If your business uses Elavon for credit card processing and you see any variation of OTHR NQ VOL FEE on your statement, it means Elavon is classifying a portion of your transactions as “non-qualified” and you’re paying more than you should be.

As a processor-imposed markup, this fee can be negotiated and even removed from your statements altogether.

Here’s what you need to know, and how we’ve handled it for our clients using Elavon.

What is the Elavon Non-Qualified Volume Fee?

Elavon’s Non-Qualified Volume Fee is an additional charge that Elavon assesses on top of your regular discount rate for any transactions deemed internally as non-qualified.

- Typically labeled as OTHR NQ VOL FEE on statements

- Charged at 0.55% on non-qualified volume as of February 2026

- Previously 0.40% of non-qualified volume from February 2025

It’s essentially Elavon’s way of downgrading transactions.

When Elavon Applies its NQ Volume Fee

The most common trigger is card-not-present (CNP) transactions, which can include:

- Online payments

- Virtual terminals

- Manually keyed cards

- Phone orders

Basically any scenario where the card isn’t present at the time of the sale. These transactions carry more fraud risk, so Elavon designates a portion of that volume accordingly.

It can also be applied if you’re not settling batches daily, completing address verifications, or doing anything that falls outside of what Elavon considers “best practices.”

The problem with this designation is that it’s arbitrary and everything is determined at Elavon’s discretion. There’s no formula or published table that merchants can use to predict or control it. You just see the charge on your monthly statement after the fact.

How it Differs From Other Non-Qualified Transaction Fees

In most instances, non-qualified charges from a payment processor indicate that the merchant is on a tiered pricing structure. This is when transactions get bucketed into qualified rates, mid-qualified, and non-qualified, with the non-qualified tier being the most expensive.

But Elavon’s approach is different.

They also applied their Non-Qualified Volume Fee to merchants on interchange-plus pricing.

The whole point of IC+ is that you’re supposed to pay the interchange cost plus a fixed markup. Adding a non-qualified volume fee defeats that purpose as you’re essentially getting a hidden penalty on top of your regular discount rate.

Additionally, the term “non-qualified” can also be used at the interchange level (like with Visa’s Non-Qualified Consumer Credit Fee). But unlike Visa’s fee that’s universally applied to all merchants for specified criteria, Elavon’s criteria isn’t consistent for all merchant accounts.

And Elavon charges its non-qualified rate in instances where Visa does not.

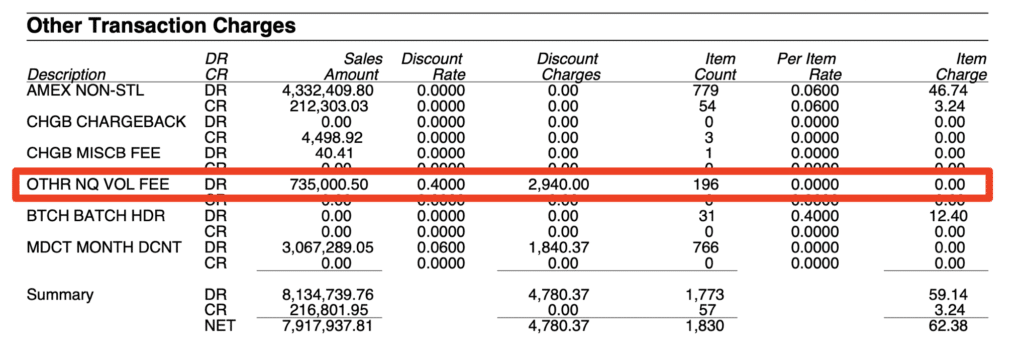

What This Looks Like on Elavon Statements

Here’s a real example from a client statement that we audited:

As you can see, Elavon classified $735,000 of this merchant’s volume as non-qualified. At a 0.40% discount rate, this resulted in $2,940 in additional fees for this month alone.

This goes straight to Elavon.

At the current 0.55% rate, this same volume would have cost $4,242.50, which is a meaningful difference and highlights the significance of that most recent rate increase.

What You Can Do About It

The good thing about the Elavon Non-Qualified Volume Fee is that it’s negotiable, and we’ve successfully eliminated it from client accounts altogether.

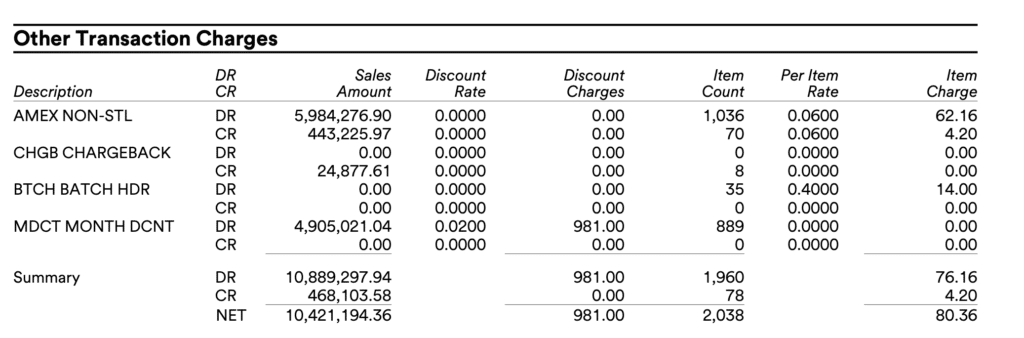

Here’s a statement from the same merchant after we negotiated we Elavon on their behalf:

The fee is gone. There’s no OTHR NQ VOL FEE at all.

Let’s talk about the savings impact here from just one line item:

This merchant’s non-qualified volume had been running at roughly 10% of their total processing. Their volume grew to $10.4M in net monthly sales here, and at today’s rate of 0.55%, the fee would be ~$5,720 per month (estimated $1,040,000 non-qualified volume).

Removing this fee entirely saved this merchant over $68,000 per year.

Final Thoughts

Elavon’s non-qualified volume fee is a big problem for certain businesses, particularly those accepting payments without the physical card present.

The fact that qualification is solely at Elavon’s discretion is also problematic, especially when it’s applied to interchange-plus accounts (not just tiered pricing).

So if you see this fee on your statement, don’t just brush it off as a cost of doing business. It could be costing you thousands per year, and potentially more if your statement has other Elavon fees that can be negotiated.

Pick up the phone and demand that Elavon remove this from your account. If you’re struggling and they won’t budge, you can always contact us and we can get it removed on your behalf — without switching providers.

{kind=link}