Unlike Visa and Mastercard, American Express credit card processing isn’t very straightforward.

That’s because Visa and Mastercard are both open credit card networks, meaning anyone can issue cards. But American Express is a closed network. This structure gives Amex much more control over credit card merchant fees.

As you’ve probably learned by now, it costs more to accept American Express credit cards. Anyone who accepts Amex cards knows this. Exactly how much more? Sometimes it’s difficult to understand.

I consult with merchants on a daily basis. Most small business owners have lots of questions about their American Express processing fees, which is what inspired me to write this guide. I’ll clear up any misconceptions and paint a clearer picture of Amex credit card processing fees.

This guide also contains the latest information on Amex interchange rate changes and fee increases.

New Variable Authentication Feature

Effective October 18, 2024, American Express is rolling out a new feature for merchants on the OptBlue program. This feature will allow businesses and third-party processors to request an increase or decrease to the amount authorized prior to submitting a transaction.

This applies to:

- Estimated Authorizations

- Incremental Authorizations

- Partial Reversals

New American Express OptBlue Interchange Rates

American Express updated its OptBlue program with interchange fees and categories for merchants in different industries. Aside from the industry (designated by the merchant’s MCC code), the interchange rate tier depends on the amount of the settled transaction, and whether or not the payment was accepted in person or keyed.

All of the rates below are for US-based merchants and have an additional 0.15% American Express Network Assessment Fee on settled transactions.

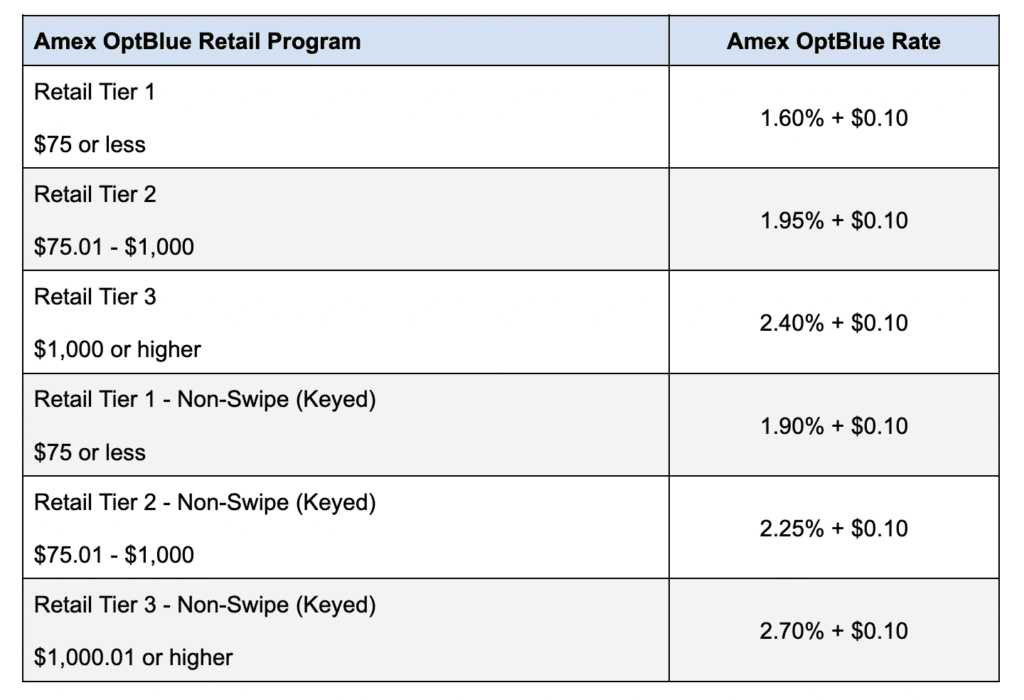

Amex OptBlue Retail Interchange Rates (April 2024)

US-based retailers with one of the following MCC codes are eligible for the rates displayed in the table below: 5013, 5021, 5044, 5072, 5122, 5192, 5193, 5200, 5211, 5231, 5251, 5261, 5300, 5309, 5310, 5311, 5331, 5399, 5411, 5422, 5441, 5451, 5462, 5499, 5531, 5532, 5533, 5551, 5611, 5621, 5631, 5641, 5651, 5655, 5661, 5681, 5691, 5698, 5699, 5712, 5713, 5714, 5715, 5718, 5719, 5722, 5732, 5733, 5734, 5735, 5815, 5816, 5817, 5818, 5912, 5921, 5931, 5932, 5937, 5940, 5941, 5942, 5943, 5944, 5945, 5946, 5947, 5948, 5949, 5950, 5965, 5970, 5971, 5972, 5973, 5977, 5978, 5992, 5993, 5994, 5995, 5996, 5997, 5998, 5999, 7296, 7622, 7631, 7841.

