Self-storage operators using or considering Storable software have a few different options to choose from for integrated payment processing.

Each one is very different in terms of the structure, company behind it, control, and most importantly, implications for your pricing.

This post breaks down exactly what you need to know about each processor so you understand what you’re working with. And if you’re already using one of these providers, I’ll explain how you can lower your costs without changing anything.

Option 1: Storable Payments

In addition to being the software provider, Storable doubles as a credit card processor with its in-house solution for payment acceptance.

Naturally, this is the option that Storable steers its customers toward because it’s the most profitable option for them (not necessarily for you).

Our experience helping audit Storable statements on behalf of our clients has been mixed. Some self-storage companies are getting good rates, while others are not.

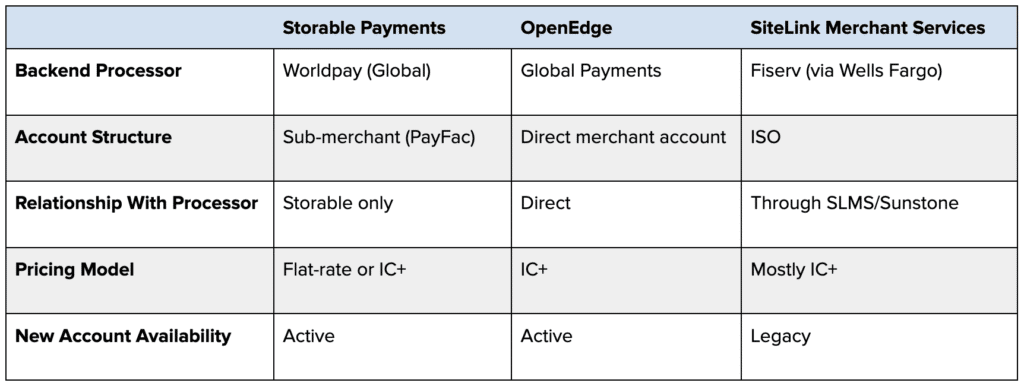

- Storable operates as a PayFac, powered by Paytrix Pro from Worldpay.

- IC+ pricing is available, but some sales reps try to push flat rate.

- Multi-location businesses often have inconsistent rates and structures for each facility (which should not be the case).

- Statements are easy to understand, but not always 100% transparent.

- Onboarding is straightforward and support is solid, with everything handled under one roof from Storable.

This setup is uniquely different from other integrated processing options in which the software provider simply supports the API for a third-party provider.

Even though Storable is leveraging Worldpay for Platforms on the backend, Storable is your processor — not Worldpay. Storable onboards you through a sub merchant account, and you don’t have any direct line to Worldpay when it comes to rate negotiations or fee structures.

Structuring things this way guarantees your rates will always be slightly inflated because Storable needs to earn enough margin to compensate Worldpay while still profiting.

That said, Storable is flexible on pricing and is willing to negotiate if you know how to ask the right questions (or demand your needs). So there’s definitely savings opportunities here, even for existing Storable users who are already set up for payment processing.

Option 2: OpenEdge

OpenEdge is a third-party processing solution that’s owned by Global Payments.

This setup with Storable is more traditional for integrated processing. If you’re using Storable Edge or SiteLink, you have the option to integrate OpenEdge for credit card processing.

- Your merchant account and contract are directly from OpenEdge.

- Storable simply supports the API to integrate, but has nothing to do with your rates.

- OpenEdge has modern technology and everything you need to accept payments.

- But they’re known for increasing rates on your account over time.

- They’re also notorious for junk fees and hidden markups that quietly inflate your effective rate.

The OpenEdge option is a bit of a double-edged sword.

On one hand, having a direct relationship with your processor cuts out a middleman and puts you in a position to get better rates, which would normally be better than the PayFac model from Storable. The trade-off is that OpenEdge can be one of the most expensive providers on the market if you’re watching your rates like a hawk.

We’ve seen this dozens of times from merchants in every industry. OpenEdge will try to get away with charging you as much as possible. And if you don’t catch it or push back, you’ll literally end up overpaying by tens of thousands every year.

It’s also worth mentioning that as of January 2026, Global Payments completed its acquisition of Worldpay (powering option #1 above). Even though Storable controls your rates if you use Storable Payments, it’s still important to understand that two of these three processing options now have the same parent company.

Option 3: SiteLink Merchant Services (SLMS)

This is the most layered structure of the three, and worth unpacking carefully. I also want to call out the fact that very few new accounts will probably be onboarded with this setup.

But if you’re currently using SiteLink Merchant Services with Storable, this can help you make sense of what’s happening behind the scenes with your integrated payment processing.

