Elavon is actually a fairly decent payment processor, and they aren’t nearly as egregious as other providers in terms of bogus fees and deceptive billing.

In fact, Elavon has offered some of the cheapest rates we’ve seen to high-volume merchants.

But even the “good” payment processors aren’t perfect. And Elavon is a prime example of this.

If you’re using Elavon for credit card processing and you find any of the following fees on your statement, it means you’re overpaying. Fortunately, these Elavon merchant fees can be eliminated with the right approach.

Key Takeaways

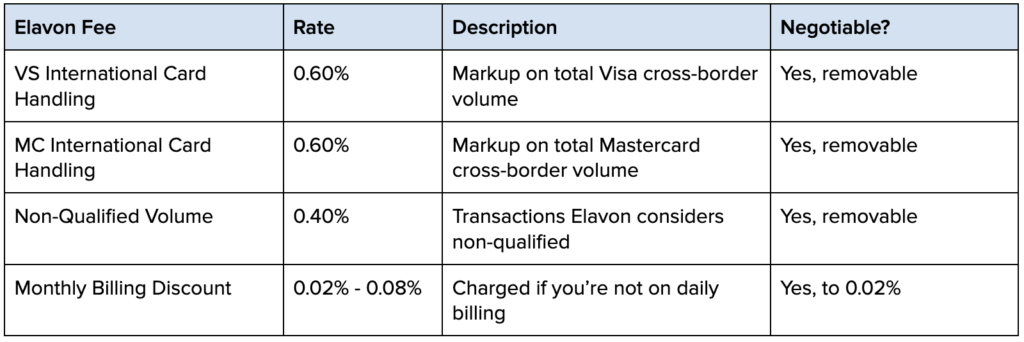

- Elavon charges a 0.60% International Card Handling Fee that is NOT a Visa or Mastercard assessment (it’s a negotiable processor markup).

- Their Non-Qualified Volume Fee (0.40%) is based on Elavon’s discretion and is often arbitrarily applied.

- Elavon’s Monthly Discount Fee has jumped to 0.08% of total volume, and while it’s difficult to fully remove, it can be negotiated as low as 0.02%.

- We saved one merchant over $60,000 annually by negotiating just four fees.

International Card Handling Fees

Despite being itemized under payment network and association fees on Elavon statements, the International Card Handling Fee is NOT a card network assessment. It’s a processor-imposed markup charged on top of cross-border fees from Visa and Mastercard.

For merchants with a high volume of cross-border transactions, this fee can cost you thousands of dollars every month. We typically see Elavon charging it to clients in the hotel and hospitality space, particularly in resorts and locations frequented by international travelers.

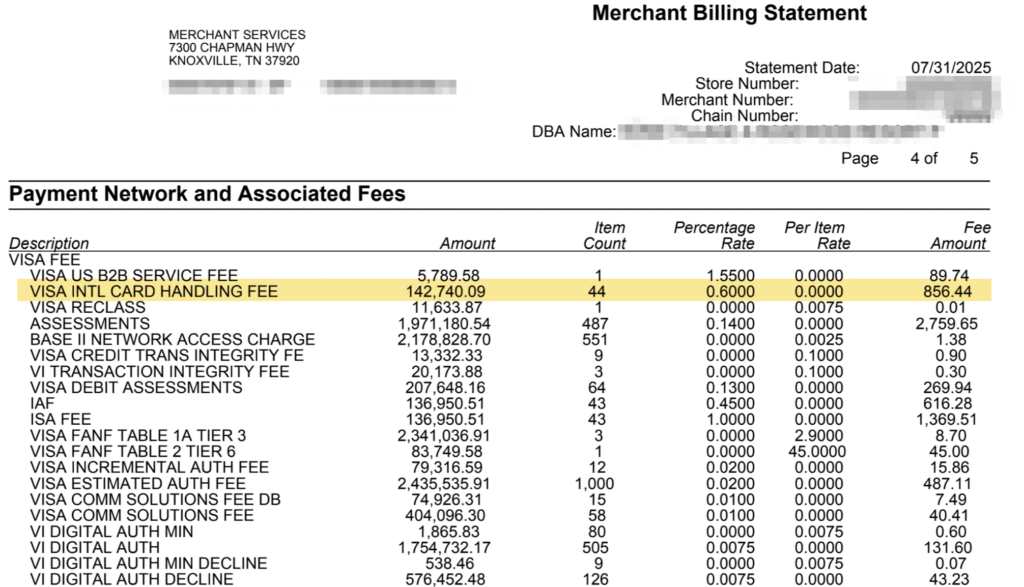

Here’s an example of Elavon charging a 0.60% Visa International Card Handling Fee to one of our clients:

As you can see, it’s buried amongst other Visa assessments and even has “Visa” in the name.