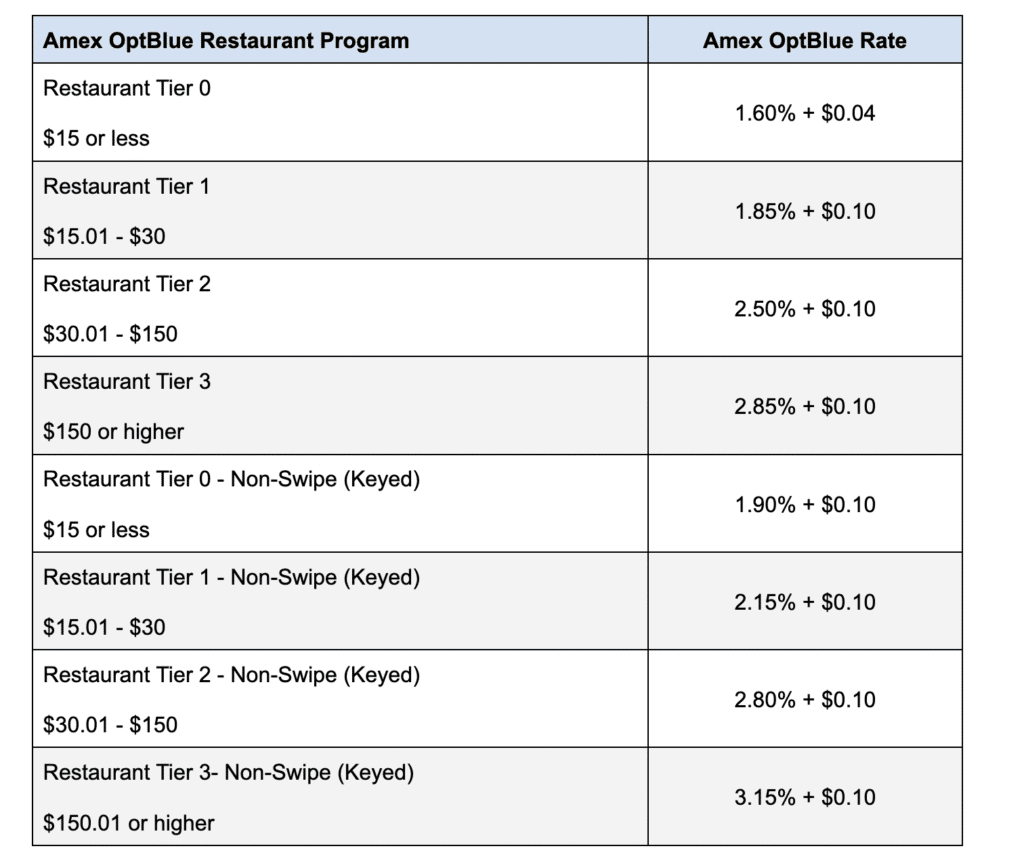

Amex OptBlue Restaurant Interchange Rates (April 2024)

The rates below only apply to eligible restaurants in the US with any of the following MCC codes: 5812, 5811, 5813, 5814.

Essentially, these OptBlue rates are for restaurants, caterers, bars, taverns, nightclubs, cocktail lounges, and fast food establishments.

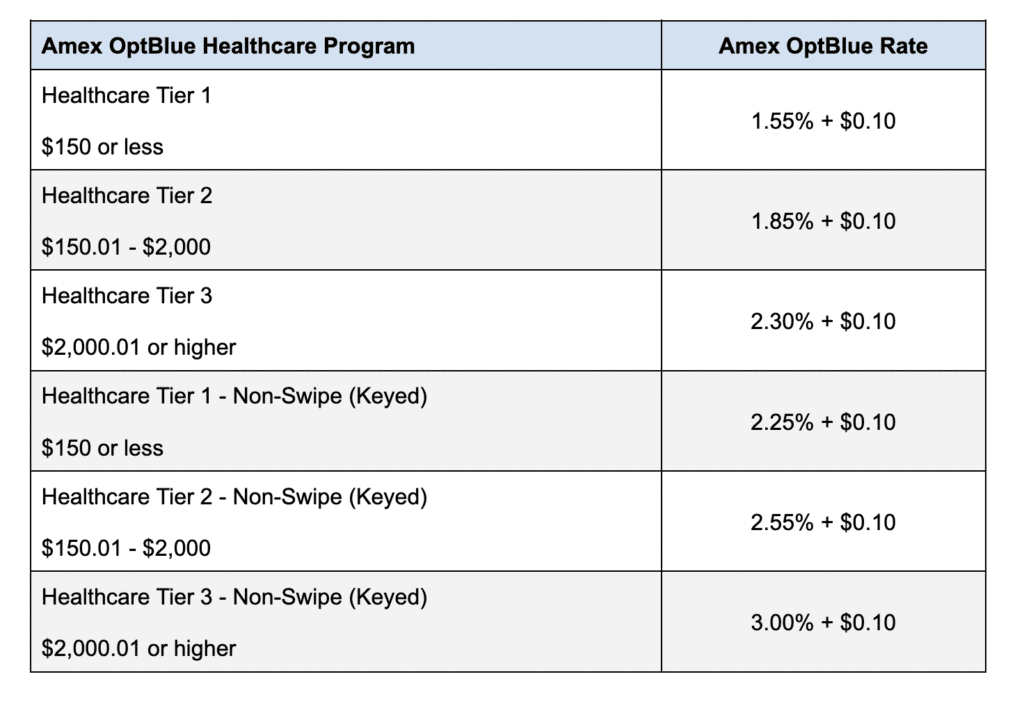

Amex OptBlue Healthcare Interchange Rates (April 2024)

Healthcare organizations in the US in the Amex OptBlue program will be charged the rates below, assuming they have one of these MCC codes: 8011, 8021, 8031, 8041, 8042, 8043, 8049, 8050, 8062, 8071, 8099, 0742, 4119.

This applies to doctors, dentists, osteopaths, chiropractors, optometrists, opticians, podiatrists, nursing/personal care facilities, hospitals, medical/dental labs, medical services, veterinary services, ambulance services.

