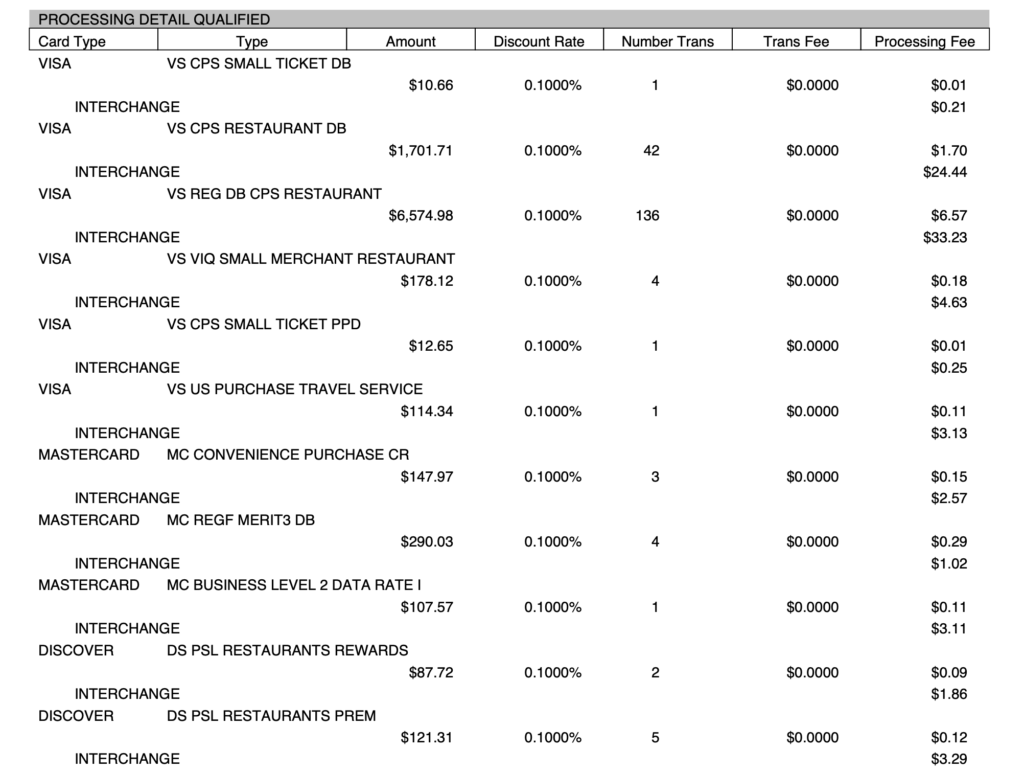

Here’s what that same merchant’s statement looked like after our team switched them to true interchange plus pricing with Shift4:

You can instantly see the difference here compared to the Simple Change statement we analyzed earlier.

- Each transaction type exactly matches a card network interchange category and the accurate published rate.

- The interchange fees and Shift4’s markup both are itemized individually for each card type in the far right column.

- The IC+ breakdown runs across several pages, whereas the Simple Change statement fits on a single page with broad buckets.

What you need to understand here is that the length of the interchange-plus statement is not a problem.

This is exactly what we want to see. It’s all about transparency, and that’s the whole point of what we’re trying to accomplish to get a good rate. You can’t hide additional markups this way because everything is being passed through to you at the wholesale cost.

How Much Money You Can Save By Switching to Interchange-Plus

Switching from Simple Change to interchange-plus results in actual savings. It’s more than just a more detailed statement breakdown.

Here are a few other specific examples that illustrate this point:

- The “Visa Other” bucket from the Simple Change statement is now broken down into over a dozen distinct categories (at much lower rates)

- Mastercard’s commercial cards that were all bucketed at 2.95% now qualify for actual published rates (like MC Business Level 2 Data Rate 1 at 2.65%).

- Shift4’s 0.54% discount rate on gross volume is gone, and replaced with a low basis-point markup on top of the actual interchange rate (0.10%).

The details may seem minor, but the savings here are massive.

Just look at the Mastercard commercial example I called out above. The Simple Change markup was 84 basis points (0.54% discount + 0.30% margin baked into the bucket).

- Once this merchant moved to IC+ pricing, the discount rate dropped to 10 basis points.

- Their effective rate was 5.31% on Simple Change.

- And it was slashed by more than half to 2.33% after switching to interchange-plus.

You don’t have to change providers to get these savings. Shift4 offers IC+ pricing, you just need to negotiate and ask them for it.

Not Everything is Inflated on Simple Change Statements

I want to make it clear that every line item on your Shift4 Simple Change statement is not inflated.

This is a crucial callout because if you’re just spot-checking a few lines, you might see that they match with true interchange categories and assume that everything is fine on your statement.

For example, on this particular statement we audited, the regulated debit card transactions were passed through at the correct cost. All of the network assessments were also charged the correct rates Visa Base II Transmission Fee, Mastercard NABU Fee, etc.) without any padding from Shift4.

If you’re unsure whether the rates you’re paying are accurately passed through, you can send us your statements for a free audit, and we’ll let you know.

How to Tell if You’re on Simple Change

Pull out your last Shift4 statement and look for any of these signs:

- Processing details fit on one page.

- Line items use generic names like Visa Other or Mastercard Card Present.

- Separate discount lines appear for each network (Visa Discount, Discover Discount, etc).

- The letters “SC” might appear next to a discount line, like Amex Discount SC (the SC stands for Simple Change).

- Each transaction category has a single fee charged in far right column (it would be two if you were on IC+),

Statements like this can guarantee you’re overpaying by at least 20 basis points (probably more). We consistently see Simple Change accounts being overcharged, and I’ve yet to see a Shift4 statement that didn’t have extra margin built into the Simple Change buckets.

Is It Worth Staying With Shift4?

Some merchants feel like they’ve been duped when they realize how Shift4’s pricing structure costs them tens of thousands of dollars in extra merchant fees. It’s a natural response, and I can see why you’d at least want to consider dropping a provider who you feel deceived by.

But don’t switch.

Shift4 is actually a good processor. Billing tricks are unfortunately just standard practice throughout the payment processing industry, and Shift4’s Simple Change structure is actually less egregious than tactics we’ve seen from other providers.

You can get a much better rate and lower your credit card processing fees by simply negotiating better terms with Shift4.

Tell them you want to move from Simple Change to interchange-plus, and demand a fair rate.

We’ve had tons of success negotiating with Shift4 on behalf of our clients. So I can tell you from my first-hand experience that they’re receptive to these negotiations. They don’t want to lose your account, and they’d rather settle on a 0.10% or 0.20% margin instead of losing you altogether.

The fix isn’t complicated, and a new processor doesn’t solve your problems. Just change your billing structure, and keep all of your existing systems, terminals, and integrations in place with Shift4.

{kind=link}