Qualified processing rates refer to the merchant fees that a business pays for a specific type of credit card processing, known as tiered or bundled pricing. Depending on the merchant account agreement and fee structure, the qualified rate is one of the three possible tiers that a transaction can fall into—with mid-qualified and non-qualified as the other two possibilities.

The qualified processing rate is the lowest price of the three different qualification tiers, and it’s also the most commonly quoted rate from a merchant provider.

But most businesses are surprised to find that the majority of their credit card transactions aren’t getting the qualified rate, which adds to their costs of processing payments.

Here’s the bottom line—if you see the qualified rates, mid-qualified rates, or non-qualified rates anywhere on your monthly statements or merchant agreement, then I can guarantee you’re overpaying for credit card processing.

This guide will cover everything you need to know about qualified and non-qualified processing rates so you can make better sense of your statements and ensure you’re paying the lowest possible fees.

Who Determines Rate Qualification For Credit Card Processing?

The credit card processor determines the qualification rate for credit card processing. This is the biggest issue if you’re signed up for a tiered or bundled pricing structure.

While a three-tier structure sounds simple, there are actually hundreds of different credit card processing rates imposed at the card network level. These are known as interchange fees, and they’re the foundation for all costs associated with credit card processing.

The interchange rate is set by the card network (Visa, Mastercard, Amex, Discover) based on factors like the card used, transaction environment, and business type.

Credit card networks have zero influence on how credit card processors qualify transactions using the tiered pricing model.

Merchant service providers have total control over rate qualification. That’s why they route most transactions to the mid-qualified or non-qualified pricing buckets. It’s more expensive for the merchant, and more money goes into the processor’s pocket.

For example, you might see a Visa interchange rate at 1.65% + $0.05 for a specific transaction. But your processor could call this a non-qualified transaction (for whatever reason they want) and charge you upwards of 3.75% to process it.

Qualified and Non-Qualified Interchange Rates

There are no qualified or non-qualified interchange rates.

In the world of credit card processing, the terms “qualified” and “non-qualified” aren’t related to interchange, and the rates are completely made up by credit card processors.

Most merchants on a tiered pricing structure are confused to hear that there’s no such thing as non-qualified interchange rates because they see the words “non-qualified” on their monthly statements. But this is simply a way that processors classify different transactions—and the non-qualified rate is always the most expensive.

If you’re still confused or want to learn more, check out our complete guide to interchange rates and fees. This will further explain where interchange rates come from, and you’ll quickly see how they’re unrelated to the qualification tiers you’re paying.

Qualified and Non-Qualified Credit Cards

There are no qualified and non-qualified credit cards.

This is another common misconception for merchants on a tiered or bundled processing plan. They think that certain types of credit cards are causing transactions to get charged a non-qualified rate.

Regardless of what your processor tells you, Visa, Mastercard, and other card networks do not determine if a certain credit card is qualified or non-qualified. While the card networks assign different interchange rates based on the type of card being used, it’s still ultimately up to the processor to say whether a transaction falls into the qualified, mid-qualified, or non-qualified bucket.

Here’s an example. Let’s say two different processors both offered tiered pricing. Two merchants, both providing the same services, accept the same Visa consumer credit card. One processor could call the transaction qualified, and another could call it non-qualified.

The interchange fee is the same for both transactions because it’s the same card, but the qualification is arbitrary and has nothing to do with Visa or the card itself.

How Qualified Processing Works

The concept behind qualified processing is simple to understand. If the merchant is on a tiered or bundled pricing plan, all credit card transactions will fall into one of three categories—qualified, mid-qualified, or non-qualified.

Qualified transactions (also known as a qualified discount) are the least expensive, and non-qualified transactions are the most expensive.

Each time a customer buys something using a credit or debit card, the processor determines whether it’s a qualified, mid-qualified, or non-qualified transaction.

Unfortunately, processors tend to have their own best interest in mind—not the merchant. So they look for ways to ensure businesses pay the highest possible rates, which in this case, would be the mid-qualified or non-qualified tier.

The sales rep for a credit card processing company will always push the qualified rates to merchants as a way to advertise low-cost credit card processing. But it often isn’t until after the merchant signs a contract and starts accepting cards that they realize they rarely get the qualified rate.

As months pass, most merchants will see the majority of their transactions being charged the mid-qualified and non-qualified rate.

Qualification conditions are supposed to be based on certain factors as outlined in the merchant agreement. But here’s the kicker—processors can change the qualification terms at any time.

So you might be getting the qualified rate for a particular card or transaction one day and then get the non-qualified rate for the very same transaction a day later.