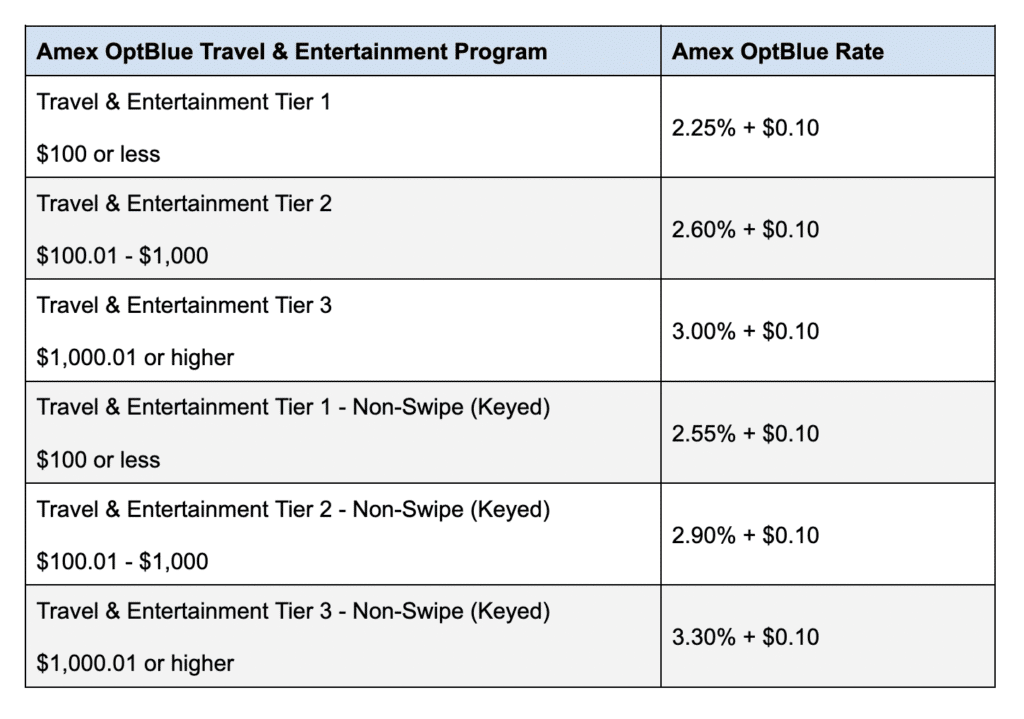

Amex OptBlue Travel & Entertainment Interchange Rates (April 2024)

These Amex OptBlue interchange rates apply travel and entertainment companies with these MCC codes: 4111, 4112, 4121, 4131, 4582, 4722, 4789, 7011, 7033, 7512, 7832, 7922, 7929, 7932, 7933, 7941, 7991, 7992, 7993, 7994, 7996, 7998, 7999.

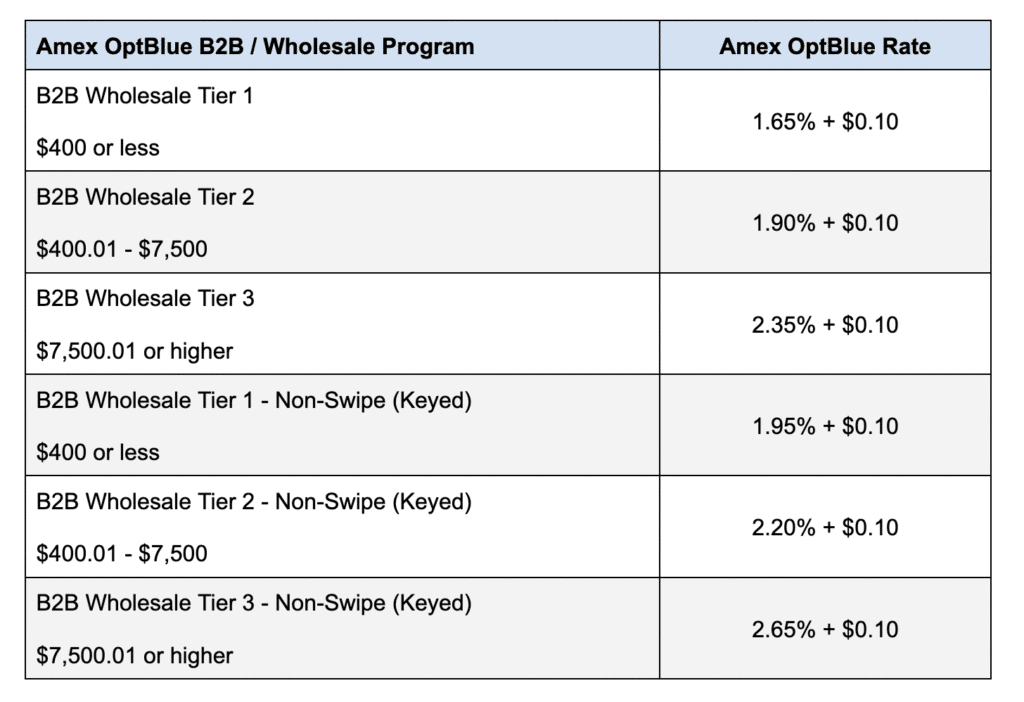

Amex OptBlue Wholesale/B2B Interchange Rates (April 2024)

You must be a wholesale company or sell business-to-business to be eligible for the rates below. These rates apply to US-based wholesalers with the following MCC codes: 1799, 7349, 2791, 5131, 7361, 5127, 4215, 5039, 5045, 5046, 5047, 5051, 5065, 5085, 5094, 5099, 5111, 5139, 5169, 5172, 5198, 5199, 4011, 7311, 7333, 7338, 7339.

