Cash flow is crucial to the success of any business. For most merchants, the majority of incoming cash comes from credit card processing sales.

But giving your customers the ability to pay for goods or services with a credit card doesn’t mean you’ll get funded instantly.

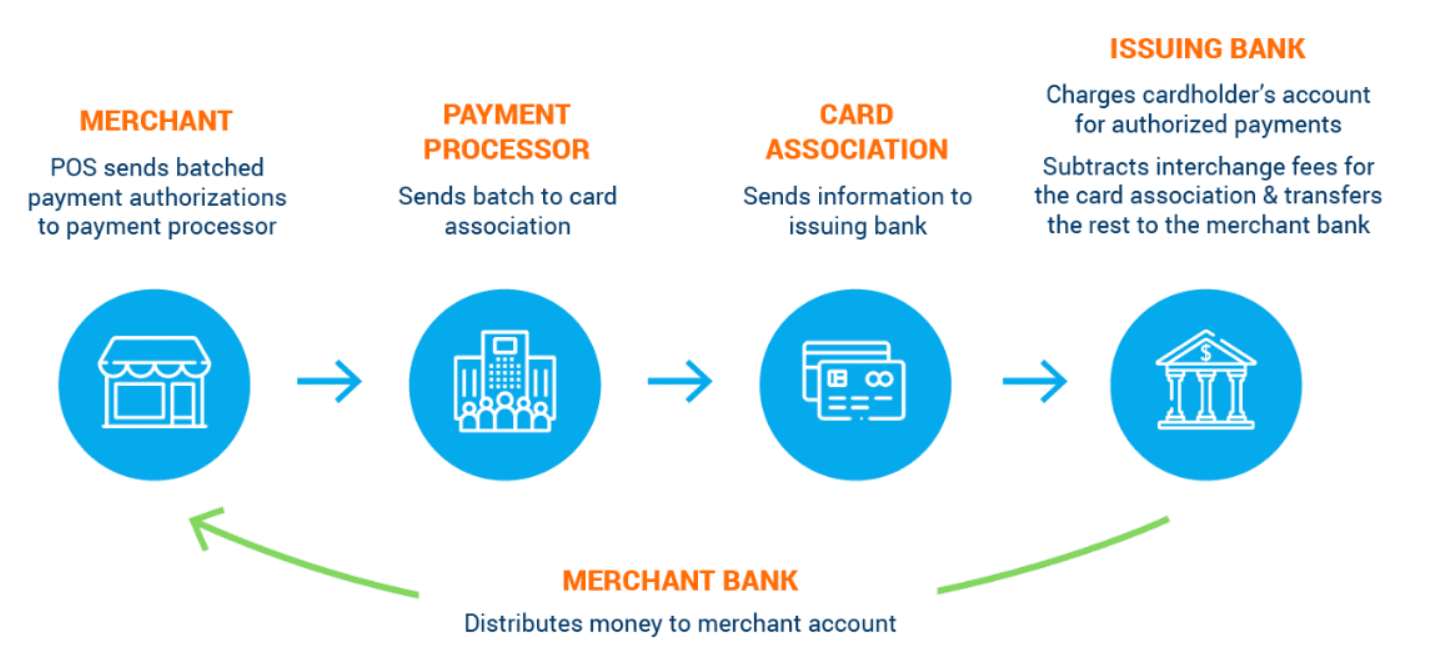

In most cases, there is a gap between the time a card is dipped or swiped, and the moment those funds reach your bank account. This can be anywhere from a few hours to a few days, depending on several factors.

To get your money, credit card processors need to facilitate the transaction between two banks:

- Issuing bank (the cardholder’s bank)

- Acquiring bank (the merchant’s bank)

While most of this will be automated, it’s still possible for delays to occur. In some instances, processors will intentionally hold funds from merchants. You can review our guide on how to prevent payment processing funds on hold for more information on this.

With that said, there are certain things you can do as a merchant to ensure you get paid quickly. Just follow these eight tips and best practices that I’ve identified below.

