Interchange Downgrades: How to Avoid Them

Any company accepting credit cards is likely familiar with interchange fees. If you’re not or you need to brush up on your knowledge, check out our complete guide to interchange fees and rates.

In the simplest possible terms, interchange is one of the main costs associated with processing a credit card transaction.

Based on factors like how the payment was accepted, card type, and merchant type, each transaction is put into a category to determine which interchange fees will be assessed.

But if something in that transaction changes, an interchange downgrade might apply.

What Are Interchange Downgrades?

Every credit card transaction has a target interchange category. Your target interchange category has the lowest interchange fees, assuming everything goes according to plan.

This will be the best-case scenario for your business.

When specific requirements aren’t met, not enough information is provided, or something else happens, a transaction can move from one category to another.

An interchange downgrade happens when this re-categorization occurs. As a result, you’ll incur extra interchange fees for the new category.

Interchange downgrades are somewhat of a complex subject. But if you don’t take the time to learn how they work, you could be throwing thousands of dollars away each year.

Common Causes of Interchange Downgrades

There are certain scenarios that will automatically trigger an interchange downgrade. Before you can avoid an interchange downgrade, you need to understand what’s causing them in the first place.

Here are some of the most common reasons for interchange downgrades.

Delayed Authorization

This is also known as a “stale” authorization. It occurs when too much time passes between the initial authorization and the credit card settlement.