So to the untrained eye, it’s easy to just assume that this is a legitimate charge coming from Visa. But it’s not.

Visa’s International Service Assessment (ISA Fee) is eight lines below this charge. That’s the cross-border markup from Visa. But the INTL Card Handling Fee goes straight to Elavon.

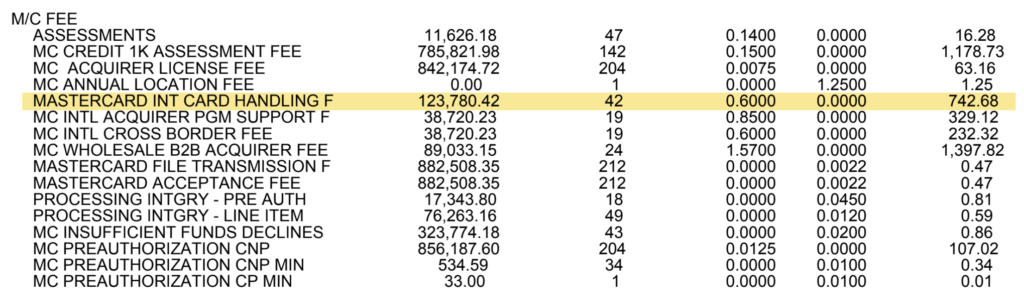

On the same statement, we can find a Mastercard INTL Card Handling Fee as well:

Just like the Visa fee, Elavon is charging 0.60% on total Mastercard international card volume.

The real Mastercard assessments for international cards are the two line items directly below this charge:

- MC International Acquirer Program Support Fee

- MC International Cross Border Fee

Both of these are legit and coming straight from Mastercard. But the MC International Card Handling Fee is a markup imposed by Elavon.

On this statement alone, Elavon overcharged our client by roughly $1,600 in International Card Handling Fees ($856.44 on Visa and $742.68 on Mastercard).

The biggest issue with this fee is that it’s nearly impossible to spot on your own.

If Elavon wants to charge you extra for international transactions, they should be transparent about it. But the way this charge gets itemized tricks merchants into thinking it’s a non-negotiable network assessment, when it’s actually a negotiable processor markup.

Non-Qualified Volume Fee

Elavon charges some merchants an Other Non-Qualified Volume Fee, in which the rate itself and the transactions it applies to are both completely arbitrary.

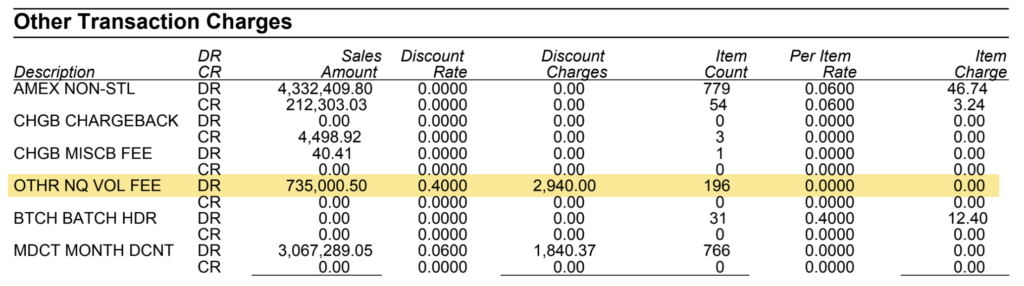

Here’s an example from the same client and statement we used above:

Elavon just decided that $735k of this month’s transaction volume was going to be bucketed into a “non-qualified” tier.

At a 0.40% discount rate, the Other NQ Vol Fee cost this business an extra $2,940 in merchant fees. These charges are going straight to Elavon.

Processors love to use the term non-qualified as an excuse to charge you more money. However, the exact reasoning behind why some transactions get downgraded into a non-qualified bucket are never clear. It’s completely at the processor’s discretion.

And as you can see, they clearly have an incentive to categorize transactions as non-qualified because it’s easy money in their pockets.

This is another fee that’s easy to overlook because it’s just a single line item on a statement with over 100+ other charges. Trying to decipher what’s legit vs. what can be removed isn’t easy, and Elavon is banking on you ignoring this and paying without questioning anything.

Monthly Discount Adjustment Fee

Elavon started charging merchants a Monthly Billing Fee a few years ago. We started seeing this on client accounts back in 2023, being charged at 0.02% of their total monthly volume.

But the rate continues to rise, and as of February 2026, Elavon is charging0.08% for monthly billing.

You can avoid this fee by switching to daily billing, but this creates a reconciliation nightmare for businesses.

