In recent years, credit card surcharging has been one of the hottest topics in the payments space for merchants and consumers alike.

While it’s legal to surcharge credit card transactions in most states (including Colorado), Colorado is one of the states that has some contingencies you should be aware of.

Disclaimer: This information is for reference only, and it does not constitute legal advice. Consult with an attorney with any legal-specific questions.

Is It Legal to Surcharge Credit Card Transactions in Colorado?

Yes, credit card surcharging is legal in Colorado under the following conditions:

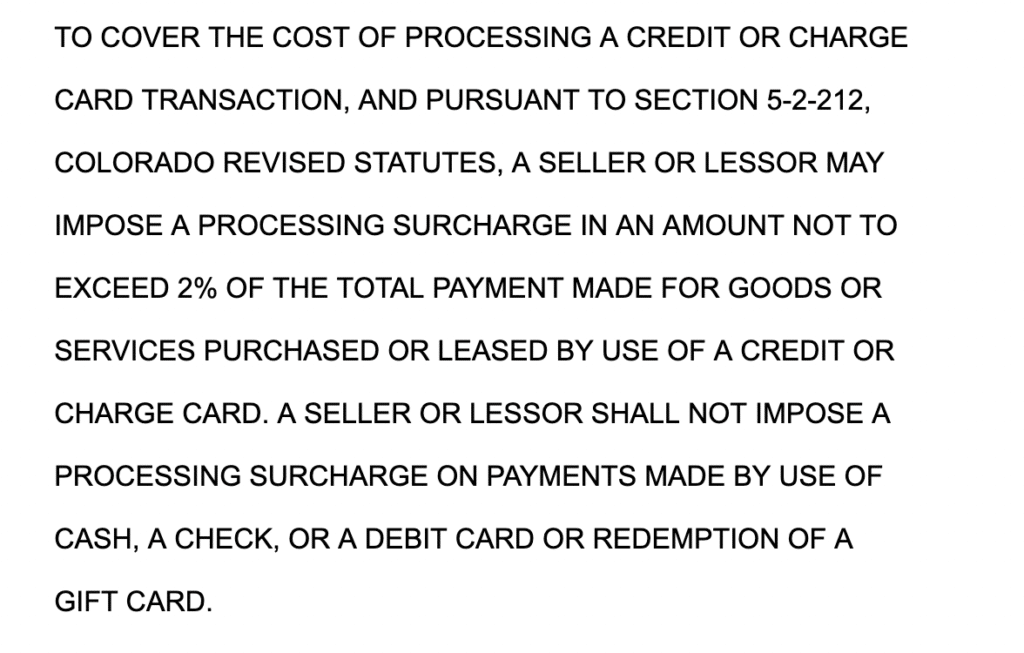

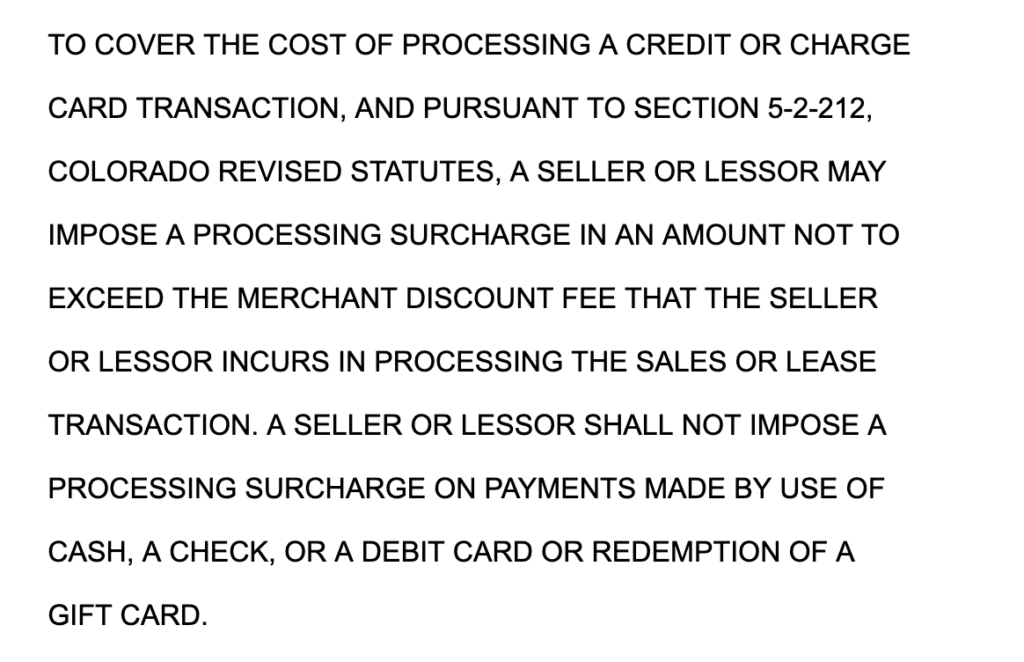

- Surcharges must not exceed 2% of the transaction,

- OR the surcharge must not exceed the total cost of the merchant’s processing fee for the transaction.

- Merchants are required to display notice of the surcharge to consumers prior to the completion of the sale.