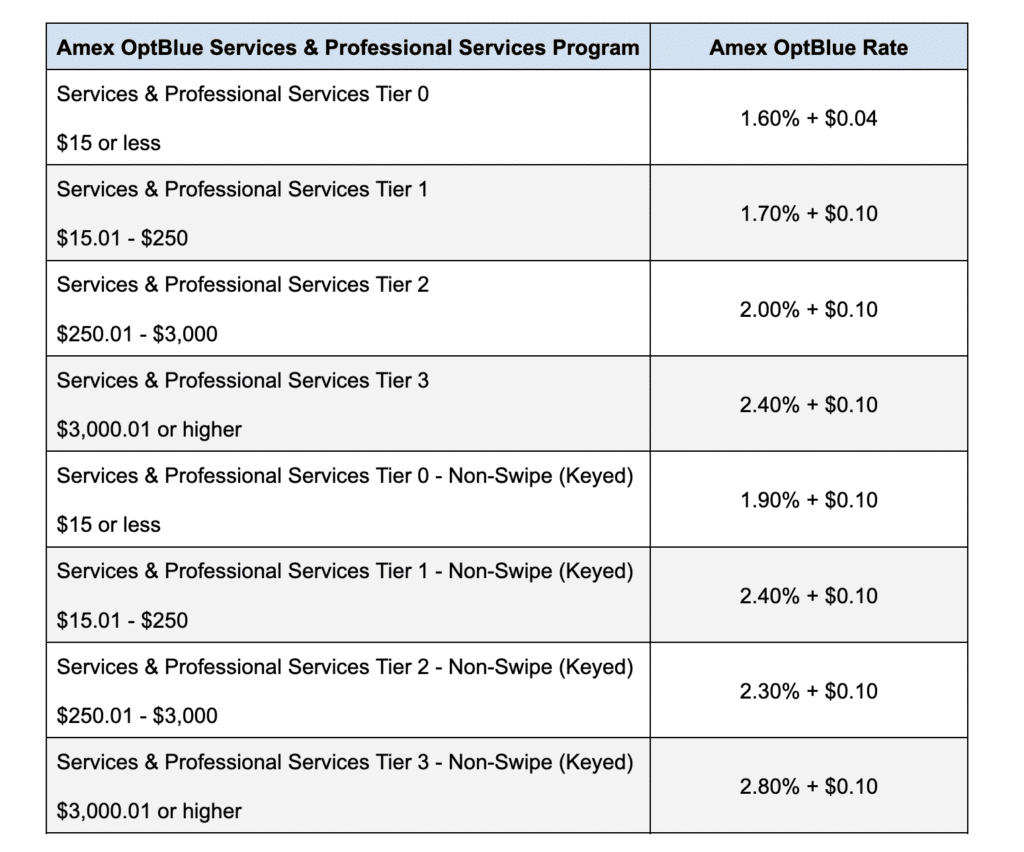

Amex OptBlue Services & Professional Services Interchange Rates (April 2024)

The services and professional services category is vast, ranging from plumbers to legal services, to computer repair, parking lots, roofing, pawn shops, electrical contractors, wine producers, and beyond.

Here’s a quick look at the MCC codes associated with the table below: 0743, 0744, 0763, 1520, 1711, 1731, 1740, 1750, 1761, 1771, 2741, 2842, 4214, 4225, 4457, 4468, 4816, 4821, 4900, 5074, 5271, 5511, 5521, 5561, 5571, 5592, 5598, 5599, 5697, 5933, 5935, 7251, 7273, 7276, 7277, 7278, 7297, 7298, 7299, 7321, 7342, 7393, 7395, 7513, 7519, 7523, 7531, 7534, 7535, 7538, 7542, 7549, 7621, 7623, 7629, 7641, 7699, 7997, 8111, 8641, 8675, 8699, 7372, 7375, 7379, 6513.

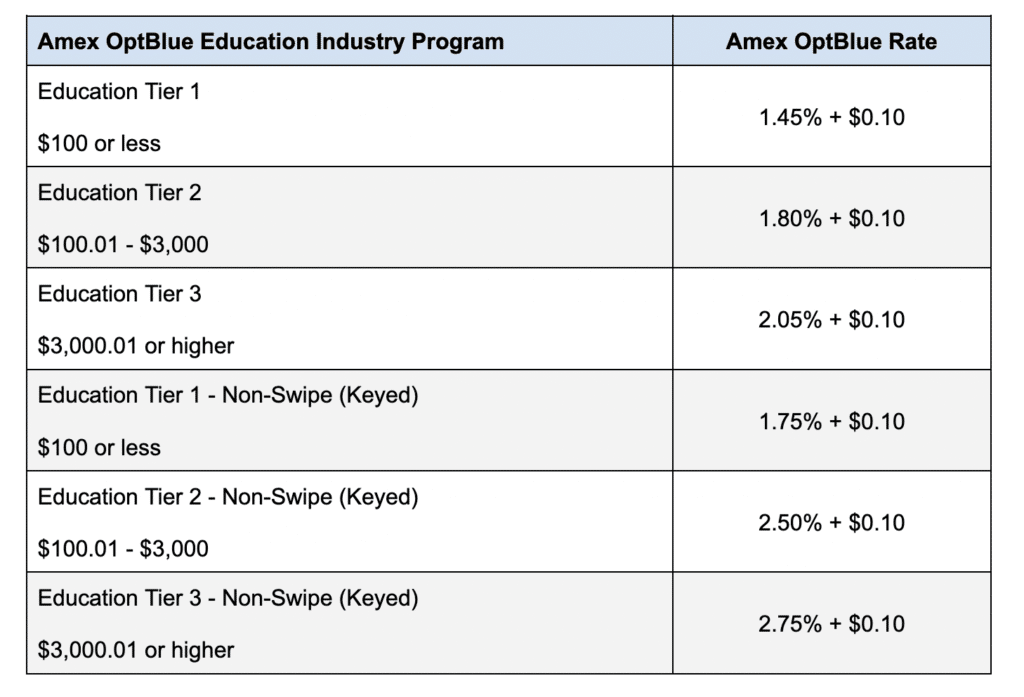

Amex OptBlue Education Industry Interchange Rates (April 2024)

These American Express OptBlue rates are for sporting and recreational camps, dance halls, studios and schools, correspondence schools, business and secretarial schools, vocational and trade schools, schools and educational services—with MCC codes 7032, 7911, 8241, 8244, 8249, and 8299.