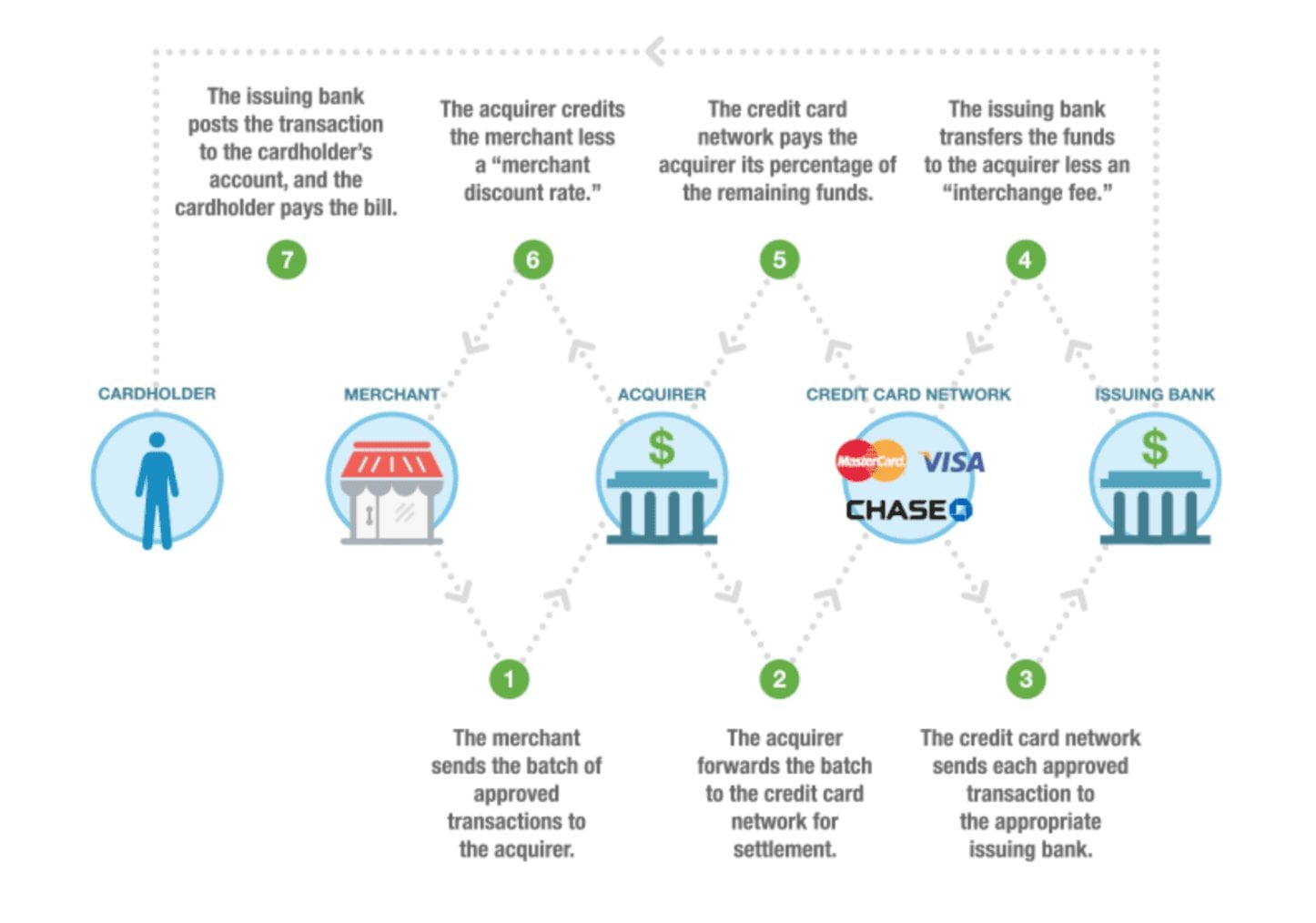

All credit card transactions must be settled for your business to receive funds from the transaction. Here’s a visual representation of how the settlement process works.

If you wait too long to settle your transactions, the authorization will go stale. When this happens, a transaction can downgrade.

How much time you’re allowed before an authorization goes stale varies depending on the interchange qualification.

But here’s a general rule of thumb. The majority of interchange categories require a settlement within 24 hours of a transaction occurring.

Mismatched Authorization

The sale amount must always match the authorization amount. Here’s an example to show you what I mean.

Let’s say a customer buys $100 worth of merchandise at your brick and mortar retail store. You obtain the authorization that’s required to approve the transaction. But then the customer decides they don’t want to buy one of the items. This change brings the sale total down to $75.

You must cancel the transaction and redo it. Otherwise, you can face a downgrade.

Poor Security

Payment processors and card networks take security measures very seriously. They require merchants to abide by certain security protocols to protect cardholders.

Your application of these security measures will impact your interchange category.

For example, let’s say you have an eCommerce store and forget to use an AVS (address verification system) to verify that the customer’s billing address matches the card used in the transaction. An interchange downgrade could occur as a result.

Interchange Downgrade Fees

As I briefly mentioned earlier, interchange downgrades cost more to process.

You won’t be assessed a specific fee or penalty based on the downgrade. Instead, the transaction will just fall into a new category with higher credit card processing rates.

