Once you get in the habit of auditing your monthly credit card processing statements, it’s worth it to start verifying some of the “smaller” charges, too.

Visa’s Base II Network Access Fee is a good example.

It’s not going to cost you thousands per month. But understanding where this fee comes from, how much it is, and when it applies, and if it’s legit, is all part of the ongoing education that will ultimately help you spot bogus fees on your statement.

This fee in particular is often misunderstood because it sounds nearly identical to other charges. Some statements have it, others don’t, and you’ll even find processors lumping it together with other Visa assessments.

Let me clarify everything for you below.

What is the Visa Base II Network Access Fee?

Visa’s Base II Network Access Fee (sometimes called the Settlement Network Access Fee or simply Visa Base II Fee) is an assessment that Visa charges whenever a transaction is submitted to its settlement system for clearing.

The current Visa Base II Network Access Fee is $0.0025 per settled transaction.

To help you understand where this fee comes from, you need to know a little bit about Visa’s network architecture. Visa’s global processing platform is called VisaNet, which has two main components:

- Base I — Authorization and clearing system that approves or denies transactions in real time.

- Base II — Clearing and settlement system that actually moves money after the sale.

So every time a merchant accepts a Visa card and that transaction settles (meaning money is moved), it passes through VisaNet’s Base II system and Visa charges a small fee for that access.

Who Pays the Base II Network Access Fee?

The Base II Network Access Fee applies to all US-based Visa settlement transactions.

Essentially, if your business is in the US and you accept Visa cards, you’re paying this fee on every transaction.

The fee is technically billed to the acquiring bank (the merchant’s payment processor), and then passed through at cost to the merchant on monthly statements.

It’s a flat rate, meaning the amount of each Visa transaction doesn’t impact the cost. For example, if you have 2,000 Visa transactions in a month, you’ll pay a $5 Visa Base II Network Access fee whether those transactions totaled $20,000 or $200,000 in sales.

The fee is non-negotiable. Visa sets the rate, and your processor cannot remove it or reduce it.

What your processor can do is choose how to pass it through to you. Some processors pass it through at cost, others pad it (which they shouldn’t), and many bundle it with other Visa assessments under a generic “Visa fees” line item that obscures what you’re actually paying.

You won’t see this fee if you’re using a flat-rate processor like Square, Stripe, or PayPal. All of your assessments have already been baked into the flat rate you’re paying. That doesn’t mean it doesn’t apply to you (you’re absolutely still paying for it), but it’s “invisible” because your processor has already marked up your rates enough to account for it.

How to Spot the Base II Network Access Fee on Your Statement

Processors don’t all use the same fee names, which is part of what makes it so difficult for merchants to audit assessment fees. Here are some of the variations you might see on your account:

- Visa Base II Fee

- Visa Base II Network Access Fee

- Visa Settlement Network Access Fee

- Visa Network Access Fee

- Base II Access Fee

- VS Base II Net Access

Basically, any combination of Visa with Base II and Network Access that’s being charged at $0.0025 per settled transaction. If you see that rate, regardless of what it’s called, it’s most certainly that this fee.

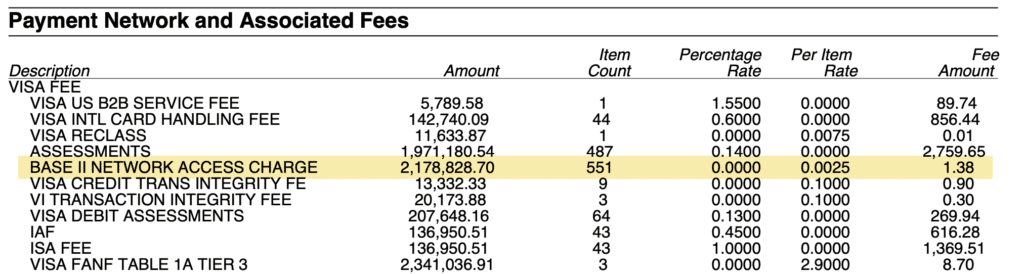

Here’s an example from one of our client’s statements:

As you can see, the total fee amount is just $1.38 on over $2 million in Visa volume for this period. Again, that’s because it’s a flat rate per transaction, and not based on the total settled.

In this case, there were 551 applicable Visa transactions charged at $0.0025 each, so the math checks out at $1.38.

Why the Base II Network Access Fee Matters

A $0.0025 per transaction fee seems trivial. As shown from the example above, you could literally be processing millions of dollars per month and the fee may not even cost you a couple of dollars.

So why waste your time on it?

Because you need to be auditing every single assessment on your statement. That’s the only way to tell if your processor is charging you fair rates.

Even if your processor doubled or tripled this rate on you, it still won’t amount to much money. So you may not think it’s worth doing anything about.

But if your processor is willing to pad such a small charge, I can all but guarantee they’re overcharging you elsewhere.

The point I’m trying to make is that every fee on your statement is important. In isolation, it may not seem like much. But in the big picture, it could be a sign of thousands in overpayments elsewhere.

Plus, processors have become so good at coming up with fee names that sound legit but actually aren’t. Just because “Visa” or another network is in the fee name, doesn’t automatically mean it’s a non-negotiable interchange fee or assessment.

It’s a good idea to double-check all of these names. So you did the right thing by searching for this one, and ultimately verifying its legitimacy.

Final Thoughts

If you think you’re being overcharged by your processor, that’s a big deal.

Small discrepancies with a fee like this one can be the first red flag that ultimately uncovers a lot more hidden on your statements.

So if you’re having trouble identifying those fees on your own or if you need help negotiating with your processor, contact our team here at MCC for a free audit. We’ll help you save money without switching providers to ensure you get the best possible deal on credit card processing.

{kind=link}