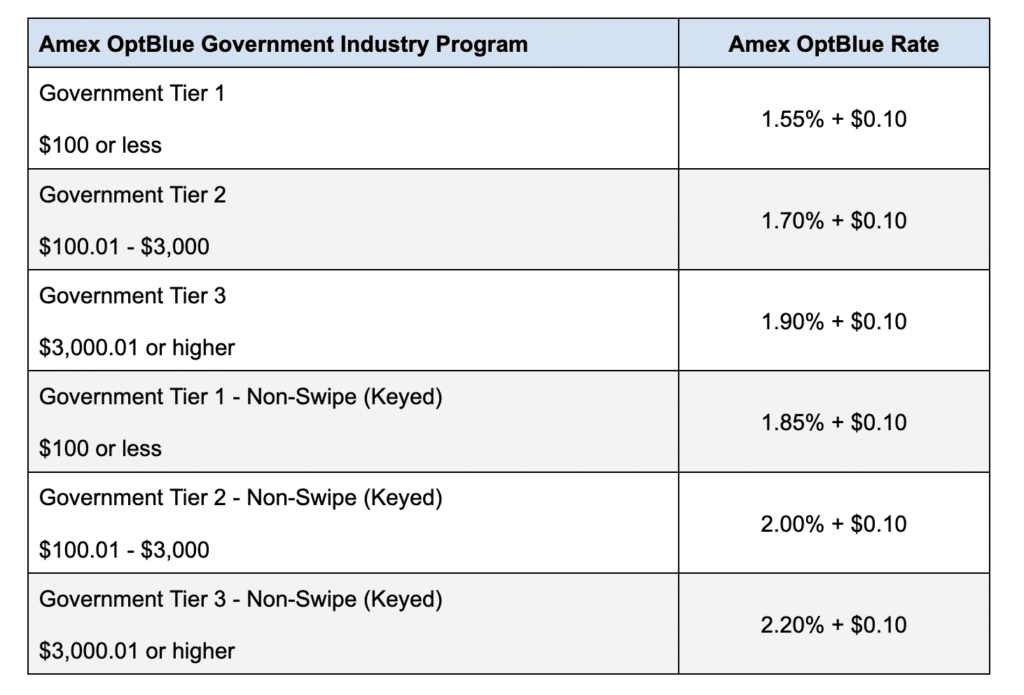

Amex OptBlue Government Industry Interchange Rates (April 2024)

Only 3 MCC codes are eligible for this OptBlue category:

- 9311 – Tax Payments

- 4784 – Tolls and Bridges

- 9223 – Bail and Bond Payments (fee only)

Amex Fraud and Chargeback Updates

Effective January 2024, American Express has made changes to its OptBlue program—specifically regarding the requirements for merchants submitting chargeback reversals. This effects the following types of chargeback disputes:

- Credit not processed

- Goods/services returned or refused

- Goods/services canceled

- Goods/services not received or only partially received

- Paid by other means

- No show or deposit canceled

- Cancellation of recurring goods/services

- Goods/services nota s described

- Goods/services damaged or defective

- Vehicle rental capital damages, theft, or loss of use

Effective April 2024, merchants will no longer be subjected to CNP fraud chargebacks if they submit an approved transaction that contains a “no match” data verification.

Old Amex Interchange Rates

Here’s a look at Amex OptBlue Rates that went into effect on 10/14/2022. While they’re obsolete now, they can be useful for comparison purposes to see how American Express has increased its rates over time.

Education and Government Interchange Rates

- Education Tier 1 Credit – 1.10% + $0.10

- Education Tier 2 Credit – 1.45% + $0.10

- Education Tier 3 Credit – 1.70% + $0.10

- Government Tier 1 Credit – 1.40% + $0.10

- Government Tier 2 Credit – 1.55% + $0.10

- Government Tier 3 Credit – 1.75% + $0.10

An additional 0.30% will be imposed on manually keyed transactions.

As of 10/14/2022, merchants in the following MCCs will be moved from the Emerging Markets interchange program to the Education segment:

- Elementary School (8211)

- College (8220)

- Child Care Services (8351)

Merchants in these three MCCs will move from the Emerging Markets segment to the Government program:

- Court Costs (9211)

- Fines (9222)

- Government Services (9399)

Merchant Segment Programs and Interchange Rates

Effective October 14, 2022, Amex intrododuced five new merchant segments in the Amex OptBlue program: Charity, Insurance, Residential Rent, Utilities, and Online Gambling.

Here’s a look at those new Amex interchange rates:

- Charity Tier 1 – 2.00% + $0.02

- Charity Tier 2 – 1.60% + $0.04

- Charity Tier 3 – 2.00% + $0.10

- Insurance Tier 1 – 1.25% + $0.10

- Insurance Tier 2 – 1.85% + $0.10

- Insurance Tier 3 – 2.50% + $0.10

- Residential Rent Tier 1 – 1.40% + $0.10

- Residential Rent Tier 2 – 1.75% + $0.10

- Residential Rent Tier 3 – 1.90% + $0.10

- Utilities Tier 1 – 0.00% + $0.75

- Utilities Tier 2 – 1.50% + $0.00

- Utilities Consumer Debit – 0.04% + $0.65

- Utilities Small Business Debit – 0.09% + $1.45

- Online Gambling Tier 1 – 2.40% + $0.10

- Online Gambling Tier 2 – 2.75% + $0.10

- Online Gambling Tier 3 – 3.15% + $0.10

- Online Gambling Consumer Debit – 1.19% + $0.15

An additional 0.30% will be imposed on manually keyed transactions for online gambling.

The Online Gambling segment is newly eligible for participation in the American Express OptBlue program.

American Express OptBlue Continuation Fee (US)

As of October 14, 2022, US merchants will have a new program continuation fee to all Amex sales exceeding $3 million in a rolling 12-month period. The new fee is 0.03%.

This applies to merchants in industries with a threshold limit of $1 million.

Other American Express Interchange Updates

As of July 1, 2022, Amex is updating its pricing policies and discount rates. In a letter from the American Express merchant care team, these changes are based on the merchant’s prior year of activity and industry. Here’s a quick summary of those changes:

- Credit and charge cards – 3.03% + $0.10 per transaction

- Prepaid cards – 1.68% + $0.15 per transaction

- Corporate purchasing cards – 3.01% + $0.10 per transaction

Check your statements to see if these new charges apply to your business. You can also have the team here at Merchant Cost Consulting review your statements to check for any specific rate increases.

American Express Interchange Updates and OptBlue Changes

Like the other major credit card companies, American Express is made significant changes to interchange pricing and fees in April 2022.

Debit Interchange Fees For OptBlue

Effective 4/22/2022, Amex introduced a new debit card program for unregulated and regulated consumer and business debit products.