1. Know Your Processing Limits

Some credit card processing companies have weekly or monthly limits for merchants based on credit card processing history. If you exceed those limits, it can automatically trigger a hold on your account. In some instances, exceeding your processing limit could even cause an account termination.

Even if you don’t have a processing limit, any weeks or months when the processing amount is drastically above normal will raise a red flag with your processor.

For example, let’s say you’ve been getting roughly $20,000 per month in credit card sales, on average, over the last three years. If you have $90,000 in transactions next month, your processor may start holding your funds to investigate what caused the spike.

So if you’re expecting a busy week or month due to some type of promotion or special event, it’s best to inform your processor ahead of time. Gradual increases over time are far less suspicious.

2. Provide Documentation For High-Ticket Transactions

Similar to an unusual month of high volume sales, a larger than normal single transaction will also raise a red flag with your credit card processing company. That’s why you should always capture customer signatures on a written invoice for any big purchases.

Some merchants will automatically hold a certain percentage of transactions exceeding a specific value, which should be described in your merchant agreement.

If your average order value is $50 and one transaction is $1,900, your processor likely won’t release those funds right away. But if you can provide them with written documentation to verify the sale, it will help you get paid faster.

All businesses selling high-ticket items (furniture, electronics, etc.) should capture signatures and keep detailed documentation, even if they always have a high AOV.

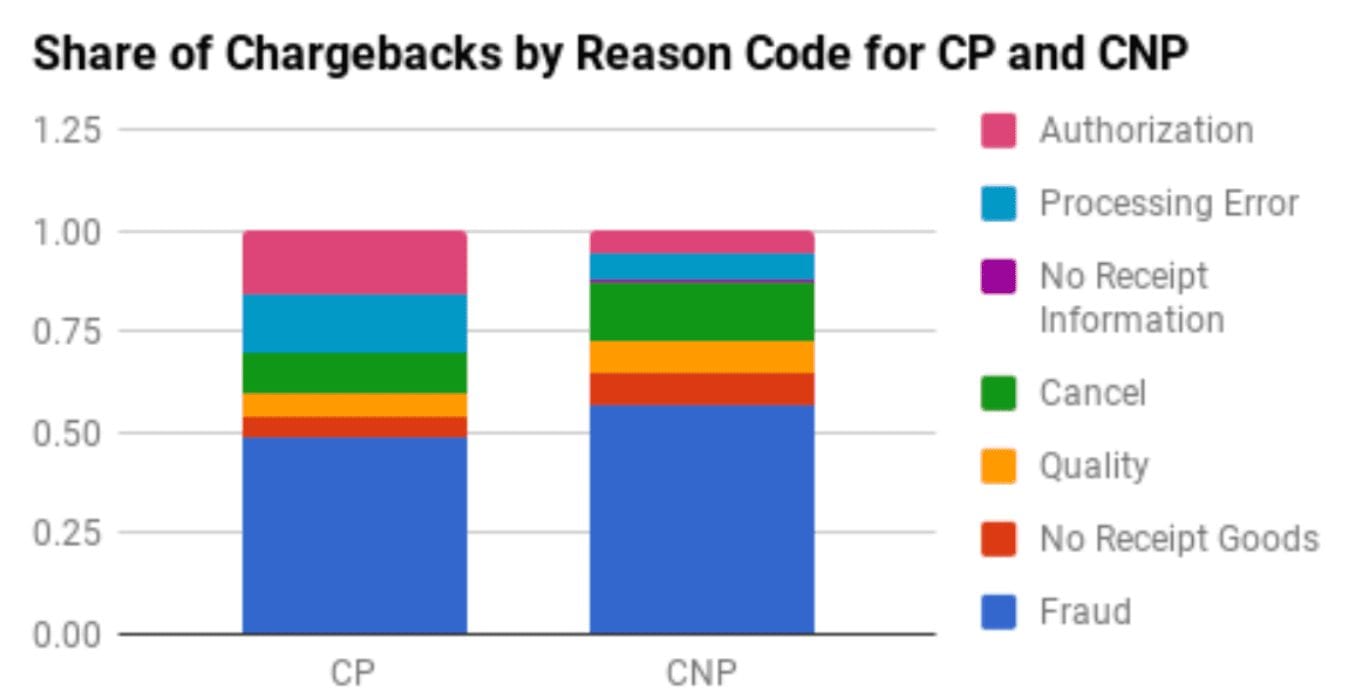

3. Reduce Chargebacks

A chargeback occurs when a customer disputes a credit card charge by directly contacting the issuing bank. This causes a reversal of funds between the merchant and the customer.