These rules are defined by Colorado Senate Bill 21-091, and they apply to both in-person and online transactions.

When Surcharging is Prohibited in Colorado

Surcharging is only legal on credit card transactions in Colorado. Merchants are prohibited from adding a surcharge to:

- Debit card transactions.

- Cash transactions.

- Check payments.

- Gift card redemptions.

Merchants in violation of SB 21-091 can be penalized as a creditor under Colorado’s Uniform Consumer Credit Code.

Breaking Down the Details of Colorado’s Credit Card Surcharge Laws (To Help You Stay Compliant)

Now that you’ve seen the basics of Colorado’s credit card surcharge laws, let’s take a closer look at the granular details. Remember, always consult with a local attorney before you consider applying a surcharge. But this information will help you understand things a bit more.

You Can Surcharge Up to 2% OR Your Cost to Accept the Card

For merchants to legally surcharge in Colorado, they can choose to add a 2% surcharge to all credit card transactions OR impose a surcharge fee that reflects the merchant’s cost of accepting that card.

Unless your POS software can accurately calculate your cost of acceptance for each transaction, going with a blanket 2% charge on all credit cards is the easiest route.

While it depends on your merchant agreement, most businesses pay several different rates for each transaction. Factors like the card brand (Visa vs. Amex), card type (cash back vs. rewards), transaction amount, whether you’re getting a qualified rate, certain assessment fees, and other criteria impact your costs.

For example, let’s say you decided to impose a 3% surcharge on all of your credit card transactions. But one of those transactions only costs you 2.5% to process. This scenario would be illegal in Colorado.

Why? In this example, your surcharge exceeds the 2% maximum allowable rate and it exceeds your cost of acceptance.

The only way you can impose a credit card surcharge in Colorado that exceeds your cost of acceptance is if your cost of acceptance is less than 2%.

You Still Need to Follow Federal Laws Governing Surcharges

The state of Colorado says it’s legal for merchants to charge a credit card surcharge that covers their cost of acceptance for that transaction. However, there is a federal cap of 4% for credit card surcharges in all 50 states.

Let’s say a particular transaction costs you 5% to process. The wording of Colorado’s surcharge law may sound like you could charge a 5% fee to your customers—but that’s incorrect and illegal.

In this scenario, you’re still bound by the 4% maximum allowable surcharge fee that’s governed by the Fed.

Note: Your transactional costs should never be 5%. If so, it’s a red flag and a sign that you’re overpaying for credit card processing.

Don’t Forget About the Card Brand Rules

All of the card networks have their own rules and requirements for how merchants handle surcharges. Generally speaking, the card brands say:

- You can’t surcharge customers more than 3% per transaction.

- You must apply surcharge fees equally to all card types (meaning you can’t charge 2% on Discover cards and 3% on Visa cards).

- You must notify customers of the surcharge prior to charging it.

Technically, you won’t be breaking the law if you don’t follow these rules. However, you could be subject to penalties under your merchant agreement—including fines and potentially lose your ability to accept certain cards.

Make Sure to Display Notice of Your Surcharge Program

It’s mandatory under Colorado law for merchants to clearly display notice of their surcharge before a customer pays for goods and services. This notice applies to both in-person and online transactions.

This rule is all about transparency and ensures customers aren’t blindsided with an added fee.

According to SB 21-091, your notice must include exact language. There are two options to consider, depending on whether you’re charging a 2% surcharge or you’re charging the exact fee per transaction.

If you’re charging a 2% surcharge, your notice needs to say:

If you’re charging a surcharge based on your transactional cost, the notice needs to say:

Quick History of Colorado’s Surcharge Laws

Credit card surcharging was actually illegal in Colorado until July 2022. There were only two exceptions to this old law:

- State agencies (like the Colorado DMV) were allowed to impose surcharges on credit card transactions.

- Merchants could impose a cash discount instead of a surcharge (listing the price of an item as $52 but charging $50 to customers who paid with cash).

Some merchants tried to work around these rules by charging a convenience fee in lieu of a surcharge. But this was a legal gray area, and likely illegal in most instances.

This all changed when SB 21-091 went into effect on July 1, 2022.

The new law lifted bans that were previously considered illegal and extended the right to surcharge for all businesses (not just state agencies).

Final Thoughts

Just because surcharging is legal in Colorado, merchants should still think twice before passing fees to customers.

In the long run, squeezing a few extra dollars out of each transaction to cover your processing costs may actually hurt you—as consumers nationwide have a negative sentiment when it comes to paying surcharge fees.

Are you really willing to lose a loyal customer over $2 or $3? I hope not.

That said, this is totally your choice. Just talk to a lawyer about it to make sure your surcharge program is actually legal.

If you’re going to impose a surcharge fee, I think it’s easier to just go 2% across the board. There’s too much room for error if you try to calculate the exact cost of each transaction. And while some providers offer this type of service, it’s probably not worth switching processors for this single feature.

Alternatively, you can always look for other ways to lower your payment processing costs. You can save money without burdening your customers—so it’s a win-win all around.

If you’re interested and want to learn more, contact our team here at Merchant Cost Consulting. We can audit your statements to identify bogus fees and overages. From there, we’ll negotiate your rate directly with your processor on your behalf. So you can save money without having to change anything.

{kind=link}