OptBlue Unregulated Consumer Debit Interchange

- B2B / Wholesale Consumer Debit – 0.99% + $0.15

- Education Consumer Debit – 0.79% + $0.15

- Emerging Market Consumer Debit – 0.79% + $0.15

- Government Consumer Debit – 0.79% + $0.15

- Healthcare Consumer Debit – 0.99% + $0.15

- Restaurants Consumer Debit – 1.29% + $0.10

- Retail Consumer Debit – 0.99% + $0.15

- Services and Professional Consumer Debit – 0.99% + $0.15

- Travel and Entertainment Consumer Debit – 0.99% + $0.15

- Other Consumer Debit – 0.99% + $0.15

OptBlue Unregulated Small Business Debit Interchange

- B2B / Wholesale Small Business Debit – 1.94% + $0.10

- Education Small Business Debit – 1.99% + $0.10

- Emerging Market Small Business Debit – 1.99% + $0.10

- Government Small Business Debit – 1.99% + $0.10

- Healthcare Small Business Debit – 1.94% + $0.10

- Restaurants Small Business Debit – 1.99% + $0.10

- Retail Small Business Debit – 1.94% + $0.10

- Services and Professional Small Business Debit – 1.94% + $0.10

- Travel and Entertainment Small Business Debit – 1.99% + $0.10

- Other Consumer Debit – 1.94% + $0.10

Other Amex OptBlue Pricing Updates

Here are some additional changes for OptBlue effective 4/22/2022:

- Service and Professional Tier 1 – 1.65% + $0.1

- Service and Professional Tier 2 – $15.01 – $150 (new transaction threshold)

- Service and Professional Tier 3 – $150.01 – $3,000 (new transaction threshold)

- Acquirer Transaction Fee – $0.02

- Assessment Fee – $0.165

American Express “Interchange” Fees Explained

Credit card processing fees are broken down into three categories—interchange, assessments, and payment processor markup.

What is an interchange fee?

Interchange is paid to the issuing bank. These are the costs associated with a particular interchange category, depending on the criteria of a transaction.

Visa and Mastercard publish transparent interchange fee tables online. This makes it easy for merchants to calculate their costs before assessments and markup.

American Express is a bit different. Technically, American Express doesn’t have interchange fees. Amex has “discount fees” that operate the same way as an interchange fee.

All credit card networks collect a network fee or card brand fees. This is essentially the membership fee for using those card networks. But the Amex fee structure adds to your overall processing costs.

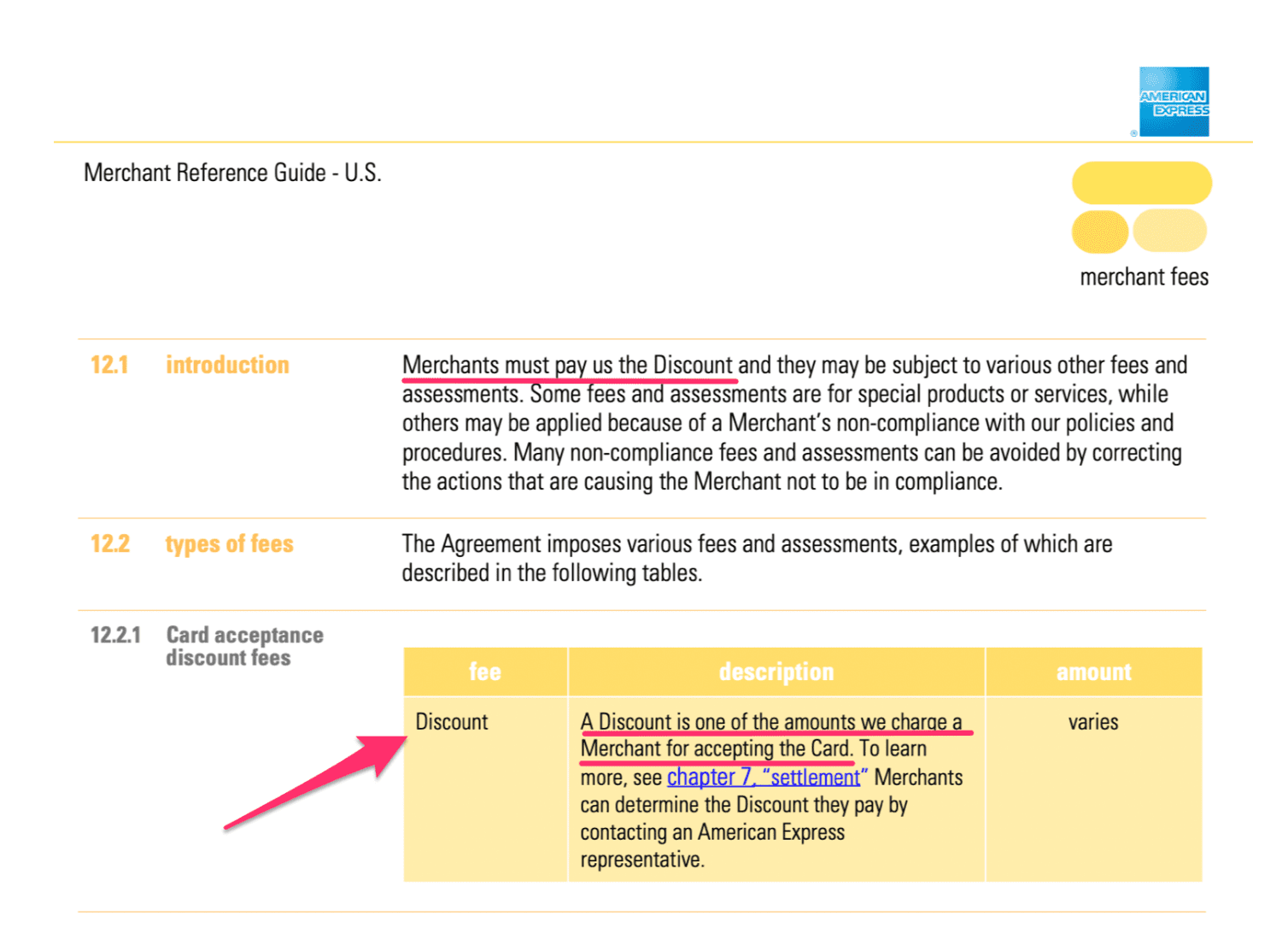

American Express Discount Fees

If you refer to the American Express Merchant Reference Guide — US, you’ll see a clear explanation of Amex discount fees.