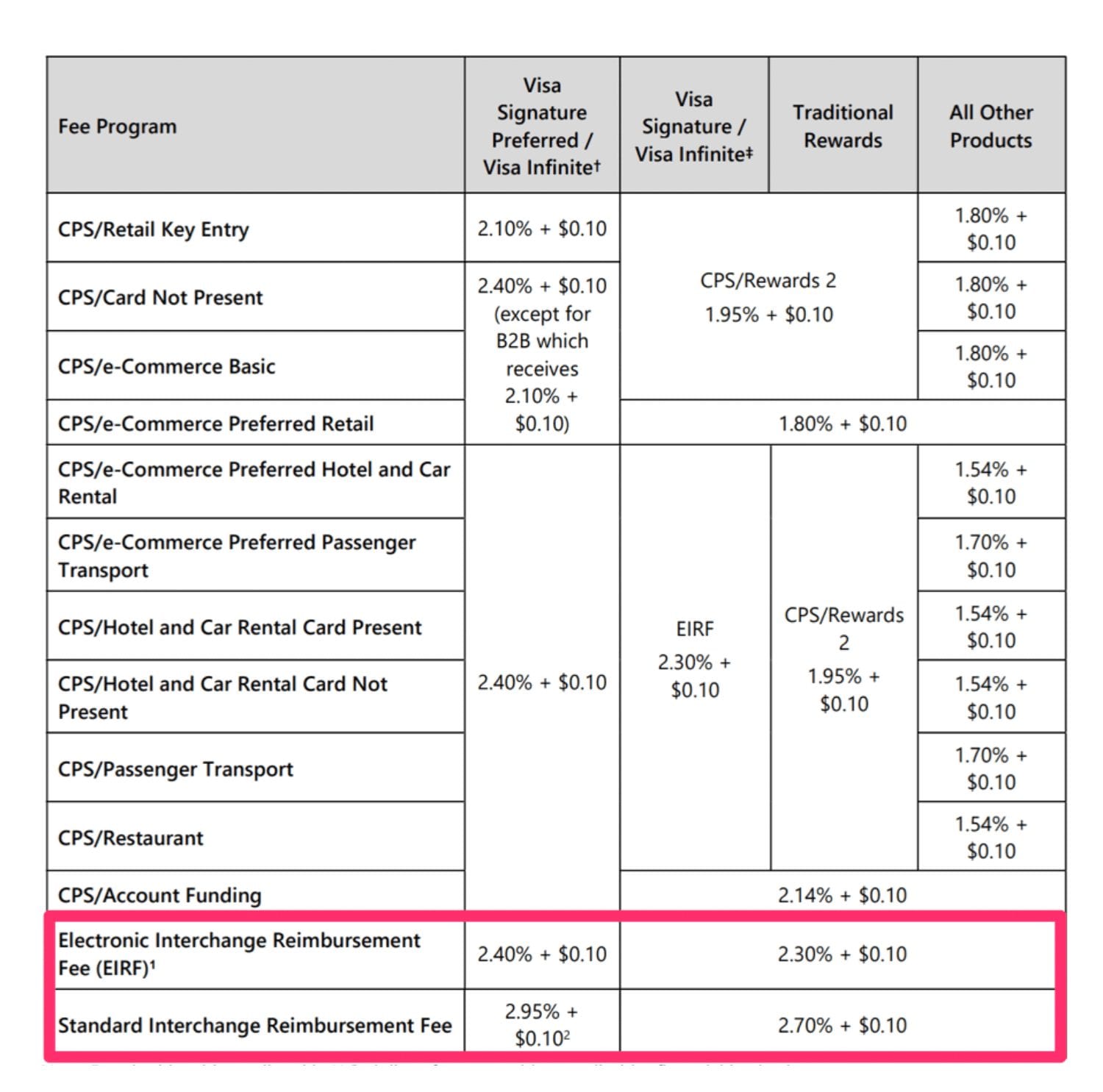

To further explain, let’s take a look at some of Visa’s interchange rates.

I highlighted the bottom section of this table to showcase the electronic interchange reimbursement fee (EIRF) and standard interchange reimbursement fee (SIRF) for consumer credit cards.

Transactions will first be downgraded to the EIRF. But like any other interchange category, EIRF also has its requirements. If those requirements aren’t met either, the transaction will downgrade to SIRF.

Here’s an example:

For simplicity’s sake, let’s say your target interchange category is CPS/Retail for a Visa Signature card (top line on this table). If something goes awry, like you wait several days to settle the transaction, it would downgrade all the way to SIRF.

At the card level, this interchange fee just went from 2.10% + $0.10 to 2.95% + $0.10.

You paid an extra 0.85% because of the downgrade. That may not seem like much, but let’s say your company processes $10 million in credit cards annually. If all of those transactions were downgraded at this rate, you’d pay an extra $85,000 in credit card fees. That doesn’t even include your processor’s markup.

How to Prevent Interchange Downgrades

While certain interchange downgrades are unavoidable, some of them can be prevented. Follow these quick tips and best practices to save money on credit card processing.

Settle Batches Every Day

Always settle your credit card batches daily. As previously discussed, delayed authorizations or “stale” authorizations are a leading cause of interchange downgrades.

You can set up most POS systems to do this automatically at a specific time each day.

If you have a large organization that’s processing transactions at scale, this type of feature will be extremely helpful for avoiding an interchange downgrade.

Don’t Force a Transaction

We already talked about the importance of credit card security in the payment processing industry. But merchants have the ability to bypass certain security protocols in order to force transactions to the credit card processor.

In some cases, merchants do this to save time when processing a transaction. We strongly advise against this.

Forcing a transaction will automatically lead to a downgrade. Don’t cut corners to save time. It can ultimately make your transactions more expensive.

Make Sure You’re Using Updated Equipment

Using old and outdated hardware and software could lead to an interchange downgrade. Aside from the security protocols, some equipment could fail to collect certain pieces of crucial data.

Make a habit of assessing the condition of your equipment on a regular basis. Take steps to ensure that it’s been set up correctly, and it’s secure as well.

Review Your Downgrade Reports

Request a downgrade report from your credit card processor. This will help you identify how many downgrades you’re getting. The report will also explain which interchange requirements weren’t met.

Ultimately, a review of your interchange downgrade reports can give you insight into what’s causing downgrades in the first place. Then you can take the proper steps to prevent them moving forward.

Final Thoughts

You need to understand every aspect of your credit card processing fees. While interchange downgrades aren’t talked about frequently, they can add up quickly.

For larger organizations and enterprises that are processing millions of dollars each year, interchange downgrade fees can total tens of thousands of dollars annually.

If you need help assessing the cause of these fees and want to save money on credit card processing, contact our team here at Merchant Cost Consulting.

{kind=link}