Most merchants are under the assumption that their routing systems are optimal. That’s because credit card processors have sold them on the concept of dynamic routing.

However, if you take the time to truly assess your debit card processing, you’ll quickly discover there are ways to save money.

For a merchant, optimal debit card routing means that you’re using the most cost-effective solution. But your debit card processing fees will vary based on a wide range of factors.

I created this guide to give you an incentive to audit your debit card processing solution. I’ll teach you what you need to know about debit card routing so you use an optimized method.

Debit Card Routing Paths Explained

Before we go any further, I want to explain the two ways that debit card transactions can be processed—PIN routing and signature routing.

The routing paths for each of these vary, which will affect your fees. You could be paying too much for debit card processing if you’re using a non-optimal method.

PIN Debit Routing

Cardholders use a personal identification number (PIN) to complete a debit card transaction.

This processing method goes through a PIN debit network for routing. For PIN debit routing, the transaction bypasses Visa or Mastercard’s network. As a result, interchange fees from these card networks will not apply to your transaction.

Instead, the PIN network fees will be imposed. PIN networks typically have low percentage fees, but higher fixed fees for each transaction. Due to this pricing structure, low-ticket purchases are more expensive for merchants.

For example, let’s say you run a local or national coffee chain. $2 transactions would not be optimal for PIN-based debit card routing.

Signature Debit Routing

Unlike PIN debit routing, a signature debit transaction will get processed through a card network. Customers verify these transactions with their signature, hence the name.

You can compare a signature debit transaction to traditional credit card processing. That’s because they’ll be routed the same way through a processor and card network. With that said, there are still differences between credit and debit transactions.

PIN networks do not have a role in processing a signature debit card. But these transactions are subject to interchange fees imposed by the appropriate card network.

The signature debit processing fees are significantly lower than a standard debit card transaction. That’s because there is far less risk associated with these transactions. The issuing bank does not have to extend any credit. Money is deducted straight from the cardholder’s checking account.

What You Need to Know About Debit Card Routing Optimization

Now that we’ve covered the basics about the two paths a debit card transaction can take, it’s time to take a look at some other factors associated with debit routing.

No Network Exclusivity (NNE)

The Durbin amendment of 2011 had a clause for No Network Exclusivity (NNE).

This clause was enacted to entice competition between card networks. It guaranteed that each debit card must have at least two mutually exclusive debit networks. Merchants have the ability to route PIN debit transactions at competitive rates. That’s because there are more options in the industry, as opposed to a monopoly of just one network per card.

Payment Processor Incentives

All PIN routing will still go through your payment processor. But your credit card processing company might have relationships with specific debit card networks.

In these cases, payment processors have an incentive to route the transaction based on what’s financially optimal for them—not for the merchant.

Payment processors could receive a higher percentage or bonus based on the volume of PIN debit transactions routed through a particular network. But you could potentially save money on debit card sales if those same transactions were routed elsewhere.

In some cases, there might be a clause in your credit card processing contract that does not oblige the processor to optimally route debit transactions in your favor. So essentially, they have free rein to do whatever they want.

Your Own Incentive Agreements With Networks

Larger merchants and enterprises are often able to negotiate their own terms with debit networks.

In these cases, it’s common for a network to offer you a large sum of cash upfront to prioritize their network for PIN debit routing.

While a big check can be tempting, take the time to weigh the true cost of this agreement.

This short-term gain could end up costing you significantly more money in processing fees in the long-run. So I’d recommend seeking an alternative incentive agreement if you’re presented with this offer.