I highlighted some of the key terms of this section. The language is basically identical to the definition of an interchange fee; it’s just called a “discount fee” instead. Amex interchange rates and discount fees can be used interchangeably.

So don’t get confused when you see that term.

How Much Does it Cost to Accept American Express Cards?

Historically, accepting Amex cards was complicated for small business owners. But as of late, American Express has made this much easier.

The cost of American Express credit card processing fees is based on four main factors:

- Processing terms (OptBlue vs. direct agreement)

- Industry

- Sale amount

- Transaction environment (in-person vs. online)

First, let’s talk about the two different ways that merchants can accept American Express cards.

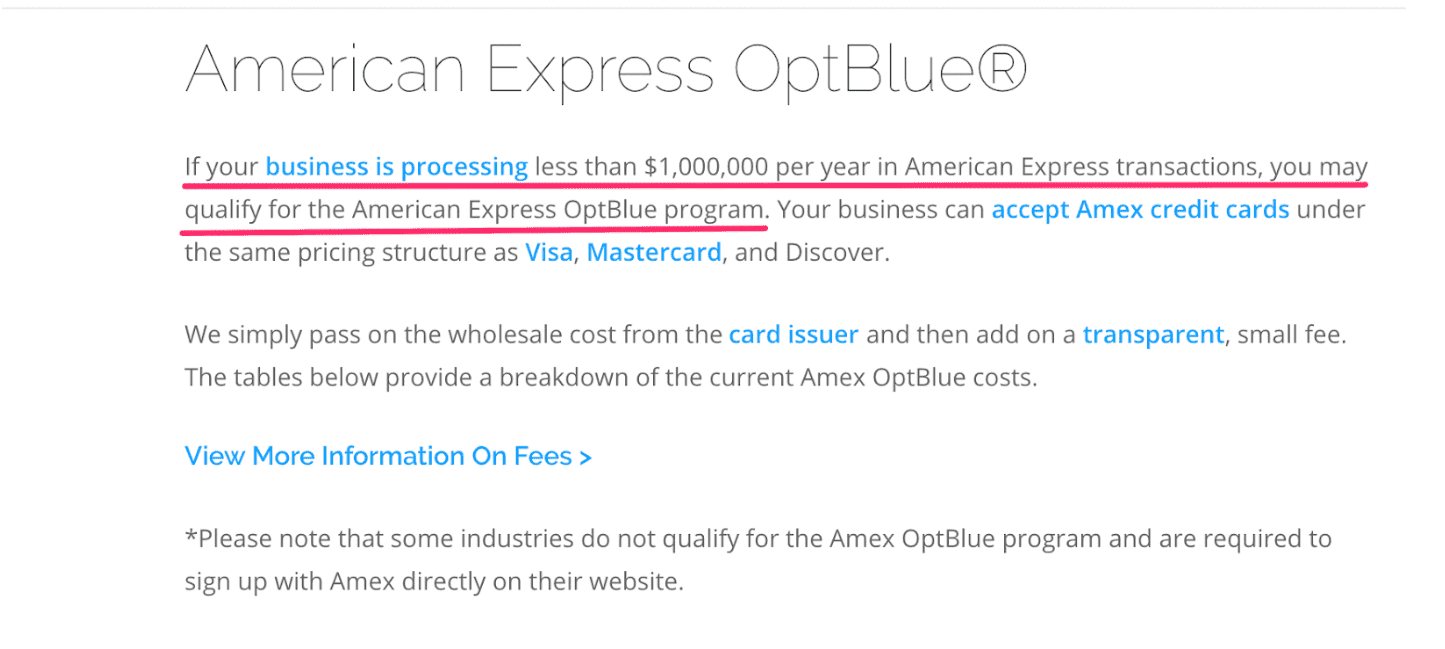

Amex OptBlue

OptBlue allows payment processors to offer American Express processing to merchants. Acquirers get wholesale rates and add a markup to merchants. This is essentially identical to the way Visa and Mastercard acceptance get offered through a processor.

With OptBlue, it’s easier for small businesses to accept American Express cards in-store, online, or both. There are no standardized rates here because processor markup fees will vary.

While it’s tempting to choose a processor based on their Amex rates, you should look beyond this one factor. Although it’s definitely on the list of things that need to be taken into consideration.

Amex Direct Agreement

OptBlue is only for merchants processing less than $1 million annually in American Express card transactions. Once you surpass $1 million for the year, you must switch to a direct merchant agreement through American Express.

Here’s an example of how this information should be disclosed on a payment processor’s website:

Every processing company will have similar wording on the website and in your merchant agreement.

This rule is mandated by American Express. As I mentioned earlier, Amex is a closed system, so they can pretty much do whatever they want.

The rates from a direct agreement with American Express will have higher interchange fees than the “wholesale” rates offered to processors in the OptBlue program. However, you won’t have to pay the processor’s markups.

For example, let’s say you were using merchant services from Wells Fargo Bank or another major bank. Once you reach the $1 million threshold processing Amex cards, you’ll no longer be able to use that merchant service provider. Smaller merchants typically won’t need to worry about this.

American Express Direct Agreement Pricing

Any merchant that processes American Express transactions should expect to see the following two fees on their statements:

- Network fee

- CNP surcharge

The network fee is essentially your membership cost for using the Amex network. The fee is roughly 0.15% of your total American Express transactions each month. If you accept a card remotely (like through an ecommerce website), you’ll pay an additional surcharge for card-not-present fees.

Again, an Amex direct agreement is required for merchants processing more than $1 million in American Express transactions per year.