Payment processors are more likely to withhold funds from merchants with a high chargeback rate. Customers file chargebacks for a wide variety of reasons.

As you can see from the graph, the vast majority of chargeback reasons are related to fraud, but we’ll discuss that in greater detail later.

Most merchants can take steps to prevent chargebacks.

According to a recent study, 80% of consumers filed chargebacks simply because it was easier than requesting a refund directly from the merchant. So implementing a customer-friendly return policy will lower your chargeback rate.

Check out this guide on chargeback prevention tactics. Eliminating chargebacks reduces the chances that your processor will withhold your funds.

4. Avoid Keyed Transactions

Swiped and dipped credit card transactions process faster than a transaction that was manually keyed. That’s because a magstripe or EMV chip is registered as card present, whereas keyed transactions are card not present.

In addition to keyed transactions taking longer to process, they also come with higher merchant processing fees.

Note: Are you paying too much for credit card processing? Get a free audit and analysis to find how much money you can save.

While the occasional keyed transaction is sometimes unavoidable, doing this on a regular basis will raise suspicion in the eyes of your credit card processor. An unusually high number of keyed transactions can even cause a hold on your funds.

5. Find the Right Payment Processor

While it’s rarely cost-effective to switch payment processors, finding the right processor is crucial to getting your funds fast. For those of you who are in the market for a new payment processor, here are some that have a reputation for releasing funds quickly:

- Payment Depot: 24-48 hour funding

- Helcim: Payouts in two business days for most US merchants. Next-business-day funding for weekend transactions.

- Square: Funds routed to a digital wallet that can be used instantly.

- Dharma: Payouts in two business days. Retail merchants eligible for next-day funding with card-present transactions.

- PayPal: Funds available in PayPal account immediately.

- FattMerchant: 24-hour funding for all merchants.

If you choose a merchant that delivers funds in 3-5 business days, don’t expect to get your money immediately. Always check the terms before you agree to anything.

6. Keep a High Bank Balance

Credit card processors want to protect themselves in case a chargeback is issued by a customer.

That’s why some processors will ask to see a bank statement while funds are placed on hold. A high balance re-assures the processing company that you’re able to cover the costs for a chargeback, in the event that this happens.

This is sort of a catch-22 since you need credit card funds to keep a steady cash flow, but those funds can ultimately help you get paid faster as well.

7. Optimize Your Batch Times

Settling your credit card transactions at a specific time can help you get funds faster.

As a merchant, you can send batch payment authorizations to your processor whenever you want. But doing this once every 24 hours is the industry standard.

With that said, most processors have a cut-off time for when a settlement is eligible for next-day or two-day funding. For example, a processor might require batched payments by 7:00 PM EST Monday-Friday to get next-business-day funding. If you batch out at 8:00 PM, it wouldn’t be processed until the following day at 7:00 PM, which would take an extra day to get your money.

Always confirm deadlines with your credit card processor, so you know the most optimal time to submit batches for processing.

8. Use Fraud Prevention Best Practices

As I briefly mentioned earlier, fraud is a top reason why chargebacks occur and why funds get placed on hold. If your processor believes a transaction is fraudulent, they won’t release the funds.

Merchants who process lots of fraudulent transactions could even have their merchant accounts suspended. I highly recommend you review our fraud prevention tactics guide. These tips will also help you get paid faster from your processor.

Final Thoughts

Just because a customer swipes or dips their credit card and leaves with merchandise, it doesn’t mean that those funds will hit your bank account immediately.

In some cases, it can take up to five business days, or longer, for processors to release funds to merchants.

If you want to get paid as fast as possible, follow the merchant best practices that I’ve outlined above. Let us know if you have any other questions or need further assistance.

{kind=link}