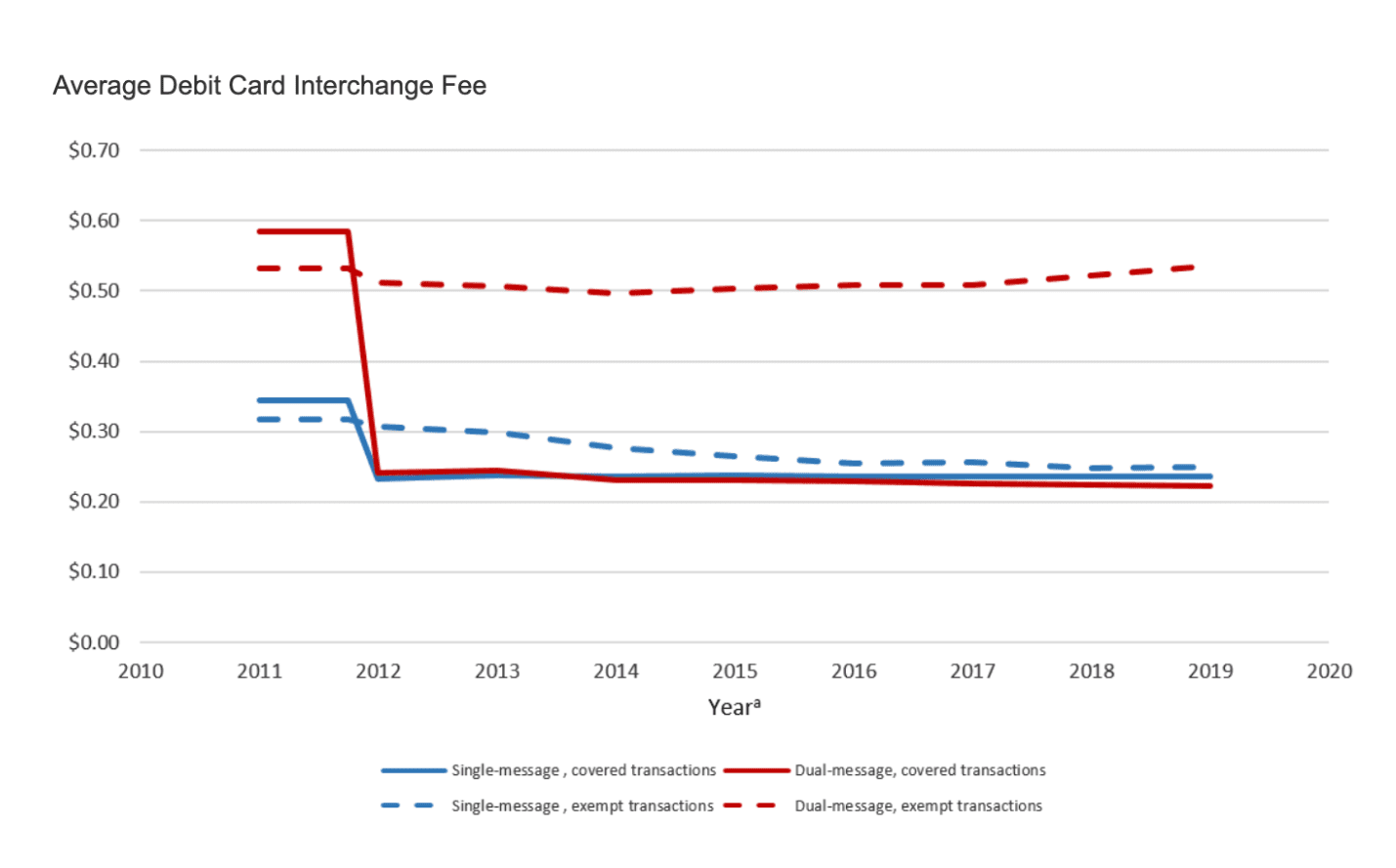

Unregulated Interchange Fees

Earlier, we talked about the Durbin amendment. But not every transaction applies to these regulations.

According to data from the US Federal Reserve, roughly 37% of debit transactions are exempt from the Durbin amendment. This explains why those interchange fees haven’t dropped. Here’s a look average interchange fees by year:

Take a look at the red dotted line in this graph. This is for duel-message networks and exempt transactions.

Those interchange fees remain high, even after the Durbin Amendment went into effect in 2011. As you can see, the average rate has been slowly rising over the last few years and is trending upward.

Final Thoughts

Optimal debit card routing is a complex subject.

A payment processor cannot simply view a table of various network fees to find the most cost-effective route for merchants. There are lots of other factors at play.

So how do you optimize your debit card routing?

There isn’t a blanket statement or general piece of advise that applies to all businesses. It’s in your best interest to get an audit and assessment from an expert in the payment processing industry.

Here at Merchant Cost Consulting, we can do this for you. We’ll let you know how much money you can save on debit card processing.

For large businesses, enterprises, and chains that are processing millions of dollars a year, that savings amount can be significant.

{kind=link}