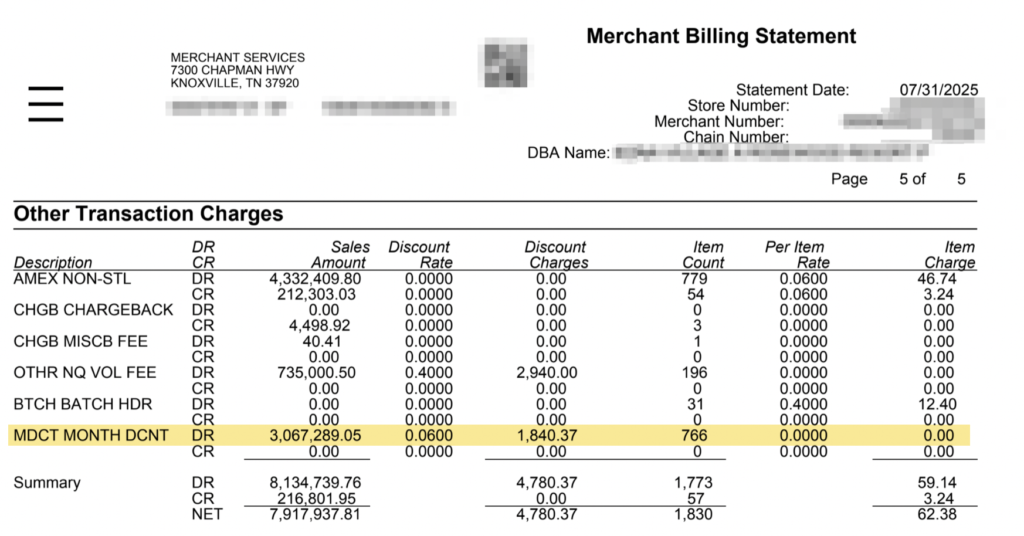

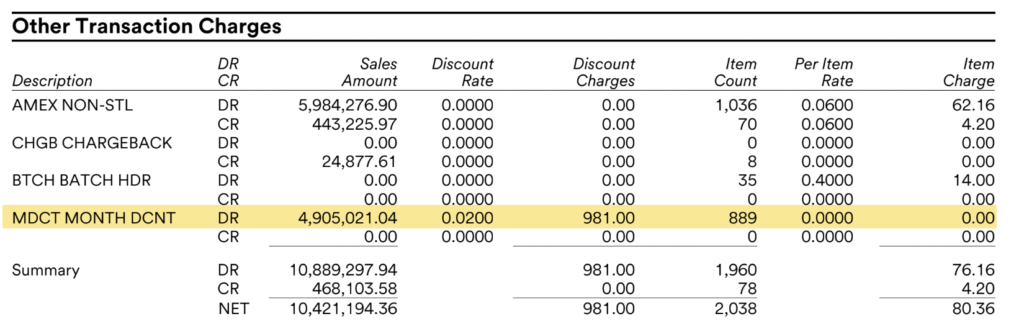

Here’s Elavon’s Monthly Discount Fee highlighted in the other fees section so you can see how it’s itemized:

This statement is from 2025 when the Monthly Billing Discount Rate was 0.06% of total volume, which cost this merchant $1,840.37 in extra fees.

Unfortunately, Elavon is stubborn about this one and won’t always remove it for you altogether if you don’t want to switch to daily billing. That said, we’ve successfully negotiated this rate to a lower amount for our clients.

Here’s a screenshot from the same exact merchant in January 2026, with the fee reduced to 0.02% after our negotiations:

While I’d obviously love to see this eliminated altogether, they’re paying $981 total for this fee on $4.9 million in volume compared to $1,840 on $3 million in volume. So it’s significantly better.

And if you look closely, you can see the Other Non-Qualified Volume Fee has been removed completely on this statement.

How Much These Elavon Merchant Fees Can Cost Your Business

A few extra charges on your monthly processing statement may not seem like a big deal. But when you run the numbers, they add up quickly.

Let’s recap how much the merchant from the examples above was paying, and how much they saved after we negotiated those fees with Elavon on their behalf.

- VS INTL Card Handling – 0.60% – $856.44

- MC INTL Card Handling – 0.60% – $742.68

- Other NQ Volume – 0.40% – $2,940

- MDCT Month DCNT – 0.06% – $981

That’s $5,520.12 in extra fees charged by Elavon in a single month.

We were able to eliminate everything except for the Monthly Discount Fee, but even that we got Elavon to cut it from 0.06% to 0.02%.

By negotiating just four fees on an Elavon statement, we saved this client over $60,000 per year in merchant fees.

So if you spot any of these charges on your Elavon statement, it’s a sign that you’re overpaying. Reach out to Elavon ASAP to demand removal. If they won’t budge or you’re struggling to do this on your own, contact our team here at MCC, and we’ll handle it on your behalf.

{kind=link}