There are two pricing structures for your direct agreement:

- Discount Rate Pricing

- Flat Per-Transaction Fee Pricing

I took this screenshot from the Amex Merchant Reference Guide we looked at earlier.

The discount rate structure is basically the same as the OptBlue program. However, you won’t be getting the wholesale rates. You’ll be charged a percentage of each transaction depending on your industry and transaction size.

The flat per-transaction rate is a little more complex. You’ll pay a fixed monthly fee for processing. But in order to qualify, you’ll need to stay within specified limits. This will only work for merchants who have an accurate estimate and stable processing volume from month to month. Otherwise, you’ll incur extra fees.

You won’t be able to find much information about the exact rates for either plan on the Amex website. The only way to get those prices is by applying for a direct agreement (once you eclipse $1 million per year in Amex sales).

Understanding Amex Interchange Rates

Generally speaking, most merchants don’t have a clear understanding of interchange fees and how they work. When it comes to American Express and those fees, the rates are even more of a mystery.

If you spend your time analyzing interchange charts from the major card networks, you’ll likely end up more confused than when you started.

Interchange Explained

In simple terms, interchange is the base cost of processing a credit card transaction. The interchange rates are set by the credit card networks, and they are universal for every credit card processor and merchant services provider. Regardless of how your specific processor advertises their pricing, contract, or processing fees, the interchange fees will always remain the same.

Interchange fees are listed in two parts. The table will include a percentage fee and a per-transaction fee. For example, let’s say the interchange rate for a particular category is 1.60% + $0.10, the interchange fee would be $1.70 for a $100 transaction.

How Amex Interchange Rates Are Determined

There are hundreds, if not thousands, of different interchange rates out there. That’s one of the reasons why this subject can be so confusing. It’s tough to determine the interchange portion of a translation without having all of the information.

Without getting too complex here, these are the main factors used by the card networks to determine interchange rates:

- Card Type — Rewards cards, airline affiliate cards, and cashback cards all have different interchange fees. These types of rewards are essentially paid for by the merchants who process the transaction. That’s why an Amex Platinum Rewards card has higher interchange fees than a debit card.

- MCC — The MCC (merchant category code) is another factor used to set interchange rates. A local dry cleaner won’t have the interchange fees as a car dealership. A hair salon won’t have the same interchange rates as an online cannabis merchant. Businesses with a higher risk for chargebacks typically pay higher interchange fees.

- Processing Method — The same card and transaction could incur different fees based on how the transaction gets processed. For example, ecommerce transactions cost more than a swiped card. Cards that are dipped cost more than transactions that were manually entered into a credit card terminal. Phone sales entered into a virtual terminal have different costs than a tap-to-pay card.

- Transaction Size — This factor is actually unique to the American Express network. It’s not necessarily the size of each individual transaction, but rather the average transaction value for the business. For example, merchants with a $50 average ticket value see different interchange fees than merchants with a $500 average ticket value.

For example, business and corporate purchases won’t have the same rate as debit cards. Credit card processing for international transactions will likely incur a few additional fees.

Again, there are lots of other factors used to determine interchange rates. Every card network has unique algorithms that they use to set these costs. But these four are the main ones that you should understand, especially for processing Amex cards.

Why Amex Interchange Rates Are Different

It’s no secret that American Express is unique compared to other major credit card networks. That’s largely due to the fact that Amex doubles as a card network and issuing bank.

While networks like Visa and Mastercard rely on third-party banks (like Wells Fargo bank) to issue their cards to the public, Amex handles this responsibility in-house. All American Express cards issued to consumers come directly from Amex itself, which is known as a closed system.

This independence from issuing banks extends beyond the cardholder and card network relationship—it also affects Amex’s relationship with merchants.

Additional Reading: Amex Chargeback Reason Codes Explained

Why Are Amex Costs So High?

American Express has a different business model than the other card brands. While Visa and Mastercard rely mostly on interest for their income, Amex also relies on fees from the merchant and annual fees from clients. The company does make some interest but nowhere near the scale of the others.

Should I Accept Amex at My Business?

We get asked this question a lot here at MCC. It really depends on various factors—including type of business, clientele and even location. That being said, there are a few major benefits to accepting Amex. Amex has very affluent consumer cardholders which means their customer base tends to spend more than the other card brands. While you may be paying a higher fee to take their cards you might be getting more business due to the fact.

How Can I Lower My Amex Pricing?

There are a few different options that we have found to be beneficial when looking to lower Amex pricing for our clients. The right path depends on whether you’re processing directly through Amex or going through a processing company.

If you are processing directly through Amex, it depends on your SIC Code and type of business Amex. There are some programs that can lower your fees directly. Sometimes these reductions can be significant if you understand which category to be in. Now, if you are processing through a standard credit card processing company, you must always try to make sure the structure and markup is the same for Amex as the other card brands. While the pricing will still be higher, there’s no reason these processing companies should charge a higher percentage on top of interchange than the others.

Are You Receiving the Best Possible Rate For American Express?

If you are wondering if you are at a competitive cost for taking Amex cards, simply submit your statement to us and our team will run a free analysis. From there, at least you will see if you are priced appropriately or if there is room for improvement.

Final Thoughts on American Express Interchange Rates

While American Express might have more complex pricing compared to Visa and Mastercard, it’s something that you’ll just need to deal with.

Amex cardholders are loyal to the brand. So if your business doesn’t accept Amex cards, you’ll run the risk of losing customers. Even if you’re paying a few additional fees, accepting American Express cards as a payment method is still worth it. This holds true for small merchants as well.

In most cases, you’ll pay more to process American Express cards. Some payment processors charge the same rate for all cards. Just remember you can’t get Amex through your credit card processor if you reach $1 million per year in Amex transactions. This requires a direct agreement.

Merchants are price-sensitive to credit card processing fees. At Merchant Cost Consulting, we understand how you feel. Contact us today to learn more about how much money you can save on credit card processing.

{kind=link}