- SiteLink merged with Storable years ago, but SiteLink Merchant Services is legally a separate entity.

- SLMS is a DBA of Sunstone Merchant Services.

- Sunstone is a registered ISO of Wells Fargo Bank, and First Data (Fiserv) reseller.

- This is an ISO model, where merchants have a traditional account, but SLMS sits between you and the acquiring bank.

- Fiserv is technically your backend processor here, even though there are multiple layers in between.

SLMS is currently still listed as a supported integration partner on Storable’s website. But the actual button to sign up and proceed with this option is greyed out and unclickable.

It appears as though anyone interested in this setup is instead being pushed towards option #1, Storable’s in-house PayFac model.

Existing SLMS accounts have been pitched “upgrades” (which is Storables way of getting them to switch). And while we almost never recommend switching providers, continuing to use a legacy processing option that’s being phased out is likely not a good thing for your business.

Before you switch, I encourage you to send our team some of your SLMS statements for a free audit. If switching makes sense, we can help you negotiate directly with Storable to ensure you’re getting a fair rate and compensated accordingly for the inconvenience.

They may try to get you on a flat-rate plan or something unfavorable for your business during the switch.

How the Three Options Compare

The biggest difference between these three options comes down to who’s actually processing your payments, what kind of account you have, and how much leverage you realistically have to negotiate.

What This Means For Your Rates

The structure of your integrated processing setup directly impacts your pricing because it affects your leverage, who you can call, and what’s negotiable.

All three options are negotiable, but your approach will vary for each.

Option #1 – Storable: In this case, you need to go directly to Storable to negotiate better rates. It’s tricky because they’re also providing you with the software, and reps can often trick you into thinking you’re saving money in one place while making up for it elsewhere.

Storable’s statements aren’t always the most transparent, either. So it can be difficult for you to identify everything you’re paying without having your account reviewed by an expert merchant consultant.

Option #2 – OpenEdge: Since OpenEdge maintains your merchant account, they control your rates. Theoretically, this should be a good thing because the fewer players involved means less mouths to feed, which should translate to lower rates.

But OpenEdge is one of the most egregious processors on the market when it comes to its billing practices. Beyond your base rate per transaction, if you spot any of the following fees on your statement, it’s a sign you’re overpaying:

- Risk Assessment Fees

- Settlement Funding Fees

- Analytics Reputation Management Fees

- OpenEdge Check Fees

- PCI Non Compliance Fees

- Bank Deposit Service Fees

Option #3: SLMS: SiteLink Merchant Services doesn’t have much incentive to offer you competitive rates because they’re effectively being phased out and merging with Storable as its new parent company.

This means that existing accounts that might currently be getting fair rates can end up with worse pricing after a migration. I strongly suggest that you have an expert help you during any transition to ensure you’re not getting ripped off during the transition.

Which Integrated Processing Option is Best For Storable?

It’s honestly a toss up between Storable Payments and OpenEdge.

Normally, I’d say go for the direct agreement with a merchant account provider (OpenEdge) instead of the PayFac model (Storable Payments).

But I can’t recommend OpenEdge in good faith to anyone. I’ve just seen too many merchants get burned over the years using them, and that’s for non-integrated setups. The integration gives OpenEdge even more excuses to overcharge you.

That said, you can still get good rates from OpenEdge if you’re cautious with your account and understand what fees are legit vs. junk. If you get all of the junk fees removed and negotiate a fair discount rate, you can end up with a solid deal.

If you go with Storable payments, make sure you’re on a true interchange-plus plan instead of flat-rate. But know that IC+ doesn’t guarantee you’re getting a good rate. You still need to negotiate the best possible terms.

And for multi-location storage businesses, double-check that your pricing is consistently applied across each facility.

Should You Switch Providers?

Unless you’re currently using SLMS with Storable and you’re being forced to migrate, there’s no reason to switch providers.

Whether you’re using Storable or OpenEdge, you’re better off sticking with your current setup and reviewing your account for savings opportunities. With either provider, there are likely inflated rates and extra fees that can be removed. Many of these are significant, and can represent thousands and savings every month.

For those of you already set up with a payment processor that doesn’t integrate with Storable, I don’t think the benefits of going integrated outweigh the drawbacks of switching.

Storable pitches a really clean offering, especially if you go with their payment processing option. But the integrated path is expensive.

You actually have quite a bit of leverage here with your current processor because you’re looking for something that they can’t support. So they’re more likely to bend in your favor in order to keep your account. Use this leverage to your advantage and demand better rates.

Then you can always use some sort of third-party workaround or data push/pull to consolidate your payment info with customer data in Storable.

{kind=link}