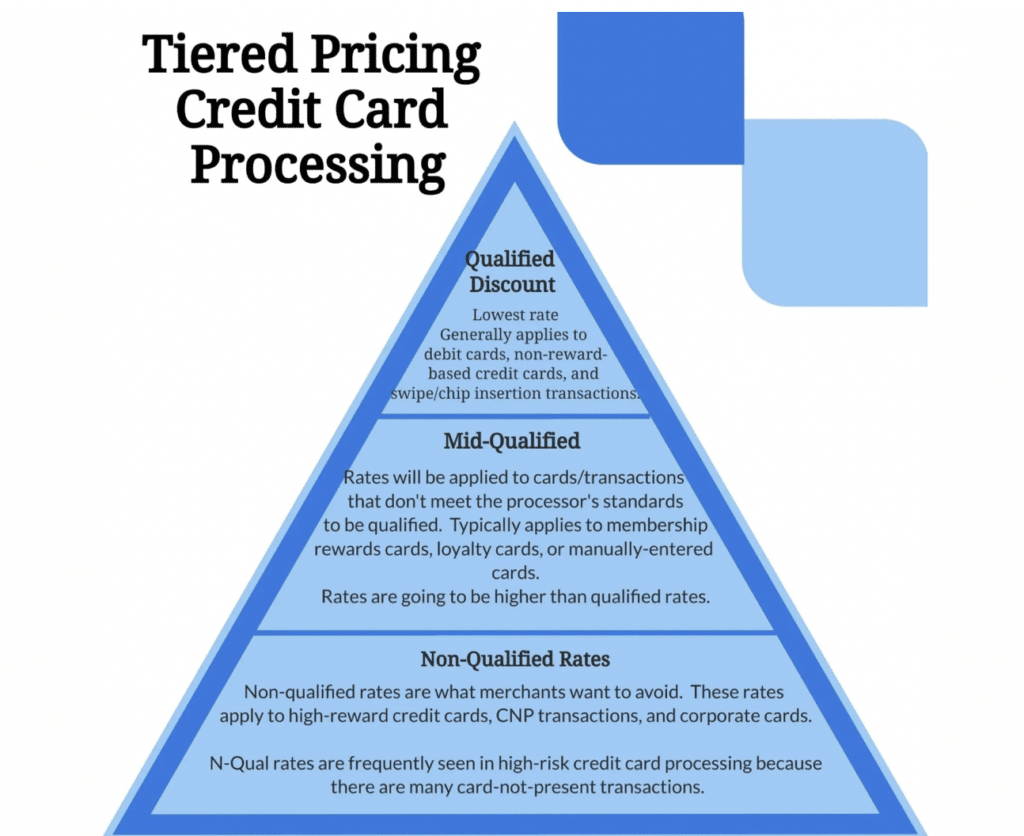

Qualified Processing Tiers

As previously mentioned, are three different qualified processing tiers:

- Qualified

- Mid-Qualified

- Non-Qualified

Each one has its own processing rates and conditions. We’ll take a closer look at all three in greater detail below.

Qualified Rate

Qualified transactions are the lowest rate a merchant will pay under the tiered pricing structure. Since it’s the cheapest rate, this is typically what processors advertise as a way to attract new merchants.

We’ve even seen some processors use the bait-and-switch technique—offering a qualified rate that’s actually below interchange rates (which would cause the processor to lose money on the transaction). But in this scenario, the processor won’t actually consider any credit card transactions to be qualified, and they’ll only route certain debit cards to the qualified tier.

Examples of conditions that might be required to get the qualified rate include:

- Personal debit card

- Non-rewards card

- Customer must sign the receipt

- Transaction must be batched and settled the same business day

Mid-Qualified Rate

As the name implies—the mid-qualified rate is the middle tier, but it’s often the lowest rate that merchants will be charged for transactions.

While many processors implement shady practices, even they’re smart enough to know that they can’t classify every transaction as non-qualified (although they could if they wanted to). So the mid-qualified rate is a better expectation for what businesses will pay for their least expensive transactions.

Here are some of the potential reasons why a processor may classify a transaction as mid-qualified:

- Card was not present (ecommerce)

- Rewards credit card was used

- Anything other than a debit card was used

- Corporate card was used

Non-Qualified Rate

Non-qualified rates are the most expensive rate within the tiered or bundle pricing structure. Processors will look for any excuse to classify a transaction as non-qualified because it results in the highest profit margins for them.

Common non-qualified rate criteria include:

- Manually keyed transactions

- Mismatched billing or no address verification

- Customer did not sign the receipt

- Transaction was not batched and settled within a certain time frame

What is a Good Qualified Rate For Credit Card Processing?

A good qualified rate for credit card processing is 1.65%. But as you now know, it’s unlikely that you’ll actually pay this rate, and the majority of your transactions will fall into the mid-qualified or non-qualified tiers, which may start around 2.75% or up to 4%, respectively.

Instead of focusing on the qualified rate, it’s better to look at your effective rate—which is the average percentage a business pays to process credit cards.

The effective rate includes more than just the qualification tier, and it also includes additional fees imposed by the processor.

For example, the average rate you pay might be around 3%. But when you consider your monthly statement fees, PCI compliance fees, AVS fees, gateway fees, and other junk markup costs added by your processor, your effective rate can jump to 3.5% or even 4%.

You can use this guide for a detailed description of how to truly calculate your processing rates.

How to Qualify For Lower Processing Rates

To qualify for lower processing rates, you should make sure you have a clear understanding of what your processor considers to be a qualified rate. But just be aware that the processor can change these terms at any point.

That’s why it’s best to avoid tiered pricing at all costs. Instead, you’ll be much better off with an interchange plus pricing structure.

With interchange-plus pricing, you just pay the interchange rate imposed at the card network level plus a predetermined markup by your processor. So instead of your processor charging you an additional 2% above the interchange rate, you may pay an extra 0.25% or 0.50% above the interchange.

Additional Reading: How to Lower Credit Card Processing Fees

Final Thoughts

Tiered processing is the worst possible contract structure for merchants. You rarely, if ever, get qualified processing rates—and you’re always getting charged more than you need to.

If you think you’re overpaying for credit card processing, we can help.

Our team can negotiate your rates directly with your processor, so you won’t have to switch. We’ll either try to lower the percentages at each qualification tier or, ideally, help get your processor to offer you interchange-plus pricing.

Get a free audit and analysis to see how much you can save today.

{kind=link}