Fiserv (formerly First Data) is one of the largest payment processors in the world. They handle over 25,000 transactions per second for six million merchants globally—making them the largest non-bank merchant acquirer in the US.

One unique standout of Fiserv is that they serve businesses of all sizes across every industry. From SMBs using Fiserv’s Clover POS system to banking partners and ISOs reselling Fiserv’s processing services to enterprise-level merchants, they support just about every possible account that you could imagine.

Due to their massive market share, particularly here in the US, we have nearly 100 clients here at MCC who rely on Fiserv for payment processing. We have years of experience auditing these statements and negotiating rates directly with Fiserv, which gives a unique perspective that you won’t find anywhere else on the web.

So whether you’re a current Fiserv customer who’s trying to save money on processing or you’re considering using Fiserv for the first time, this review will help steer you in the right direction.

Our Insider Quick Take on Fiserv

We’ve always had a positive experience working with Fiserv. Their massive size puts them in a position where they can offer competitive rates, and barring a few one-off mishaps, Fiserv is usually transparent when it comes to billing and pricing.

Financial institutions like Bank of America, PNC, Santander, Citi, and other regional banks partner with Fiserv to resell merchant services to their clients. Most independent agents and companies reselling merchant services use Fiserv because of their agent-friendly and ISO programs. These banking partnerships are one of the ways that Fiserv has grown over the years and acquired such massive accounts.

So even merchants that have never dealt with Fiserv directly may be relying on Fiserv to process transactions on the backend because that’s what their independent rep is using.

Technology-wise, they have tons of capabilities and integration options. Again, this is mostly due to how big they are.

Fiserv Pros

- Transparent pricing and competitive interchange-plus rates for payment processing.

- They rarely increase rates, and when they do, it’s minimal.

- In instances when Fiserv raised rates for our clients, we’ve been able to successfully negotiate lower terms.

- Technology-wise, Fiserv has tons of capabilities and seemingly limitless integration options.

- Fiserv makes it easy for businesses of all sizes to accept payments from any channel—and this extends to merchants leveraging Fiserv through an ISO, bank, or reseller.

- We like Clover POS for small businesses using Fiserv.

Fiserv Cons

- We found a liquidated damages clause in the early termination section of several Fiserv merchant agreements.

- Their interchange rates for Level 2 and Level 3 processing aren’t always optimized (even though they’re supposed to be).

- We’ve found inconsistent billing and rate fluctuations across different merchant accounts, although this is usually due to the merchant’s size and processing volume.

Fiserv Pricing and Fees to Look Out For

Fiserv offers interchange-plus pricing at custom rates for every new merchant account. Your specific rate will vary based on your volume and whether you’re going directly to Fiserv or through an ISO.

In addition to your per-transaction markups, here are some fees you might see on your statement:

- Annual Fee — Varies from $95 to $120

- Inactivity Fee — $197 per month

- Qualified Discount Rate — Typically as a percentage, but sometimes fixed

- PCI Compliance Fee — Roughly $60 per month

- Batch Fees — $0.35 to $0.50 per batch

- Clover Security Plus Fee — $19.95 per month

Depending on the software or hardware integrations you’re getting through your provider, you might see additional monthly fees on your statement for those.

All of these fees listed above can be removed or negotiated—and so can Fiserv’s markup for each transaction. If you need help with this, contact our team here at MCC for a free audit. We’ll negotiate with Fiserv on your behalf so you can save money without switching processors.

Other Fiserv fees that can really add up include:

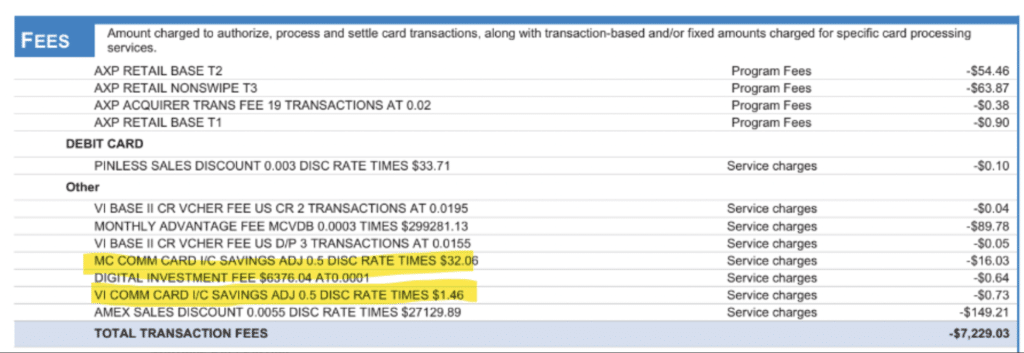

COMM CARD I/C Savings Adjustment Fee

One gripe that we do have with Fiserv, specifically related to its fees, is its COMM CARD I/C Savings Adjustment Fee. Here’s an example of this shown on a recent Fiserv statement:

The fee is “supposed” to automatically help merchants get optimized rates for Level 2 and Level 3 card data. But Fiserv is actually taking a percentage of those savings for themselves.

If you look closely at the fees highlighted above, you’ll see ADJ 0.5 DISC RATE—which is essentially saying that the merchant is only getting 50% of the savings for both of those line items.

The other 50% is a fee paid directly to Fiserv.

This doesn’t make any sense, especially because they’re already getting their normal processing fees for those transactions. If the rates were truly optimized, the savings would be completely passed on to the merchant.

Plus, we’ve seen this rate fluctuate from 25% to 75%. It really just depends on the size of the merchant.

While this isn’t a dealbreaker by any means, it’s still annoying and worth mentioning. Although it only really affects merchants that accept lots of B2B transactions where additional card data is captured.

Random Annual and Monthly Merchant Services Fees

You may notice some miscellaneous fees that appear on monthly statements if you’ve obtained Fiserv’s processing services through an ISO or reseller.

For example, we’ve seen CardConnect (a super ISO of Fiserv) charge a $119 Annual Membership Fee to businesses, and Leader Merchant Services (another ISO) charge $59.95 monthly PCI Compliance Fee.

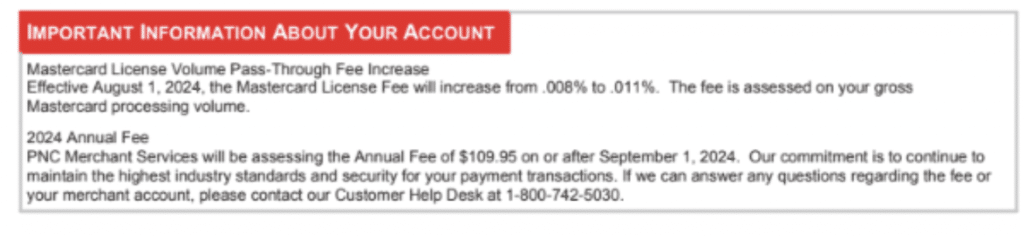

Here’s another we just found from PNC Bank, where they’re charging a $109.95 Annual Fee to businesses for merchant services—and they’re using Fiserv to handle the processing on the backend.

So again, it really just depends on how you’re obtaining processing services from Fiserv.

Liquidated Damages Fees

Liquidated damages are the worst type of early termination fee in the world of credit card processing. Fortunately, this fee can be avoided altogether as long as you don’t cancel your merchant account agreement prior to the contract end date.

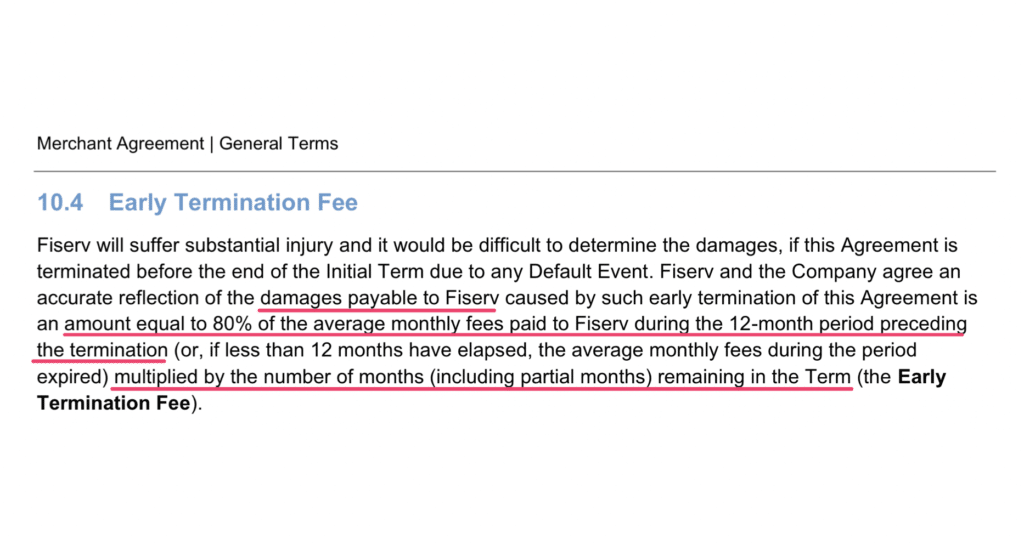

But with that said, we’ve found a liquidated damages clause in several merchant account agreements from Fiserv. Here’s an example:

What’s tricky about this is that Fiserv isn’t actually calling it a liquidated damages fee. But if you read closely, it’s clearly a liquidated damages clause.

Fiserv takes 80% of your average fees from the past 12 months and then multiplies it by the number of months remaining on your contract.

Let’s say this clause was in your contract, and you want to cancel 24 months into a 36-month term. If you averaged $6,000 in fees paid to Fiserv over the last 12 months, they’d take 80% of that ($4,800) and multiply it by the remaining 12 months—meaning it would cost you $57,600 to cancel.

We rarely recommend terminating your merchant account—especially with Fiserv. They’re solid, and it’s unlikely you’ll get a better rate elsewhere. So this fee is somewhat of a moot point since it’s only applied if you’re terminating a contract.

However, try to get this clause removed if you’re signing a long-term contract with Fiserv. You could even have them replace it with a flat-rate early termination fee of $500 or $1,000 if you needed a bargaining chip. This would be so much cheaper than getting hit with liquidated damages.

Latest Fiserv Rate Increases, Updates, and Noteworthy News

Fiserv historically hasn’t raised their rates too often. However, we’ve seen two significant rate increases in 2025.

Fiserv rates are up 0.10% + $0.10 per transaction, which was applied to some merchant accounts in November 2025, and others were hit with the same increase in September 2025.

This comes on the heels of a chargeback fee structure change in June, and more importantly, a 0.30% rate hike in March 2025.

We have a separate guide that tracks the full history of Fiserv fees and updates that you can refer to for older news and any upcoming changes.

A Closer Look at Clover: Fiserv’s Small Business POS System

Clover is Fiver’s internally produced POS system. It’s designed specifically for small businesses—particularly those with a brick-and-mortar presence.

It’s an all-in-one point-of-sale system that supports in-person, online and mobile payments.

This is definitely something that Fiserv is trying to leverage for growth in the small business market. They’re pushing hard to get this product and technology in the hands of ISOs and banks in their partner network.

One recent example of this is VizyPay. I just reported that VizyPay has already invested over $1.3 million in Clover hardware through the first six months of 2024 alone.

It feels like Fiserv is just doing a complete rebrand of their small business services under the Clover name. We’ve seen them go through changes like this in the past (like when they rebranded from First Data to Fiserv).

Just be aware that if you’re using Clover, whether it be directly through Fiserv or through a third-party reseller, you may notice some additional fees on your statement.

A Closer Look at Carat: Fiserv’s Global Ecommerce Platform

Carat is basically the enterprise-level counterpart to Clover. Rather than focusing on in-person POS sales for small businesses, Carat is built for large-scale ecommerce businesses.

It’s used by global powerhouses like Google, Microsoft, Walmart, and Fanatics—companies with complex needs and cross-border sales.

Carat is advertised as a way to get optimized processing rates. And while that’s definitely possible, we’ve seen instances where those rates aren’t actually optimized.

But like everything else Fiserv does, Carat is extremely powerful. It can really handle any complex integration and cross-border sales needs for a global business. Although it’s a bit too advanced for just an average ecommerce site that sells primarily in the US.

Final Verdict: Is Fiserv Legit?

Fiserv is a solid, legitimate payment processor. They’re a massive company, but unlike other large processors we deal with, Fiserv doesn’t use their size to take advantage of businesses.

Do we have a few gripes with them or fees we’d like to see eliminated? Absolutely.

But overall, their prices are reasonable, and they’re open to negotiations.

So if you’re currently using Fiserv for processing and feel like you’re overpaying, contact our team for a free audit. We’ll negotiate with Fiserv on your behalf so you can save money without switching.

{kind=link}